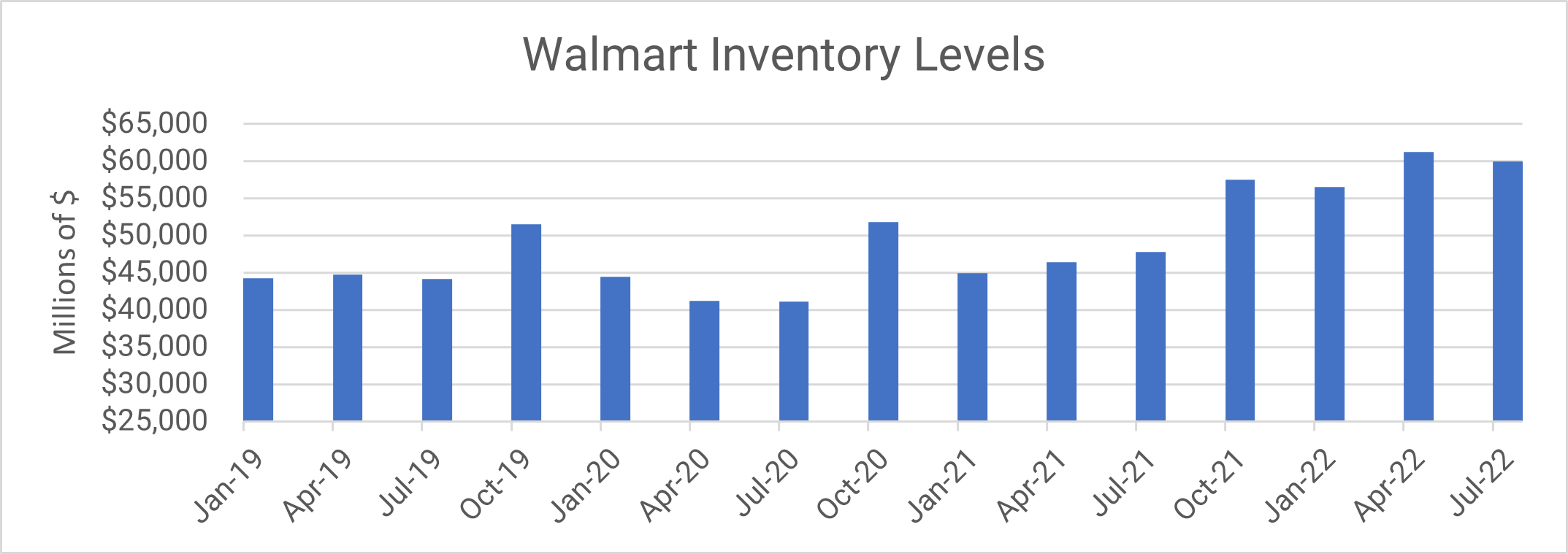

Weeks after lowering sales guidance, Walmart delivered reasonable sales growth amid heightened inventory levels. America’s largest retailer saw U.S. sales grow 6.5% compared to the previous year’s quarter while increasing in-store fulfillment for online ordering by nearly 40%. Management noted a fair number of shifts in consumer behavior, with shoppers trading from deli meats to canned tuna. “We finished the quarter on a strong note,” CFO John David Rainey told investors on the call.

A new normal for Walmart Inventory Levels?

Last quarter the company announced it was going to aggressively mark down apparel after forecasting errors flooded the company’s warehouses with unneeded items. “We’ve made good progress to reduce inventory levels where we’ve focused and taken markdowns,” CEO Doug McMillion said. Inventory is down from last quarter’s high, but still almost $15 billion higher than the pre-pandemic era. The absolute number is slightly misleading, as a fair amount of the cost is inflation related. McMillion explained:

Take the U.S. inventory increase in the second quarter of $11 billion. If you decompose that, about 40% of that is due to inflation. So don’t think units, think just dollars.

And then you look, as Doug noted, at things like the fact that we’re growing as a company that we’ve got less in stock next year, and you normalize for all of that, you whittle that down to about $1.5 billion of inventory that if we can just wave a magic wand, we’d make go away today.

Rising out of stocks hurt the company early in the pandemic. To compensate, the company placed massive orders in 2021. The company was left with a glut of apparel after rising interest rates reduced inventory turnover. Unlike Target, who ripped the band-aid off and marked down all extra inventory immediately. Walmart is taking a more targeted approach. The last quarter was apparel, with electronics being added to the list moving forward.

Spiraling inventory had some hidden costs as well. The company increased the number of shipping containers in the system as it scrambled to meet demand. “We’re making good progress in reducing costs,” management said, confirming it had halved the metric.

