- Ranking the 23 books I read in 2022

It’s the eight installment (wow) of my annual year in reading. You can see past lists here.

23. God Bless you, Mr. Rosewater – Kurt Vonnegut Jr.

It’s pretentious and doesn’t have much of a plot. Read Cat’s Cradle or Slaughterhouse Five instead. Wikipedia

22. Cold Mountain – Charles Fraiser

Struggled to finish this novel about returning home after the Civil War. Surprised it’s considered a modern classic. Wikipedia

21. Thinking Basketball – Ben Taylor

Ben Taylor is an incredible basketball writer. His writing taught me an incredible amount about not only analytics, but strategy. I didn’t love the book, but that’s because it’s aimed at a more general audience. If you feel comfortable talking about usage rates and efficiency ratings, skip the book and head over to his wonderful website.

20. The Money Culture – Michael Lewis

A collection of Lewis op-eds and articles from the 1980s-1990s. Thriftbooks

19. Financial Literacy for Managers: Finance and Accounting for Better Decision-Making – Richard Labert

Good basic book on understanding corporate finance. Website

18. Operations Rules: Delivering Customer Value Through Flexible Operations – David Simchi-Levi

High level overview on building an agile organization. MIT Press

17. Bloodchild and Other Stories – Octavia Butler

Short story collection from one of America’s best science fiction writers. Wikipedia

16. How the World Really Works: A Scientist’s Guide to Our Past, Present and Future – Vackav Smil

A “realist” look at societies impending transition to a green economy. Smil frames the book around a handful of different commodities (concrete, fertilizer) and essentially argues that it’s going to be a lot harder to transition to green energy than promoters will admit. My general complaint is that it suffers from a lack of imagination. He devotes a chapter to the production of industrial fertilizer, which is an important commodity and required for America’s industrial food system. However, he never stops to ask if an industrial agricultural system is the one we should have. Website

15. The Dawn of Everything: A New History of Humanity – David Graeber

One of the bigger “big picture” books of last year. It’s fine. I just get tired of reconsidering the past. Website

14. The Nineties – Chuck Klosterman

One of America’s foremost cultural critics examines the last era of monoculture. Website

13. The Kelloggs: The Battling Brothers of Battle Creek – Howard Market

The story of how a celebrity doctor and his brother revolutionized America’s breakfast. It’s surreal how primitive society’s understanding of nutrition was 100 years ago. Impossible to consider how our modern system will look 100 years from now. Bookshop

12. Financial Statement Analysis: A Practitioner’s Guide – Martin Fridson

A fairly detailed look at understanding specific nuances around financial statements. As is all business analysis, industry context and expertise matters. Website

11. The Goal – Eliyahu Goldratt

There’s a reason this book is on every single operation’s person’s reading list. A wonderful fictional tale about how to optimize a manufacturing plant. Wikipedia

10. The Lords of Strategy: The Secret Intellectual History of the New Corporate World – Walter Kiechel

A thorough and detailed look at the rise of management consulting and its impact on the corporate world. Who would of thought that the industry took off because they were the only ones who knew how to calculate detailed profitability for far-reaching conglomerates? Harvard Business Review

9. Blood, Sweat & Chrome: The Wild and True Story of Mad Max: Fury Road – Kyle Buchanan

Oral history of the best modern action movie. Website

8. The Thousand Autumns of Jacob de Zoet – David Mitchell

I picked this up because Cloud Atlas, the science fiction novel that redefined a genre, is one of my favorite books. Turns out Thousand Autumns of Jacob de Zoet is historical fiction. The first third is slow, the second third is fine. The last third of the book is great. Wikipedia

7. Merchants of Grain – Dan Morgan

Food is inherently political. In America, affordable food is taken for granted, but a lack of it can destabilize governments and topple regimes. Dan Morgan investigates how five private companies control what the world eats, and what people pay. The book is dated (first published in 1979) but timeless in its analysis. Amazon

6. Gangsters of Capitalism: Smedley Butler, the Marines, and the Making and Breaking of America’s Empire – Jonathan Katz

Explores the origins of modern American imperialism through the lens of one of America’s most decorated Marines—Smedley Butler. Website

