It’s the eight installment (wow) of my annual year in reading. You can see past lists here.

23. God Bless you, Mr. Rosewater – Kurt Vonnegut Jr.

It’s pretentious and doesn’t have much of a plot. Read Cat’s Cradle or Slaughterhouse Five instead. Wikipedia

22. Cold Mountain – Charles Fraiser

Struggled to finish this novel about returning home after the Civil War. Surprised it’s considered a modern classic. Wikipedia

21. Thinking Basketball – Ben Taylor

Ben Taylor is an incredible basketball writer. His writing taught me an incredible amount about not only analytics, but strategy. I didn’t love the book, but that’s because it’s aimed at a more general audience. If you feel comfortable talking about usage rates and efficiency ratings, skip the book and head over to his wonderful website.

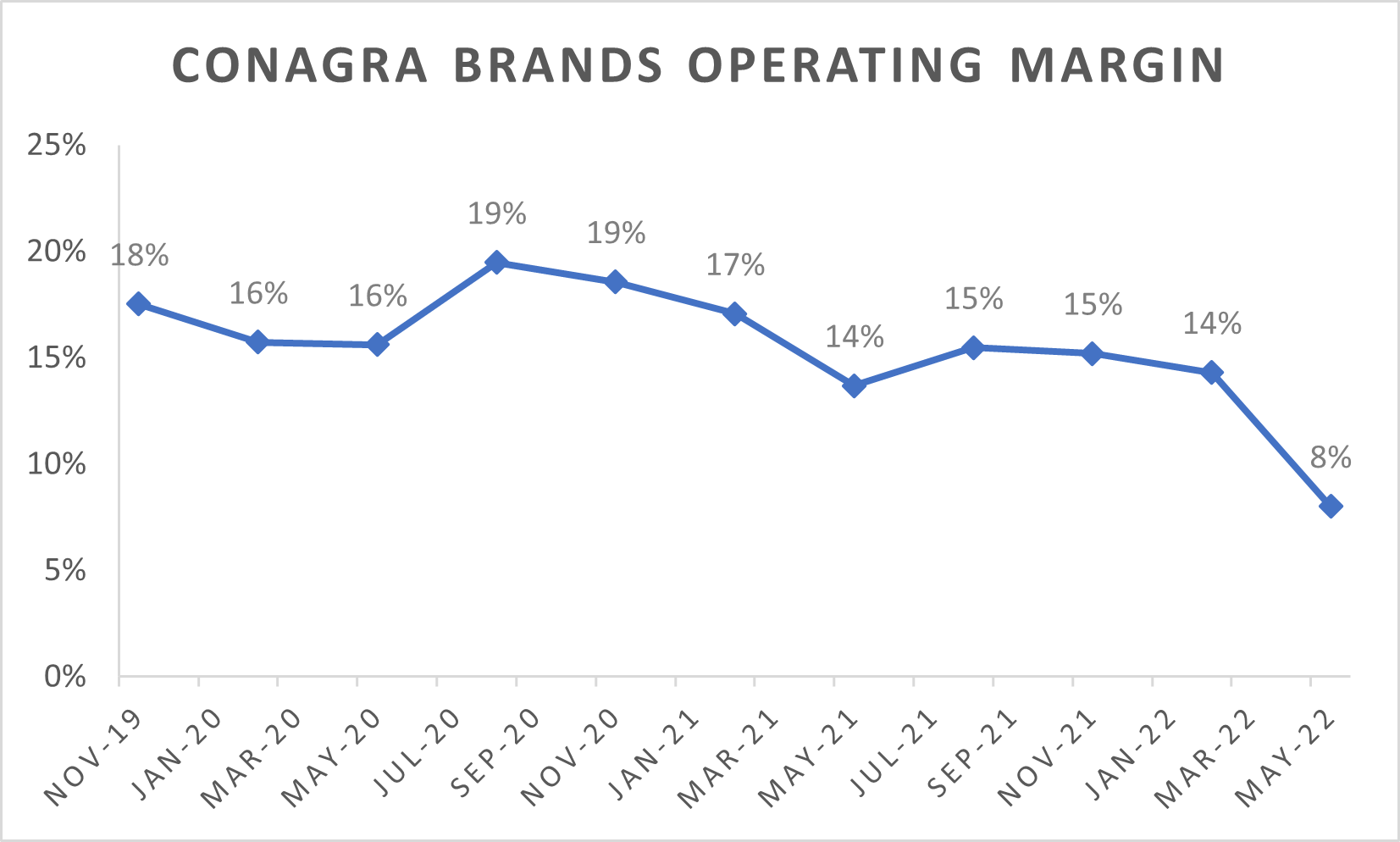

20. The Money Culture – Michael Lewis

A collection of Lewis op-eds and articles from the 1980s-1990s. Thriftbooks

19. Financial Literacy for Managers: Finance and Accounting for Better Decision-Making – Richard Labert

Good basic book on understanding corporate finance. Website

18. Operations Rules: Delivering Customer Value Through Flexible Operations – David Simchi-Levi

High level overview on building an agile organization. MIT Press

17. Bloodchild and Other Stories – Octavia Butler

Short story collection from one of America’s best science fiction writers. Wikipedia

16. How the World Really Works: A Scientist’s Guide to Our Past, Present and Future – Vackav Smil

A “realist” look at societies impending transition to a green economy. Smil frames the book around a handful of different commodities (concrete, fertilizer) and essentially argues that it’s going to be a lot harder to transition to green energy than promoters will admit. My general complaint is that it suffers from a lack of imagination. He devotes a chapter to the production of industrial fertilizer, which is an important commodity and required for America’s industrial food system. However, he never stops to ask if an industrial agricultural system is the one we should have. Website

15. The Dawn of Everything: A New History of Humanity – David Graeber

One of the bigger “big picture” books of last year. It’s fine. I just get tired of reconsidering the past. Website

14. The Nineties – Chuck Klosterman

One of America’s foremost cultural critics examines the last era of monoculture. Website

13. The Kelloggs: The Battling Brothers of Battle Creek – Howard Market