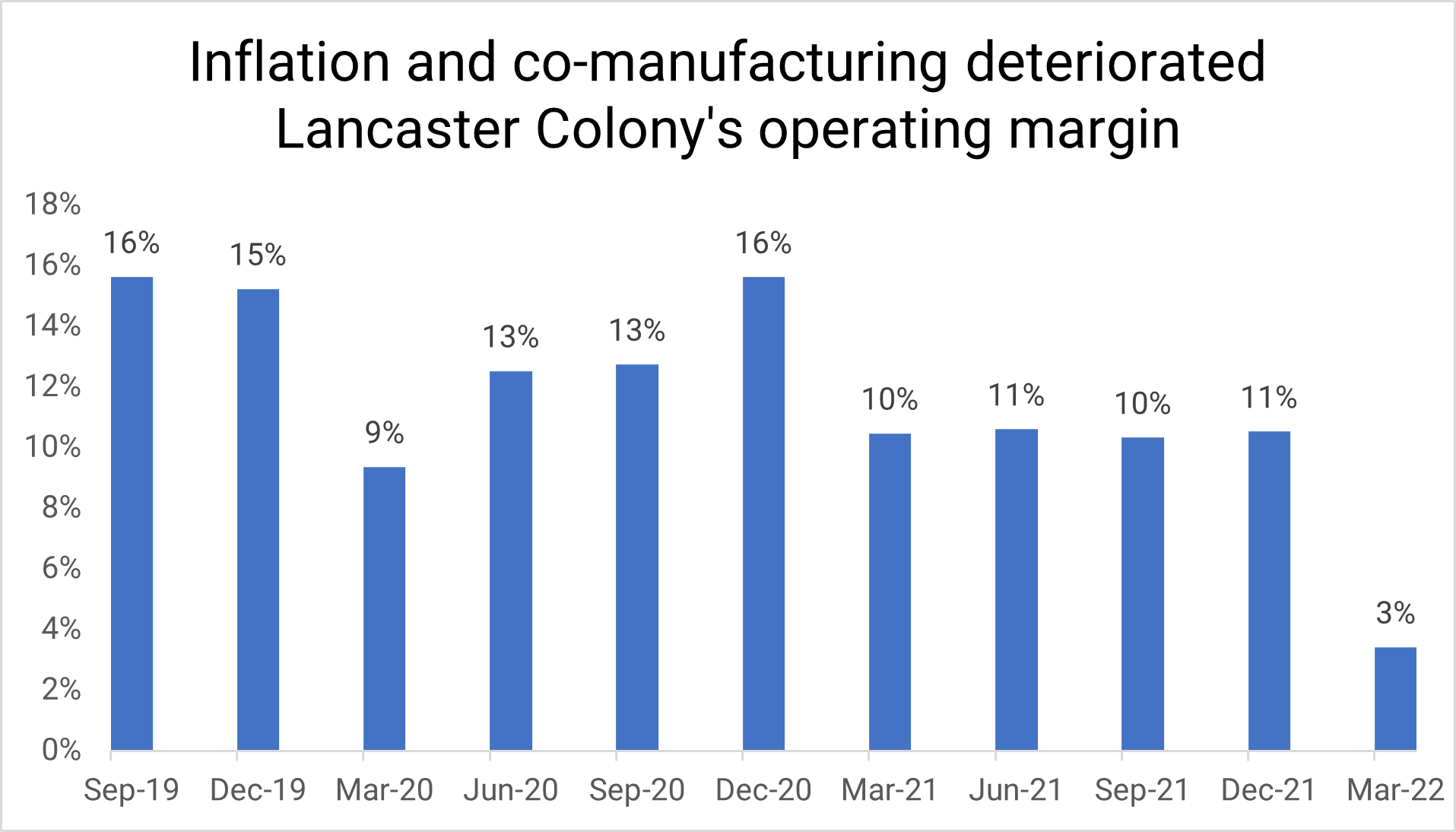

Lancaster Colony reported poor earnings in Q3 of 2022. Sales increased about 13% for the quarter, but gross profit declined by $22 million. The Ohio-based company, most known for its Marzetti salad dressing brand, faced a perfect storm of negative headwinds. Rampant commodity inflation, combined with a reliance on co-brands and co-packing, devastated the company’s margins. The operating margin for the quarter was about 3%, down from 10% the previous year. “Our third quarter financial performance fell short of our expectations,” CEO Dave Ciesinski told investors, “We have the action plans underway to help us overcome the many challenges of the current operating environment.”

Marzetti isn’t unique in facing high commodity costs. It is unique in that it’s been severely impacted by Russia’s invasion of Ukraine. Soybean oil, a key component in salad dressing, reached its highest price ever. The US dominates the soybean oil market, but sunflower oil shortages (Ukraine is a major player), have sent others scrambling for substitutes. “The soybean oil increase drove approximately half of our commodity cost inflation,” CFO Thomas Pigott said.

Marzetti’s licensing platform boosted sales while destroying margin. Lancaster develops, produces and markets a variety of licensed sauces for Olive Garden and Chic-Fil-A. Sales for the platform have tripped in the past two years—from $29 million to $89 million. Marzetti pays the brand partners a royalty on each item, and incredible sales require management to utilize co-manufacturers to meet demand. The company should be able to migrate from the co-manufacturer model this summer, as a planned line extension is scheduled to complete this past June.

Margin should recover in Q4, as the company experiences benefits from the new production line and price increases take effect. Management is also looking to potentially reformulate entire products to combat inflation.

Ciesinksi explains:

But given the nature of this inflation that we’re seeing, particularly around things like grains and oils, we’re finding that it’s increasingly important to look beyond just the way we’re manufacturing our product to look and go in to look at the intrinsic nature of our products, ourself. We’re looking at, hey, are there ways that we can lightweight plastic in our bottles? Are there ways that we can down gauge the corrugate in our boxes? And we’re also actually even looking at formulas to say, are there things that we can do to the formulas that won’t be considered a diminution of value to the consumer, let’s say, and the way mom experiences the product.

Honestly, most of these problems are good problems to have. Using co-manufacturers to meet massive demand is a problem that can be solved in-house over time. Reformulation can drive lasting value. If things go as planned, the company could leave the COVID era in better shape than it started.

DISCLOSURE – I was previously involved with a strategy project at Lancaster Colony. I no longer have any connection to the firm.

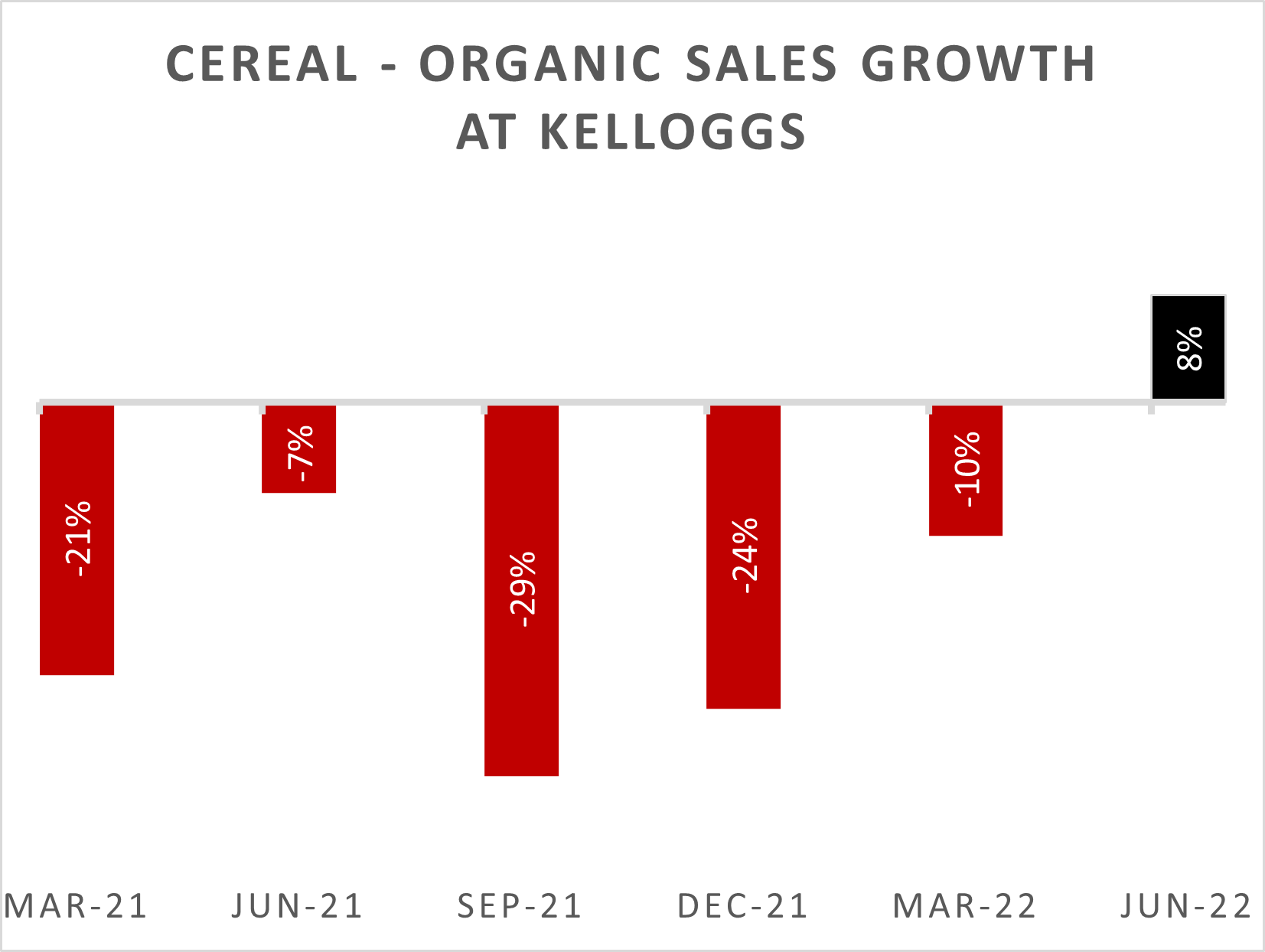

Kellogg Co. was the latest in consumer goods giants to raise sales guidance after demand remained relatively elastic after numerous price hikes. The Michigan based company, who manufacturers a variety of cereals, Eggo waffles, and snacks like Cheese It, now predicts 4-5% operating profit growth—up from the 1-2% predicted earlier this year. “We feel good enough about our business,” CFO Amit Banati told investors, “That we can today raise our full year guidance on all key metrics while using our strong cash flow to both return more cash to shareholders and preserve a strong balance sheet.”