5. The Money Machine: How KKR Manufactured Power and Profits – Sarah Bartlett

The mechanics behind private equity are simple, but the industry spent decades and billions of dollars convincing people that it’s somewhat mystical. Financers aren’t simply stripping American industry for profit—they’re financial engineering! Written in the early 1990s, before the ensuing PR blitz to rebrand the industry, Bartlett examines the rise of one of America’s most notorious and profitable leveraged buyout firms—KKR. Abe Books

4. Narrative and Numbers: The Value of Stories in Business – Aswath Damodaran

If you’re starting out in finance, I highly recommend checking out the work of Professor Damodarn. Here he’s produced a book on the importance of crafting stories out of finance. Columbia University Press

3. The Night the Lights Went Out: A Memoir of Life After Brain Damage – Drew Magary

A suspenseful and empathetic book about surviving a brain hemorrhage. Website

2. A Memory Called Empire – Arkady Martine

A mystery science fiction novel that is both gripping and thought-provoking. Martine delves into the nature of consciousness while simultaneously examining colonialism. It deservedly won the 2020 Hugo Award for Best Novel. Wikipedia

1. The Lords of Easy Money: How the Federal Reserve Broke the American Economy – Christopher Leonard

For my money, Christopher Leonard is one of the best business writers working in America. Here, he takes a look at qualitative easing and its spiraling effects on the economy. Very modern business writers understand monetary policy. Leonard is one of them, and he explains it brilliantly. Website