The biggest Kellogg Co. news of the year is that management plans to split the company into three separate companies: Cereal, Snacks, and plant based. Snacks has been the company’s key performer of the last few years. It has generated most of the company’s growth and commands the most attention from management. That attention is a key driver for the decision. In the future, CEO Steven Cahillane predicts that, “Frosted Flakes does not have to compete with Pringles for resources.”

Independently, cereal should be a strong business—well at least the way Cahillane framed it to investors last week.

We have 5 of the top 11 brands. They are strong brands. All the information, research and data that we have suggests or reinforces how strong these brands are, how relevant they are. The category, as you know right now, is very healthy. It’s showing incredible pricing power. Even the last 4 weeks is better than the last 13 weeks. The category is quite healthy. It’s versatile. It’s showing, especially in challenging times, that it is a very affordable meal for people. A bowl of cereal with a glass of milk is $1, and that’s really helping the category.

He believes that because of the firm’s focus on snacks, it has been underinvesting in cereal. Despite this under investment, the category as a whole is up 9% on the quarter. It’s rival General Mills regularly delivers 20% margins on the product, so it’s reasonable to assume that Kelloggs could get there. Prior to this quarter, North American organic sales for Kellogg’s cereal were, quite frankly, a disaster. Partly driven by a return to the pre-COVID norm, but also made worse by Kellogg’s management’s inability to manage labor relations, the company hemorrhaged share and millions of dollars.

P&G delivered fine earnings for the fourth quarter of 2022. The company behind Tide, Pampers, and Head and Shoulders shampoo earned $19.5 billion in the last three months, an increase of 3% from last year. Like most CPG companies, the big sales driver was price. The company used an 8 percent price increase to compensate for a 1% decrease in volume. From a profitability perspective, gross margin decreased by under 4 percent for the quarter. The primary culprit was an increase in commodity and freight costs. The company predicted about $3.3 billion in additional costs for the next year for the two. “We’re working to mitigate the impact of these cost headwinds,” CFO Andre Schulten said. The company will use “a combination of innovation to create and extend the superiority of our brands, productivity in all aspects of our work, and pricing.”

One hidden area of productivity is advertising spending. According to management, P&G has been incredibly successful at generating more impact without increasing spend. “We have delivered significant productivity over the past years,” Schulten said. Since it’s P&G one of the strongest brand managers in the world, the company took the efficiency savings and reinvested them in more advertisements. The composition of the spending is also telling. P&G revealed that “more than 50% of our advertising is in digital.” In 2021, P&G spent $8.2 billion on advertising. More than $4 billion was once earmarked for television, radio, and print and is now spent with Facebook, Google, and Amazon.

The efficient advertising is paying off for the company. There’s a general trend migrating towards private label—P&G hasn’t seen that yet. Outside of paper products and family care, management doesn’t forecasting much competition from private label moving forward. “Overall,” Schulten concluded, “we’ve been able to drive share growth on an all-outlet basis.”

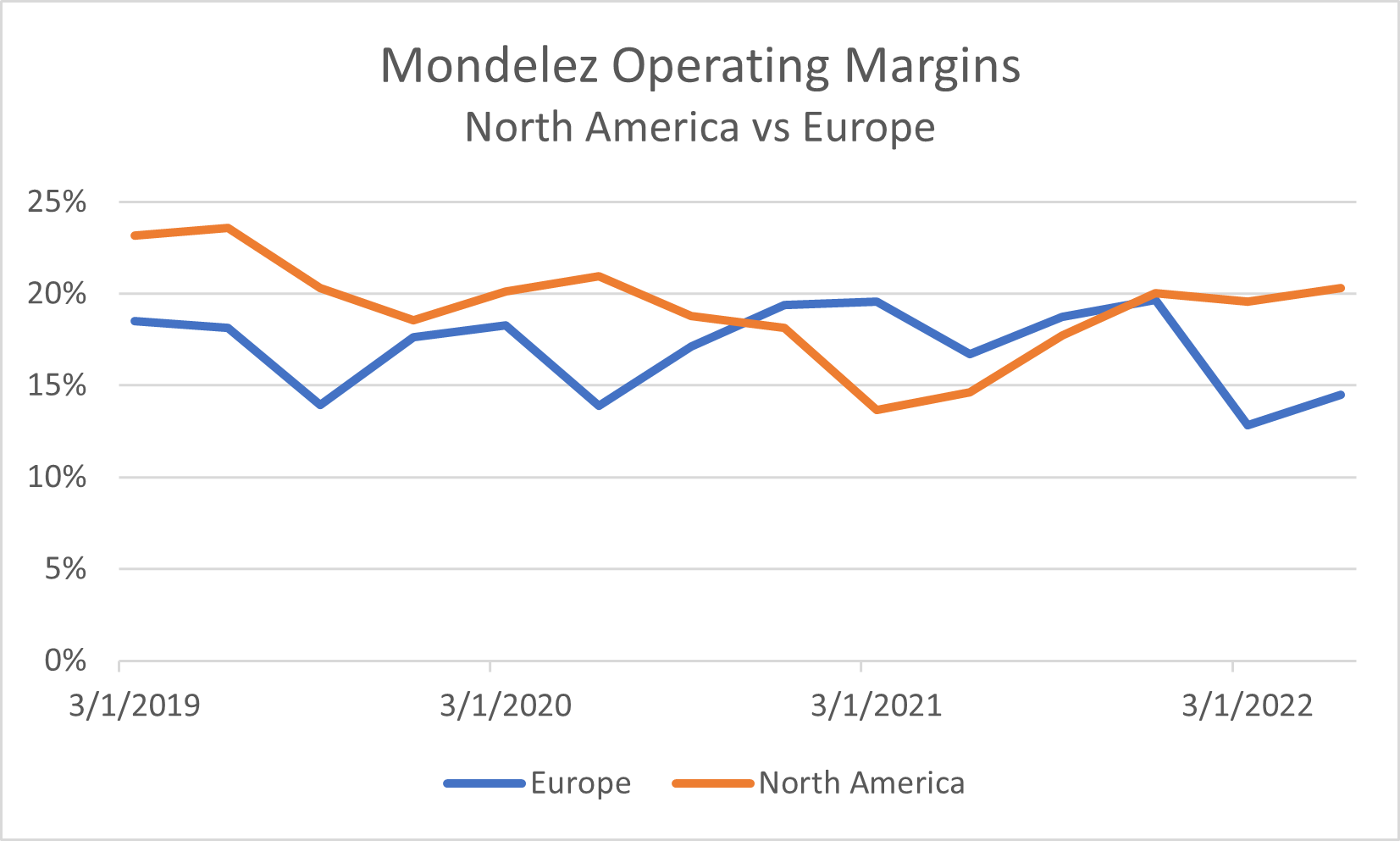

In Q2 of 2022, Mondelez delivered exceptional results, increasing quarterly organic net revenue by 13.1% to $7.2 billion. The great news for Mondelez is that the maker of Oreo and Wheat Thins saw both price and volume increase by 8% and 5.1%, respectively. “Our core chocolate and biscuit businesses continue to demonstrate volume and pricing resilience,” CEO Dick Van de Put said, “As consumers worldwide continue to seek out our trusted and iconic brands to meet their snacking needs.” Based on the outlook, the company raised guidance to 8% for the year.

One interesting thing to watch is that management signaled that the company was facing margin pressure from being unable to sell in European price increases. That’s because generally speaking, Europe is a more difficult operating environment for manufacturers selling in price increases. Part of this is Europe’s more active regulatory enforcement leading retailers to push back against passing on inflationary costs to consumers proactively. The other is that retailer pricing contracts are typically two years in Europe, offering significantly less flexibility for price spikes.

Europe and U.S. margins have taken turns leading the way throughout the pandemic. Although in the last two quarters, North American operating margins have run around 20% while European lag behind at 14%. According to management, about 35% of the second wave of price increases in agreed upon in Europe. In America, it’s 100%, with an eye towards more. “More pricing has to happen,” the CEO concluded, “Most of it has been announced, and we’re now in the discussions and implementation of it.”

Coca-Cola management reported the company’s second quarter 2022 results this morning. The Atlanta-based sparkling beverage company grew organic revenue by 16% compared to the same quarter the year before. Management said that price/mix actions caused 12% of the growth—and attributed more than half of that to mix changes. Consumers are migrating towards higher-margin products post-COVID, including smaller package sizes.

The company has utilized RGM to manage inflation. Management reported that the comparable operating margin dropped 1.7% to 30.7%. Despite the slight decline, it’s still 10% higher than the average non-alcoholic beverage company. CEO James Quincy mentioned that the company has tried to pass on all commodity increases to consumers, but it has scheduled price increases to lag inflation.

The hidden check against inflation at Coca-Cola

Unlike other CPG companies, Coca-Cola’s distribution system is somewhat of a check against inflation. For bottled products, Coca-Cola sells syrup to bottling partners, who then sell finished goods to retailers. Cost increases will be absorbed by the bottlers first. That means there is a group with significant bargaining power to push back against greed-inflation.

Image via Datasembly

The company has no plans to rollback pricing if inflation steadies. “Basically, for the price to roll back, we need the overall economy to enter deflation,” Quincy said. According to data from Datasembly, beverage costs have increased by around 20% since the pandemic’s start. If Quincy has his way, these high costs may be the new normal for consumers. “Price rollbacks seem very unlikely.”

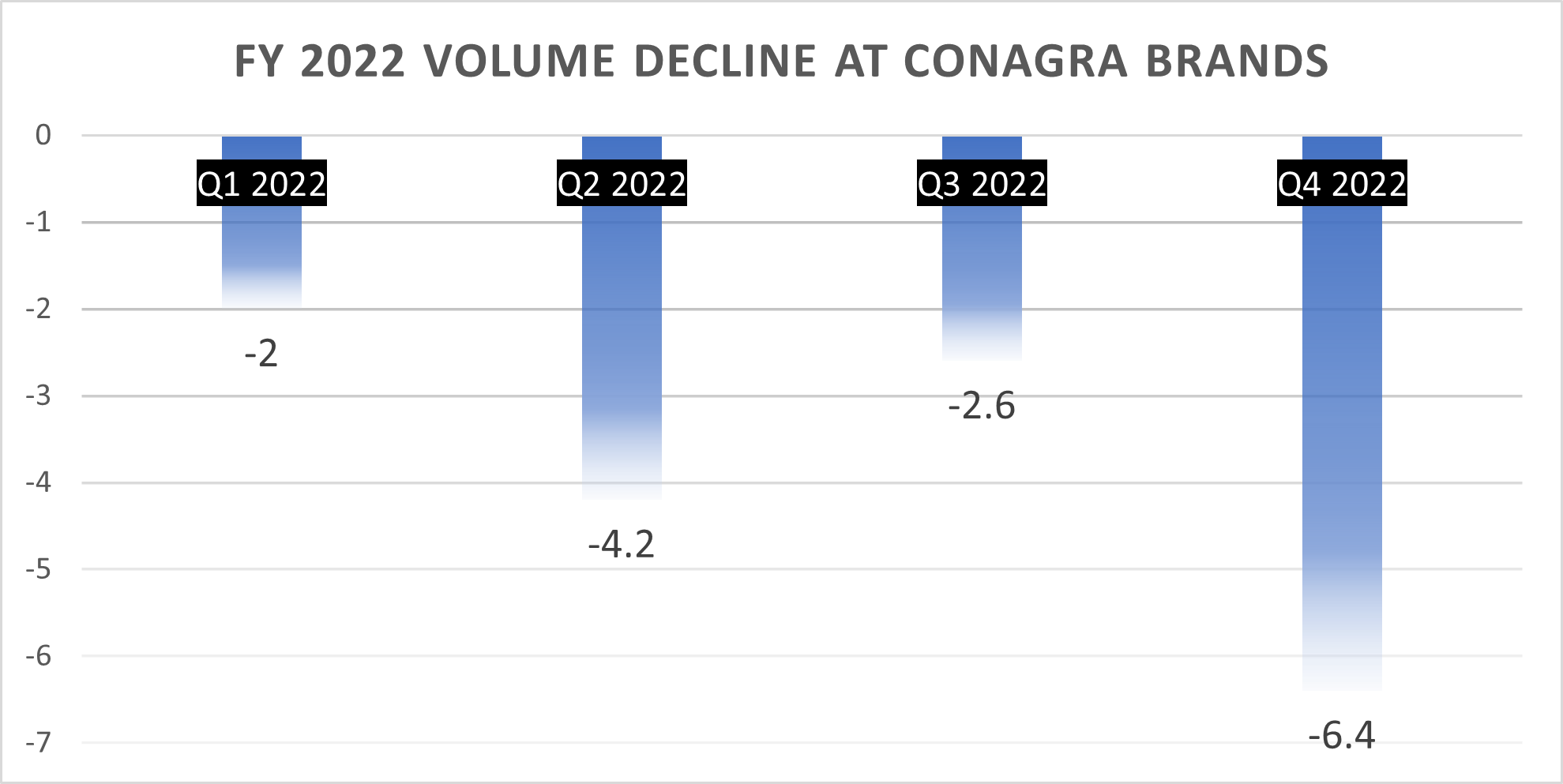

Management at Conagra Brands said that in the next two quarters, it has more price increases planned even though price increases are beginning to impact volume materially. In Q4 of 2022, the maker of Slim Jims and Birds Eye frozen foods saw sales decline by 6.4%. That marks four consecutive quarters of volume loss.