Photo by Alexander Grey on Unsplash

- Consumption is still strong at Target, despite inventory woes

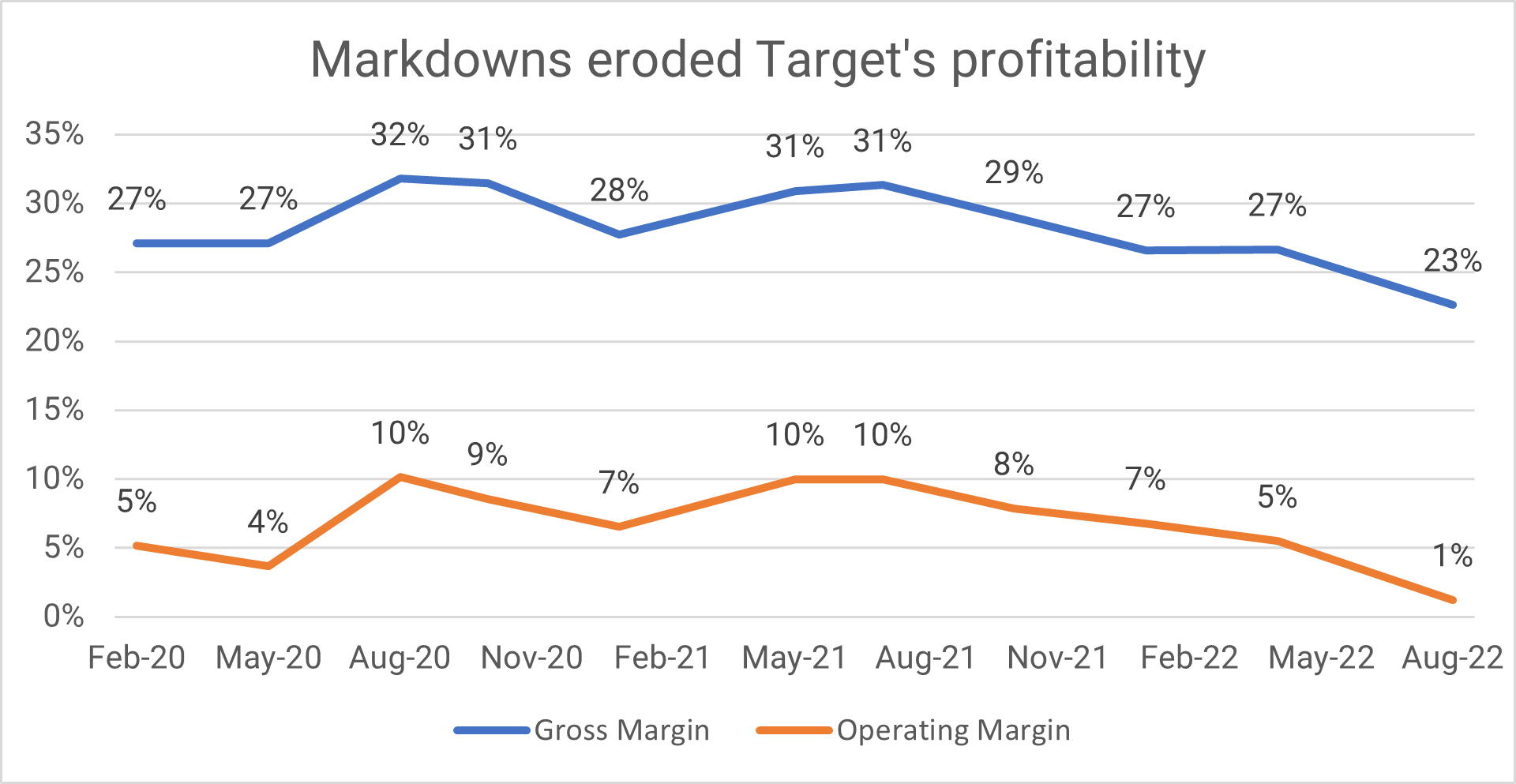

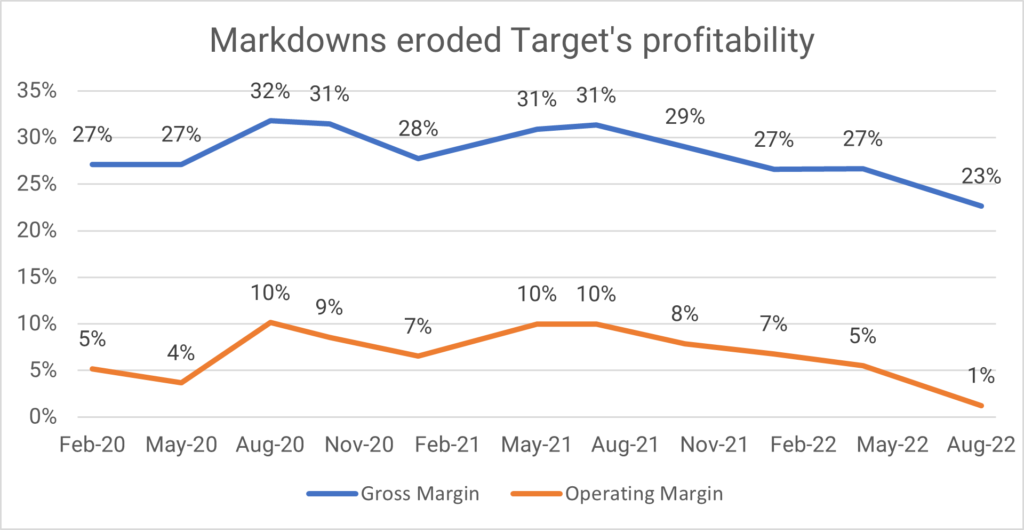

Target saw operating margins crumble after a forecasting miss pushed the company to rapidly mark down billions of dollars of apparel in a few short months. The Minnesota-based retailer typically earns around 30% gross margin across its portfolio but saw that number decline to about 23% this quarter. The numbers fall even further when accounting for operating expenses—down to about 1%. “Our focus throughout the second quarter was to ensure that we took care of the excess inventory of our network and adjust future receipts to reflect the rapid change in sales trends we’ve seen so far this year,” CFO Michael Fiddelke told investors. “We accomplished this goal to the benefit of our operations, our team and our guests.”

Inventory levels should stabilize at Target

According to management, inventory markdowns accounted for almost all margin compression, and it expects profitability to return to normal levels. “Based on the success of our Q2 inventory actions and our current performance,” CFO Michael J. Fiddelke said, “we remain positioned to deliver an operating margin rate in a range around 6% in the fall season.”

Despite the poor profitability, Target had strong sales growth. Overall, comparable sales increased almost 3%–on top of nearly 9% a year ago. Essentially, sales are up 11% from the pre-pandemic era. It isn’t just inflation. According to management, Target is growing in unit share and traffic. Even for discretionary items, where the company had significant markdowns, sales were still strong. There just wasn’t much margin. “Sales were softer than a year ago,” Chief Growth Officer Christina Hennington said, “but remained nearly $3.5 billion or more than 35% higher than the second quarter of 2019.”

As you can imagine, the composition of sales will change moving forward. Target is prioritizing food and beverage while supplementing it with high-margin categories like Beauty, toys, and its brands. The company now boasts 12 $1 billion brands. Given that Target took a big inventory loss over the last two quarters, management feels they have an efficient machine that should start returning significant returns.