However, the volume was more than offset by a 13.2% price/mix improvement. The company reported a net sales increase of about 3% for the fiscal year, while operating margin compressed down 400 basis points to 11.7%.

There was a bit of awkwardness in the call. The management team, led by CEO Sean Connolly, focused the discussion on supply chain constraints. “While we are making progress in supply chain, the constraints are still with us.” Connolly told analysts in this weeks’ investor call, “And they were still a factor in Q4 and we did see retailers burn through inventory faster than we could replenish it.”

However, not all analysts were sold on the framing.

Analyst: Okay. And maybe a follow-up, in your press release, when you talk about the reasons for the volume decline, it really is all about price elasticity. It doesn’t say anything about supply chain constraints or inability to serve customers. So is it just not material enough to show up in the price release that supply chain constraint?

Dave Marberger: Yes, just I would just add when you do the press release, obviously, you talk more about the material drivers of the thing, right? So it’s clearly elasticities are the main driver of volume. There were some supply constraints, which we gave color to because we were asked. So — but the main driver were the elasticity.

Perhaps the most interesting conversation came towards the end of the call, when Wall Street grew somewhat skeptical of the announced pricing plans.

Analyst: I’m in an event right now with a lot of your customers. And it’s kind of depressing. They’re talking about all this cost pressure, the limited ability to pass it through the consumer, the meaningful margin squeeze they are under. And you’re the third food company in a row to get up and talk about the ability to price above inflation and get margin recovery, which we saw this quarter you’re guiding to for next year. It kind of flies in the face of how I’ve always thought about the balance of power between the industry.

Was it may be a bit more balanced rather than the sort of incongruent balance that we’re seeing right now where CPG guys are saying they’re going to flex a lot of muscle, while your customers are feeling a lot of pain. What’s evolved to kind of cause that balance to pivot in this direction? And why do you believe it’s durable?

Sean Connolly: No, I wouldn’t characterize it the way you’re characterizing it, Jason. I mean when you go into these macroeconomic dislocations that we’ve experienced, the pain tends to come in waves. And manufacturers get hit with a lot of the pain early in the cycle, and that comes in the form of margin compression as you’ve seen we’ve gone through in the last year, a lot of that associated with the lag effect. And then the lag effect is a transitory effect that you do emerge from. So it’s not as if what you’re doing as you move through that cycle is you’re recovering lost margin points as opposed to adding fresh new firepower at the profit line. That’s not what’s happening.

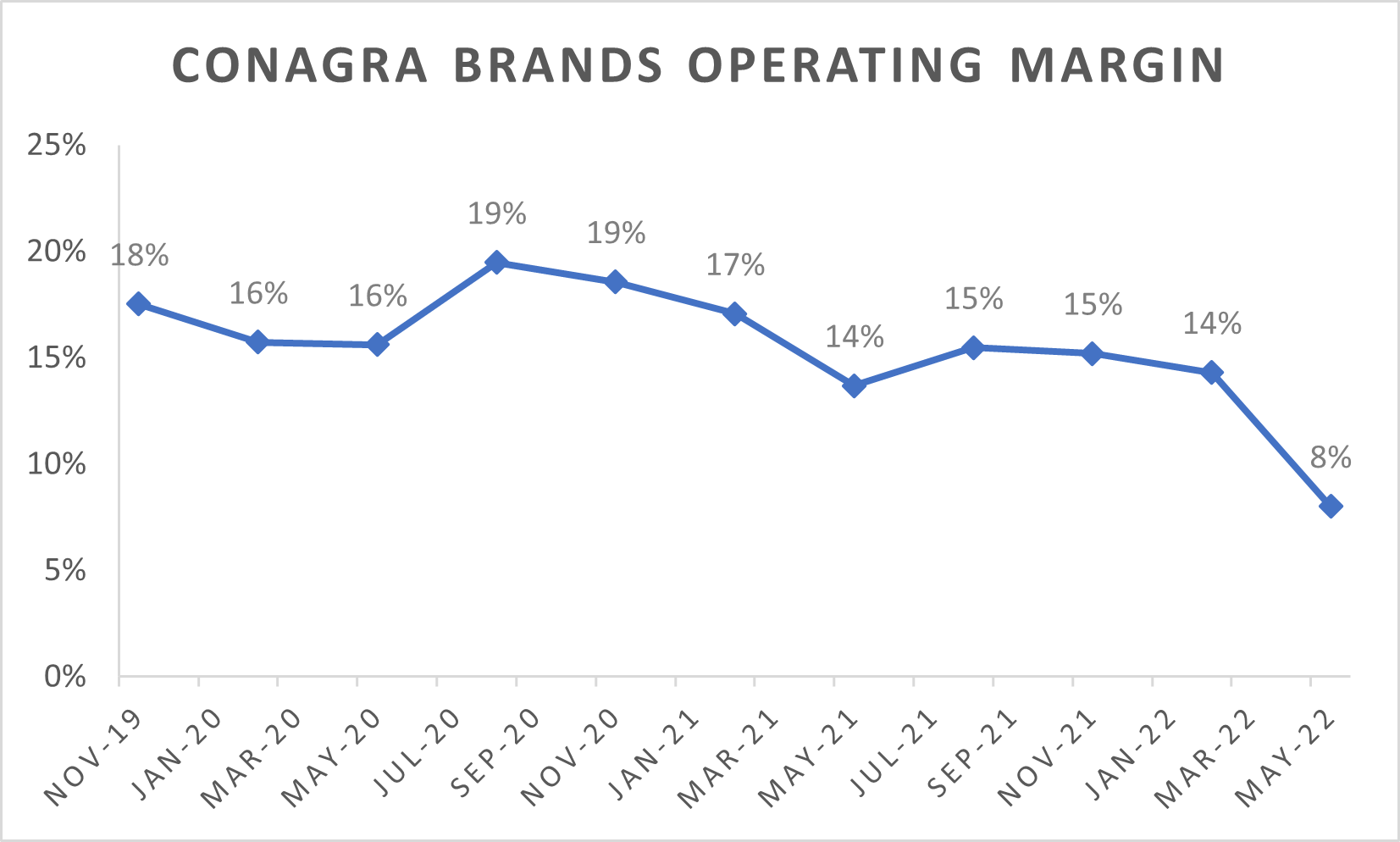

I’m somewhat with Connolly here. Conagra Brands has experienced significant margin compression. After boosting margins for a few quarters at the start of the pandemic, inflation caught up to the company. According to data from Seeking Alpha, in FY 2021, the company had operating margins of about 18%. In FY 2022, that number compressed to 12.2% (higher than the company’s reported number).

Where I somewhat lose him is his additional rationale.

This is about profit recovery. And that’s an important thing. Manufacturers have to recover their margin, why? Because the top priority for our retail customers is growth. And our retail customers here at Conagra know that our innovation has been the absolute key to driving growth for their categories. They need and want that innovation to continue, but they know that, that innovation costs us money. We have to have healthy margins to be able to build out that innovation and get it to our customers in the market. And so they know we’ve got to take inflation justified pricing to recover our margins after we go through these windows where we experienced the compression that happens early in the inflation cycle. And that’s exactly kind of how things are playing out.