“Time and time again”, Hennington said. Share and traffic “have proven to be a better barometer for lasting success than growth solely through average retail prices. That’s why I’m so encouraged that across all 5 of our core merchandising categories, we grew unit share in the second quarter.” - In Q2, Walmart managed inflation and inventory levels

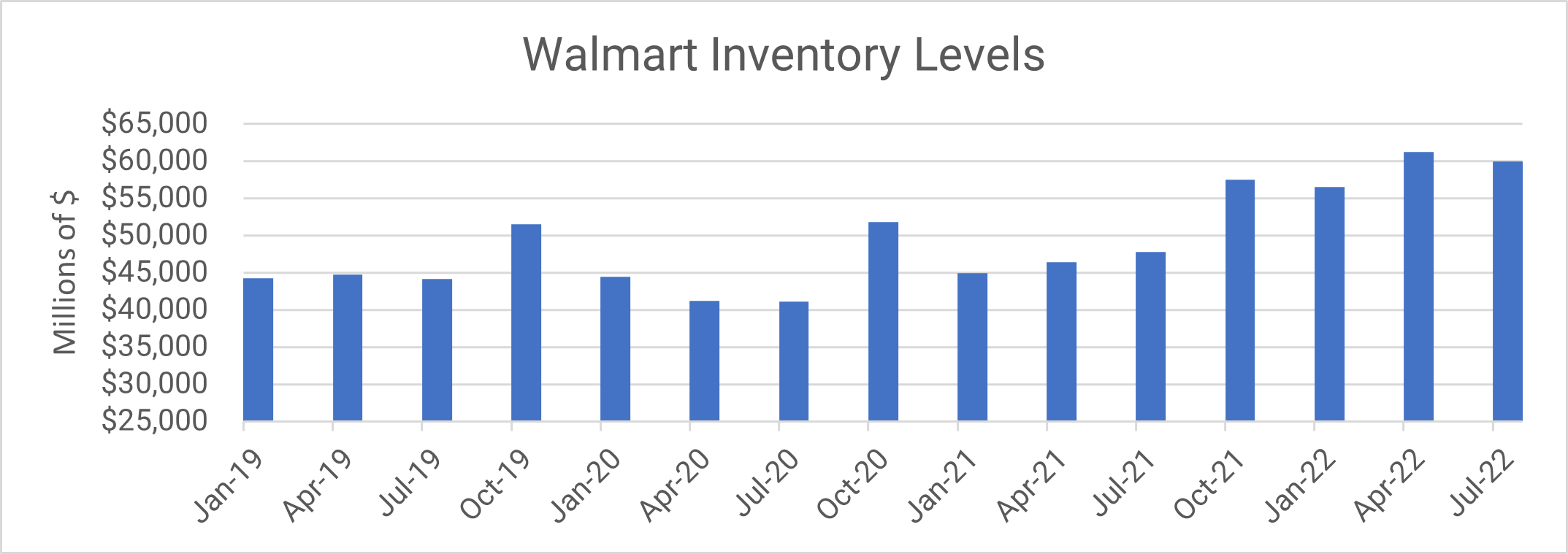

Weeks after lowering sales guidance, Walmart delivered reasonable sales growth amid heightened inventory levels. America’s largest retailer saw U.S. sales grow 6.5% compared to the previous year’s quarter while increasing in-store fulfillment for online ordering by nearly 40%. Management noted a fair number of shifts in consumer behavior, with shoppers trading from deli meats to canned tuna. “We finished the quarter on a strong note,” CFO John David Rainey told investors on the call.

A new normal for Walmart Inventory Levels?

Last quarter the company announced it was going to aggressively mark down apparel after forecasting errors flooded the company’s warehouses with unneeded items. “We’ve made good progress to reduce inventory levels where we’ve focused and taken markdowns,” CEO Doug McMillion said. Inventory is down from last quarter’s high, but still almost $15 billion higher than the pre-pandemic era. The absolute number is slightly misleading, as a fair amount of the cost is inflation related.

McMillion explained:Take the U.S. inventory increase in the second quarter of $11 billion. If you decompose that, about 40% of that is due to inflation. So don’t think units, think just dollars.

And then you look, as Doug noted, at things like the fact that we’re growing as a company that we’ve got less in stock next year, and you normalize for all of that, you whittle that down to about $1.5 billion of inventory that if we can just wave a magic wand, we’d make go away today.

Rising out of stocks hurt the company early in the pandemic. To compensate, the company placed massive orders in 2021. The company was left with a glut of apparel after rising interest rates reduced inventory turnover. Unlike Target, who ripped the band-aid off and marked down all extra inventory immediately. Walmart is taking a more targeted approach. The last quarter was apparel, with electronics being added to the list moving forward.

Spiraling inventory had some hidden costs as well. The company increased the number of shipping containers in the system as it scrambled to meet demand. “We’re making good progress in reducing costs,” management said, confirming it had halved the metric.

- Utz Brands uses a fast follower strategy to grow sales

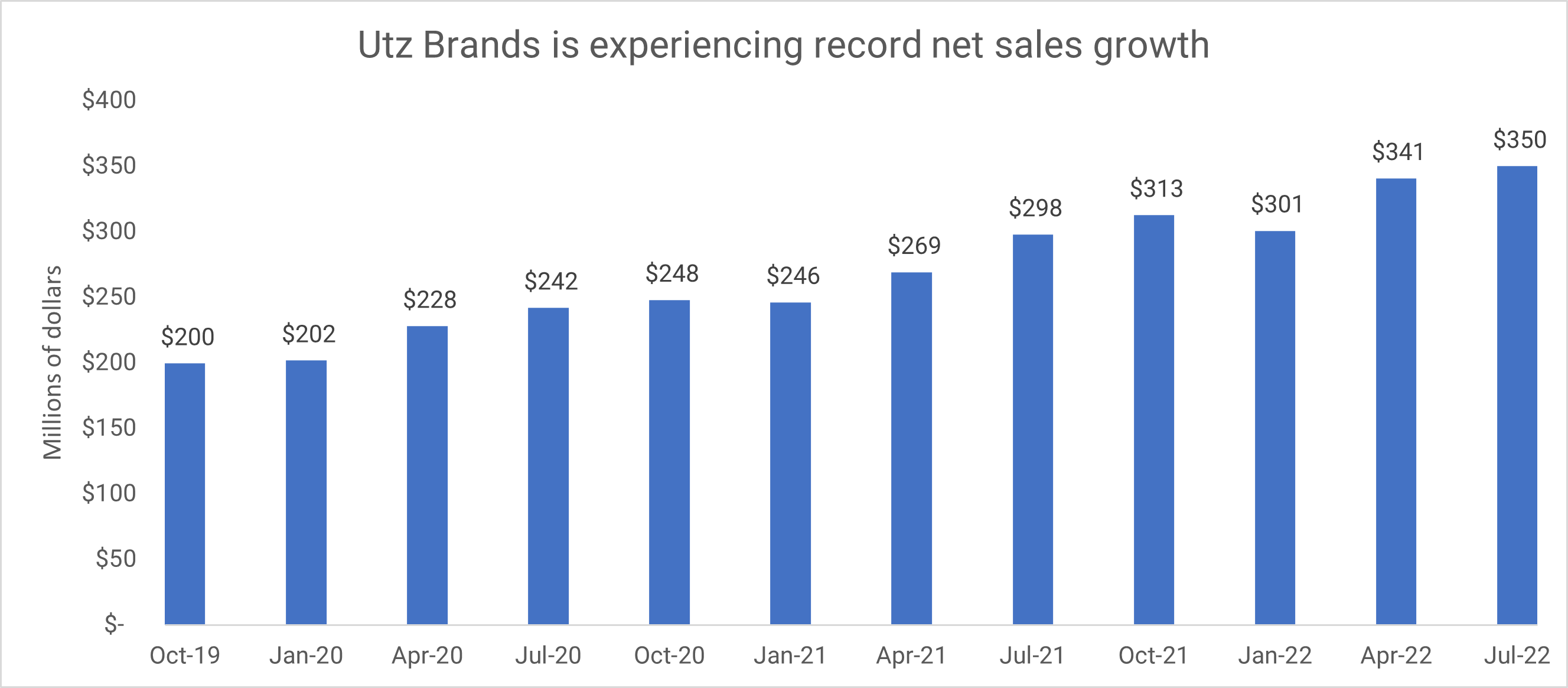

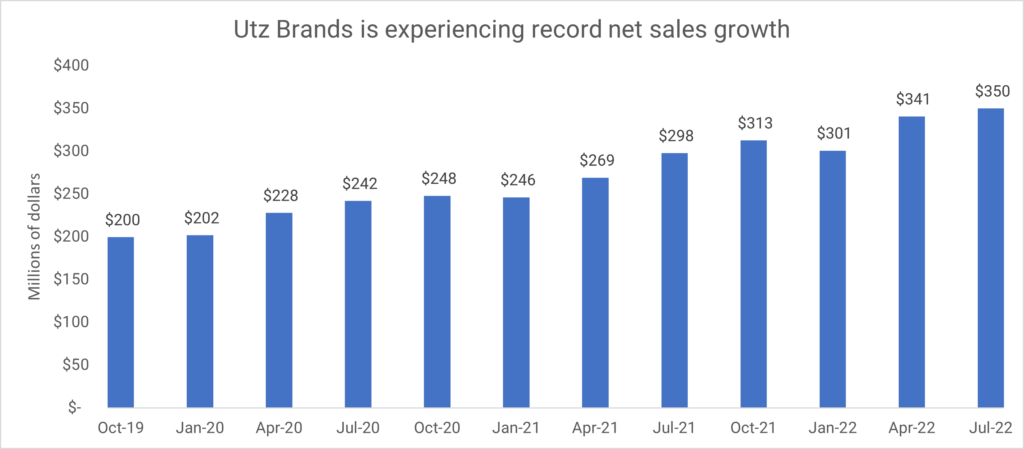

Utz Brands, the Pennsylvania-based company behind Utz and ON THE BORDER chips, delivered record net sales this quarter. During Q2 2022, Utz produced net sales of $350m, an with organic sales increasing 13.6% from the prior year. Most impressive, the company grew its category share. For the 13 weeks ending on July 3, retail sales grew 16% versus an overall category increase of 14.8%. Based on the success and limited price elasticities, Utz raised sales guidance for the year. “We now expect total net sales to grow 13% to 15% and for organic net sales to grow 10% to 12%,” CEO Dylan Lissette told investors on the earnings call.

One of the biggest standouts is the ON THE BORDER brand, which grew 15.4% in the quarter. The company bought the tortilla chip brand in 2020. Today, management estimates that it’s a $350m a year brand and projects it to grow to $450m. Not bad for an investment of $480m.

The Fast Follower Strategy

The fast follower strategy is a common strategy within the CPG world. Here, second-tier brands mimic the strategies and pricing of dominant brands. They get away with it because they’re typically lower priced. Companies maintain reasonable margins because they spend less on R&D. Utz Brands will never have the first exciting entrant in a category, but they’ll always follow shortly after.