So I’m not opposed to companies regaining margin. However, in 2021 Conagra Brands sold about $2.8 billion in consumer staples. Americans eat these products daily: Hunts canned tomatoes, birds-eye frozen vegetables, peanut butter. I’m sure they’ll use some level of RGM to minimize the pain, but raising staple prices above inflation to bring new Reddi Whip options to retailers seems…not great.

Kroger, America’s largest pure-play grocer, reported another consistent quarter. For its first quarter of 2022, the firm matched the previous year’s 4.1% percent sales growth while increasing operating margins. The big news is the composition of the company’s sales. For the first time in the pandemic era, private label led the way. According to management, sales of Kroger’s own brands increased by 6.3%–outpacing all national brands.

During the quarter, we saw tremendous growth in Our Brands, which had identical sales of 6.3% and outpaced all national brands. With 92% of households purchasing at least one of these products, we launched 239 new and innovative products during the quarter, reflecting many of the top food trend predictions we made at the beginning of the year. All of our new products continue to be tested and validated to ensure that they are as good or better than the comparable national brand.

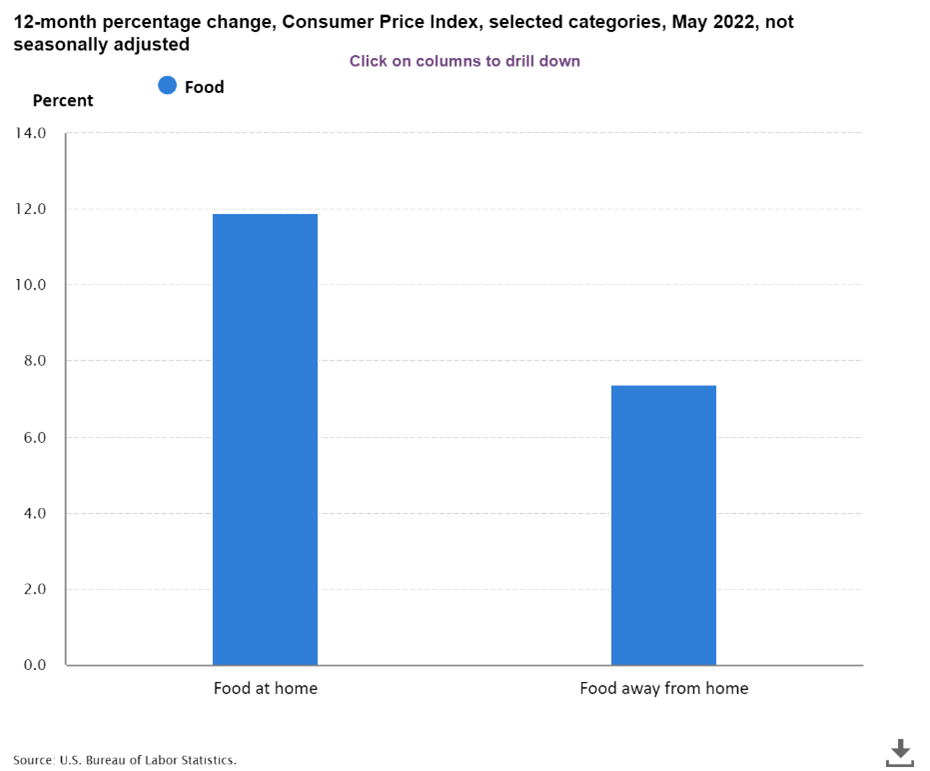

What’s interesting is why this is happening. Of course, rising inflation is impacting wallets. According to the Federal Reserve, the cost of at-home food increased nearly 12 percent since last May.

With no additional fiscal stimulus in sight, shoppers are looking for cheaper alternatives. However, an interesting component of the switch is supply constraints from branded CPG manufacturers.

McMullen explains:

I think there’s still a lot of capacity constraints among some of the national brands. So I would expect if it’s a national brand with capacity, you’ll see a typical trend where they get more aggressive in promoting as their tonnage goes down. But if they’re supply-constrained, I would be surprised. And part of that is just because all of us are exiting COVID at a level of volume higher than what we had going in, which has put different people at different points on supply constraints.

Essentially, the Campbell Soups and Smucker’s of the world can’t produce enough products to meet demand. Since sales are brisk, their management sees no reason to offer promotions that would normally make their products more price competitive and spur incremental volume.

The decision to cut back on promotions will also impact Kroger down the line. During the COVID-19 era, the company invested in new warehouse infrastructure. Unfortunately, it’s sitting somewhat idle as the lack of promotions means management doesn’t see an incentive to lock in lower prices through forward buying.

For its part, Kroger management announced that it has no plans to gain market share by taking price. “We always think it’s important to remember it’s the total customer experience that we’re focused on,” McMullen concluded, “rather than price alone.”