Back in June Ajay Kataria, EVP & CFO, of the company, spoke about the strategy with price increases.

So really the entire category has been taking prices multiple rounds in the last 12 months. And the good thing about our salty snack category, it has a very rational category leader, which has an outsized share of the category. And they have been moving price up to cover inflation, and we have been fast following the category leader. And we have been sort of activating pricing as necessary to close the gaps where we see them, and that’s been the plan.

And we have taken three sort of broad-based rounds of pricing Q4 last year, February this year, and then again May this year. And then in between, we have been taking sort of closing the gaps, optimizing mix, doing things here and there across customers, across subcategories and product portfolio that we have.

And we are seeing us do that, and we’ve seen competition do the same. There have been at least three rounds of broad-based pricing in the last 12 months. And then people have been moving up packages and optimizing mix as necessary.

He continued the discussion when talking about the company’s trade promotion plans. Like most consumer goods companies, Utz cut back on promotional activity through the pandemic. Now that things are normalizing, will they increase spend to drive share?

We have found is we have been in lockstep in terms of how we are promoting, where we are promoting with the competition, with the category leaders in every subcategory.

And in most cases, it’s not the frequency of promotions that have come off the table. It’s the depth. So if we were running two for fives before, we were running two for sixes late last year. And we are up to two for sevens now, et cetera — is an example.

So I would say, we are in lockstep with the category leaders. But we are being mindful of what works on the shelf. If you go cold on promotions, that does not work with the consumer. You just have to work with the depth and the form of the promotion as well.

So not really. Utz management will watch and mimick how Frito-Lay approaches promotions.

Just don’t call them a budget alternative. When asked if being a lower-priced alternative for consumers resonated with retailers, here’s what CEO Dylan Lissette had to say.

We’ve never positioned ourselves as a lower price alternative to any of the more national brands.

Sure. Just don’t tell anyone on your strategy or pricing team.

- Lancaster Colony reports a poor Q3, but it has good problems

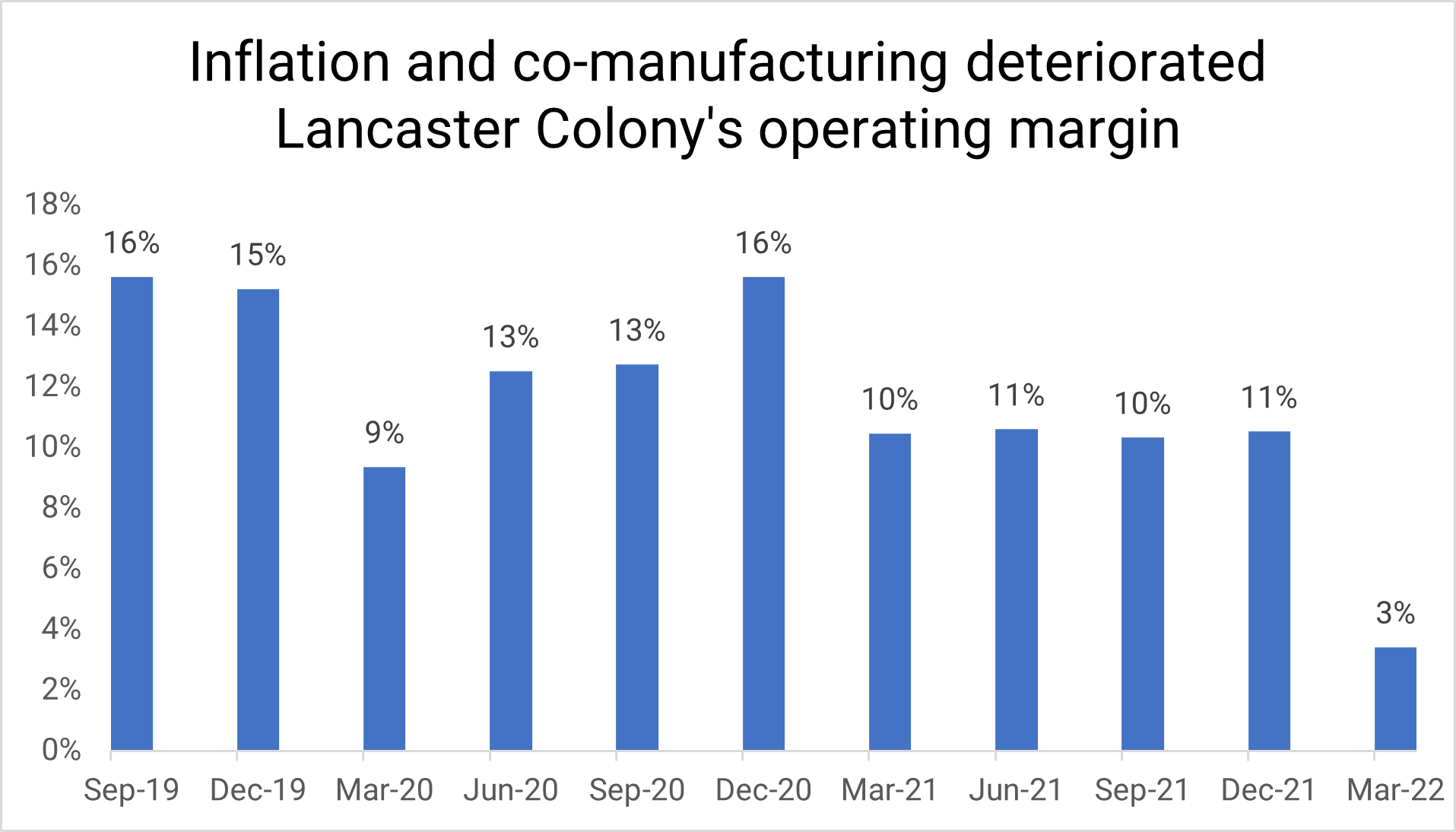

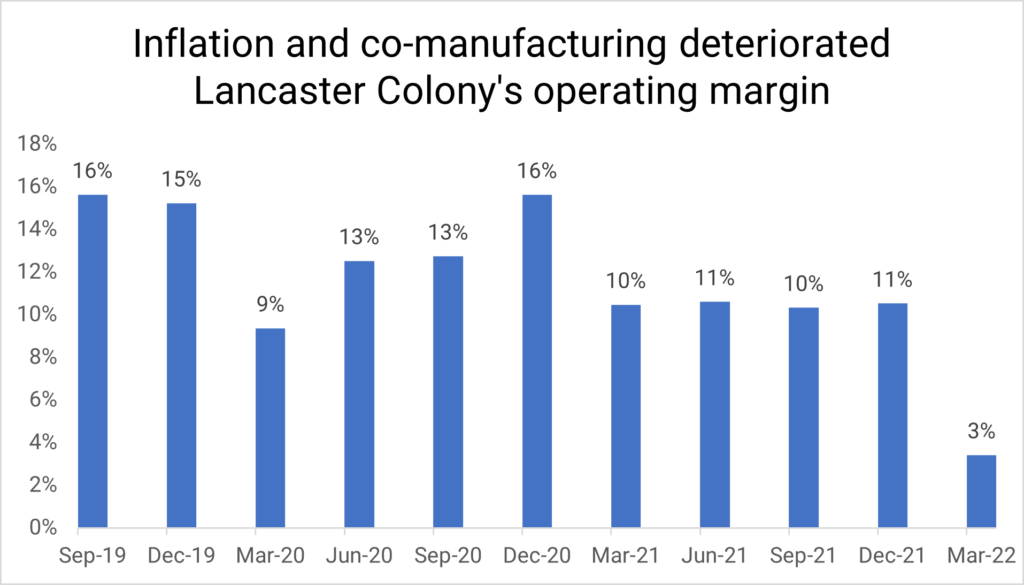

Lancaster Colony reported poor earnings in Q3 of 2022. Sales increased about 13% for the quarter, but gross profit declined by $22 million. The Ohio-based company, most known for its Marzetti salad dressing brand, faced a perfect storm of negative headwinds. Rampant commodity inflation, combined with a reliance on co-brands and co-packing, devastated the company’s margins. The operating margin for the quarter was about 3%, down from 10% the previous year. “Our third quarter financial performance fell short of our expectations,” CEO Dave Ciesinski told investors, “We have the action plans underway to help us overcome the many challenges of the current operating environment.”

Marzetti isn’t unique in facing high commodity costs. It is unique in that it’s been severely impacted by Russia’s invasion of Ukraine. Soybean oil, a key component in salad dressing, reached its highest price ever. The US dominates the soybean oil market, but sunflower oil shortages (Ukraine is a major player), have sent others scrambling for substitutes. “The soybean oil increase drove approximately half of our commodity cost inflation,” CFO Thomas Pigott said.