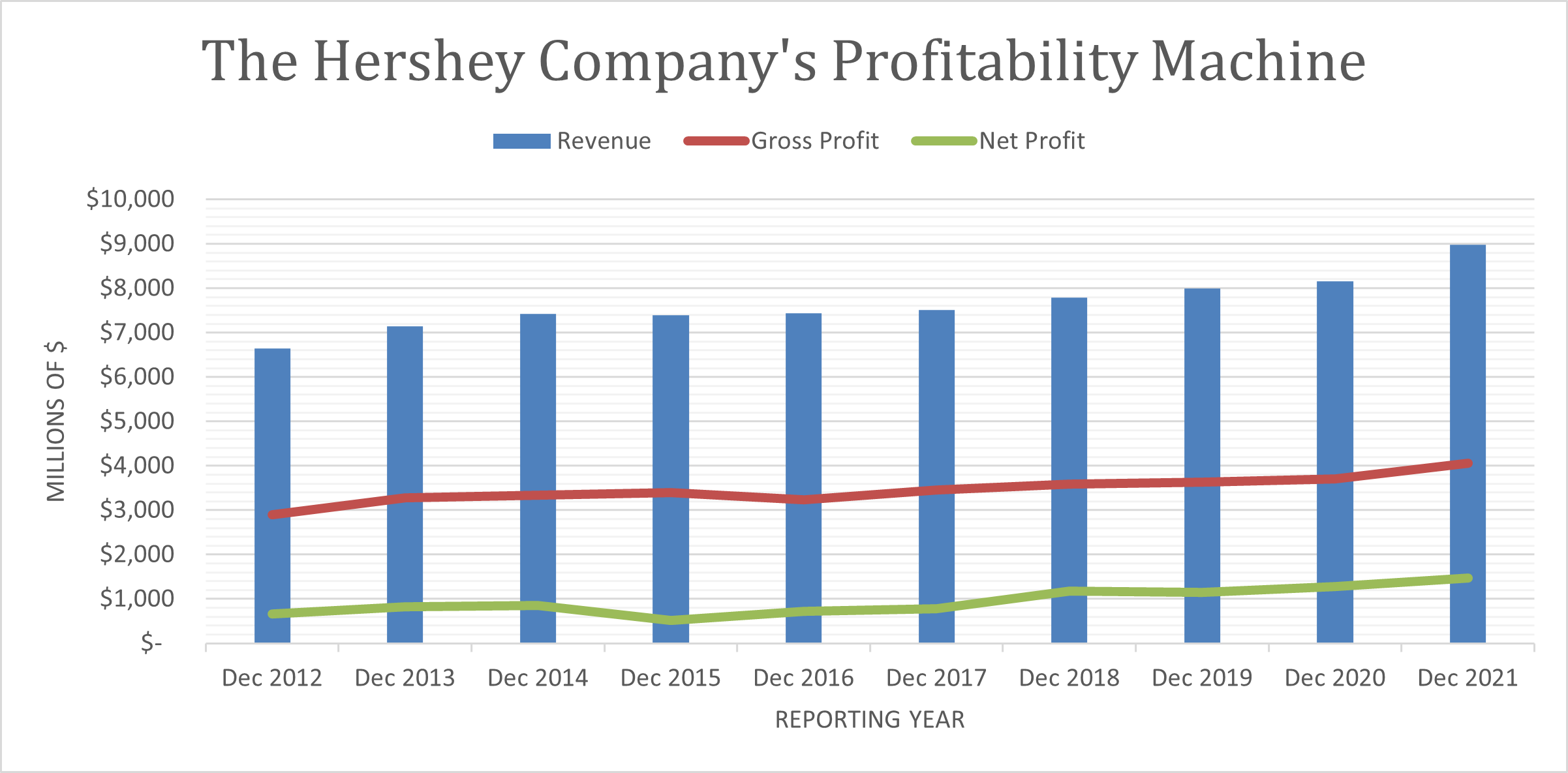

The Hershey Company, one of America’s oldest and most profitable food companies, may finally experience private-label competition. Founded in 1894, the Pennsylvania-based food processor has experienced over a century of nearly unrivaled success. Today, Hershey owns about 43% of the American chocolate market, with second place Mars commanding about 25%. This dominance enables Hershey to post nearly unrivaled margins.

Part of the success is due to great products and business execution; the other part includes an industry structure that makes it largely immune from private label competition. Hershey doesn’t face margin pressure from low-cost alternatives. A big component of this is distribution. Unlike other private label categories, candy distribution requires refrigerated trucks and is fairly labor-intensive to stock. It’s why Walmart uses McClane, rather than ordering directly. That underlying reality is why there aren’t many investors clamoring to produce lower-margin private-label alternatives.

And on your other question, we are constantly looking at a couple things relative to the strength of retail takeaway in other CPG categories, as well as our own. And also how much market share is going to private label as that has typically also been a predictor of the consumer. We’re fortunate in our category, not to have significant private label, but certainly in other categories where that’s present we do look at that as well.

At the same time, we do know that there’s significant pressure out there, and we just want to really keep our fingers on the pulse of it to make sure that we aren’t missing something. I mean certainly, we’re not a category where there’s a big private label component and people can easily just say, “I’m going to still participate but switch to lower brands.” That’s always been a benefit for us during times like this, but we do understand the pressure consumers are under.

This week, one of the faster-growing convenience stores in America announced it invested in private label offerings—and candy is a prime driver. Casey’s General Stores operates 2,400 locations across the Midwest. Unlike many other retailers, Casey essentially self-distributes 90% of its in-store products from its three warehouses. This gives it an incredible amount of control and leverage over the quality and presentation of merchandise..

You know, Anthony, we’re working on a lot of different categories right now in private brand. We actually participate in 26 different categories of private brands, and some of those are underpenetrated, some of those are more penetrated, but I can tell you where we’ve seen some success so far in the last quarter, we launched a line of Casey’s candy bars which is something we have never played in before, and they have become the number one standard size bar in dollars, units, and margins within the category. When I say that, I mean that’s outperforming Reese’s, Snickers, all of those national brands, and so I think it really illustrates the quality and the value that those products provide.

Sure. It’s one company and one example. Or it could be the start of private label candy gaining share in the convenience store channel.

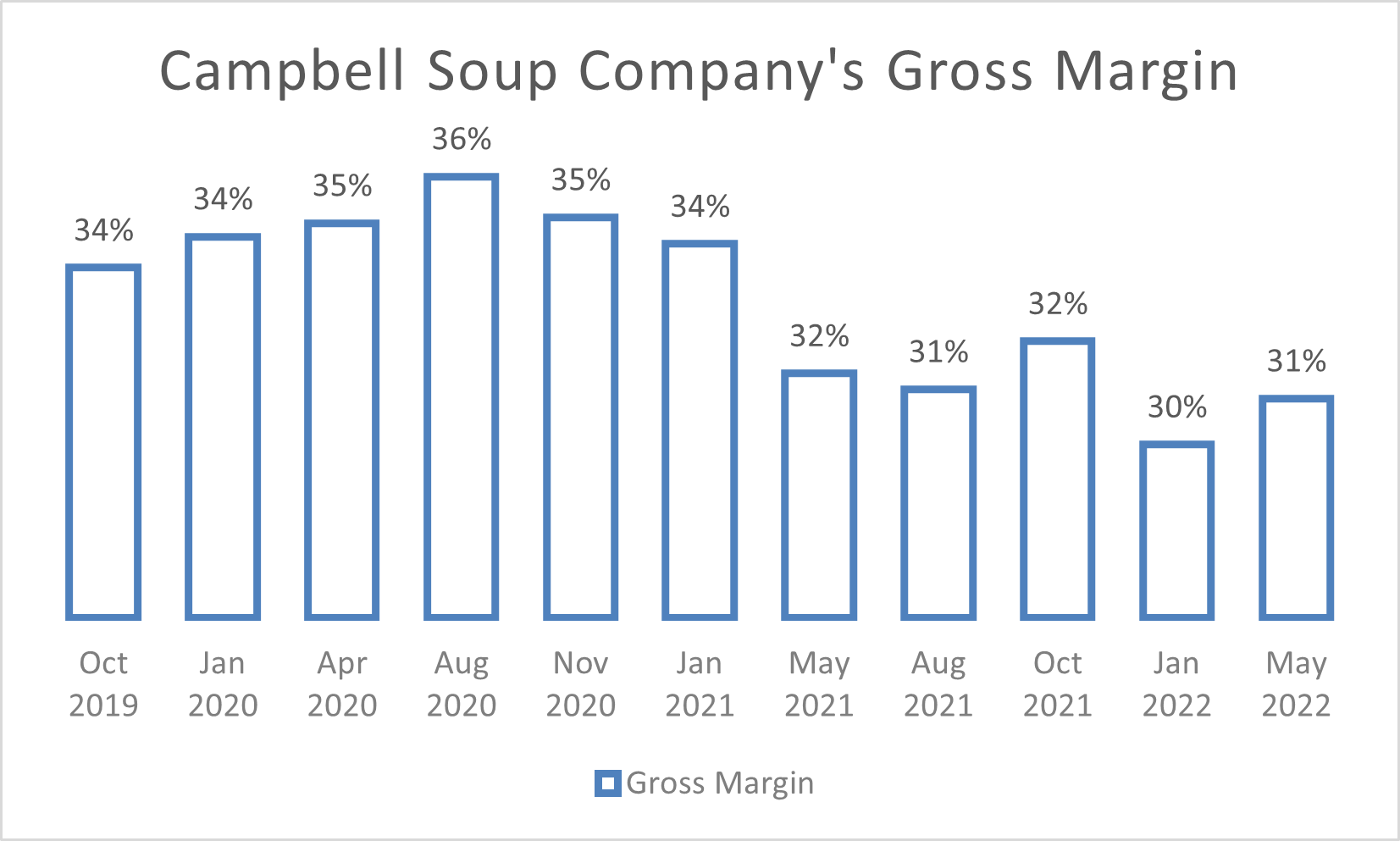

Campbell’s Soup Company, America’s dominant soup maker, had a solid third quarter after price increases generated almost a double-digit increase in net sales. In absolute terms, the company posted sales of $2.1 billion with overall gross margins of 31%. The company has maintained margins throughout the COVID era through price increases and efficiency programs. Unlike Tyson, there isn’t any overt evidence of price gouging in the third quarter.