Marzetti’s licensing platform boosted sales while destroying margin. Lancaster develops, produces and markets a variety of licensed sauces for Olive Garden and Chic-Fil-A. Sales for the platform have tripped in the past two years—from $29 million to $89 million. Marzetti pays the brand partners a royalty on each item, and incredible sales require management to utilize co-manufacturers to meet demand. The company should be able to migrate from the co-manufacturer model this summer, as a planned line extension is scheduled to complete this past June.

Margin should recover in Q4, as the company experiences benefits from the new production line and price increases take effect. Management is also looking to potentially reformulate entire products to combat inflation.

Ciesinksi explains:

But given the nature of this inflation that we’re seeing, particularly around things like grains and oils, we’re finding that it’s increasingly important to look beyond just the way we’re manufacturing our product to look and go in to look at the intrinsic nature of our products, ourself. We’re looking at, hey, are there ways that we can lightweight plastic in our bottles? Are there ways that we can down gauge the corrugate in our boxes? And we’re also actually even looking at formulas to say, are there things that we can do to the formulas that won’t be considered a diminution of value to the consumer, let’s say, and the way mom experiences the product.

Honestly, most of these problems are good problems to have. Using co-manufacturers to meet massive demand is a problem that can be solved in-house over time. Reformulation can drive lasting value. If things go as planned, the company could leave the COVID era in better shape than it started.

DISCLOSURE – I was previously involved with a strategy project at Lancaster Colony. I no longer have any connection to the firm.