Management predicts a strong end to the year due to successful innovation initiatives in crackers and leading brands in both the ready-made and condensed soup categories.

In the question and answer portion of the call, CEO Mark Clouse answered questions about trade downs within the consumer goods world. The CPI recently reached the highest level of inflation in almost 40 years. With no future stimulus spending expected, experts expect consumers to switch from branded products to private labels. Campbell management believes it’s well-positioned.

Let’s take condensed soup as an example, where we are seeing and expected to see some pressure from private label, you also have significant migration of trading down into the category. So that the overall category growth rates are up pretty significantly. And volumes are holding up very well, even in the face of pricing that can be double digits so far that we’ve seen.

I think what’s been new about this or what’s been a little bit more unique than maybe what we’ve seen in the past is where we’re experiencing more of the trade down tends to be more in the baby boomer, a little bit older consumer that tends to be a bit more price sensitive. And we’re picking up a lot of these new consumers as they are moving into the category. Another great example of that is Chunky. Chunky’s pricing is up mid-teens right now. And what we’re learning is, although that seems like a lot of pricing, and it is, but for can of soup, it’s still under $3 for a large part of the population trading down into the ready-to-serve soup category becomes a very economic move for them. And that’s why on Chunky, we see right now, pricing mid-teens, consumption’s up 14 but units are still up 3%. And our volume was up 8% in the quarter.

Clouse did not rule out additional pricing actions down the line.

Q: I guess, Mark, in light of recent industry chatter regarding consumer behavior shifts and retailer commentary, I thought it might make sense to start with having you address this sort of building investor notion that the pricing window has sort of, all of a sudden, effectively completely closed for the industry, which obviously is an important topic given expectations for more inflation to come in — going forward in your fiscal ’23.

A: And I think as you start to ask about future and this idea that there is no room for any more pricing, I don’t think that’s particularly accurate or realistic. I think what is true is that we’ve got to be incredibly mindful of the consumer dynamics and where consumers are relative to the elasticities that we’re experiencing and being quite strategic in our thinking about where there might be pricing and where we’re at limits and probably need to think of other tools within the bag to solve for inflation. So I certainly would hate to be sitting here today ruling out that there’s no chance for further pricing. I just think we’ve got to be very prudent about it.

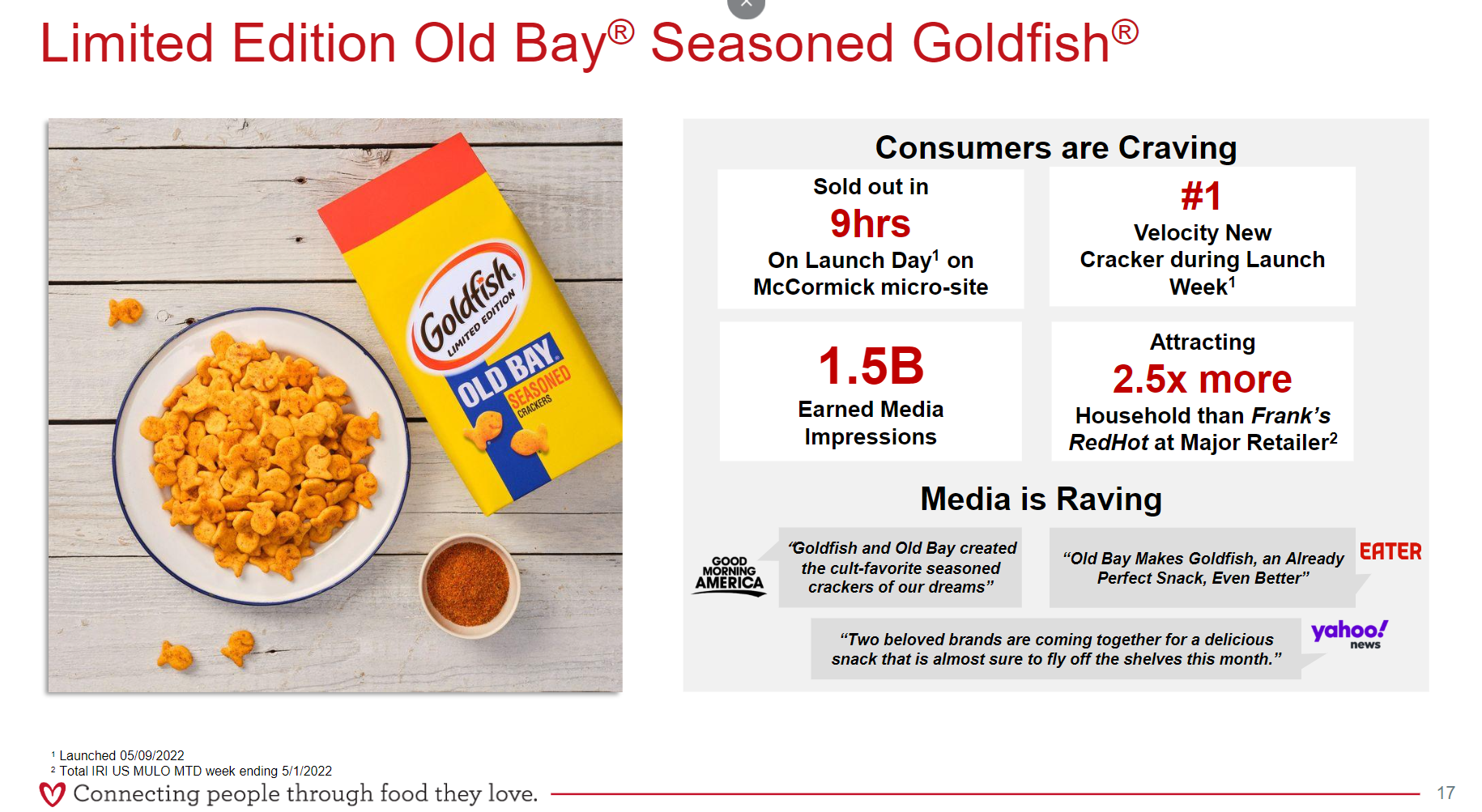

A small part of this confidence may be due to the company’s success in innovation. Last quarter, the company did some really interesting and targeted product launches. Working with McCormick, it launched a limited-time offer for Old Bay seasoned Goldfish online and saw the product sell out in 9 hours.

via Campbell Soup Company 3Q Presentation

Campbell management has done a decent job navigating the crisis. Their portfolio is still a bit processed heavy, but their strategy has been working. Combining established brands across the pricing spectrum with targeted innovation seems like a reasonable path forward.