The story of how a celebrity doctor and his brother revolutionized America’s breakfast. It’s surreal how primitive society’s understanding of nutrition was 100 years ago. Impossible to consider how our modern system will look 100 years from now. Bookshop

12. Financial Statement Analysis: A Practitioner’s Guide – Martin Fridson

A fairly detailed look at understanding specific nuances around financial statements. As is all business analysis, industry context and expertise matters. Website

11. The Goal – Eliyahu Goldratt

There’s a reason this book is on every single operation’s person’s reading list. A wonderful fictional tale about how to optimize a manufacturing plant. Wikipedia

10. The Lords of Strategy: The Secret Intellectual History of the New Corporate World – Walter Kiechel

A thorough and detailed look at the rise of management consulting and its impact on the corporate world. Who would of thought that the industry took off because they were the only ones who knew how to calculate detailed profitability for far-reaching conglomerates? Harvard Business Review

9. Blood, Sweat & Chrome: The Wild and True Story of Mad Max: Fury Road – Kyle Buchanan

Oral history of the best modern action movie. Website

8. The Thousand Autumns of Jacob de Zoet – David Mitchell

I picked this up because Cloud Atlas, the science fiction novel that redefined a genre, is one of my favorite books. Turns out Thousand Autumns of Jacob de Zoet is historical fiction. The first third is slow, the second third is fine. The last third of the book is great. Wikipedia

7. Merchants of Grain – Dan Morgan

Food is inherently political. In America, affordable food is taken for granted, but a lack of it can destabilize governments and topple regimes. Dan Morgan investigates how five private companies control what the world eats, and what people pay. The book is dated (first published in 1979) but timeless in its analysis. Amazon

6. Gangsters of Capitalism: Smedley Butler, the Marines, and the Making and Breaking of America’s Empire – Jonathan Katz

Explores the origins of modern American imperialism through the lens of one of America’s most decorated Marines—Smedley Butler. Website

5. The Money Machine: How KKR Manufactured Power and Profits – Sarah Bartlett

The mechanics behind private equity are simple, but the industry spent decades and billions of dollars convincing people that it’s somewhat mystical. Financers aren’t simply stripping American industry for profit—they’re financial engineering! Written in the early 1990s, before the ensuing PR blitz to rebrand the industry, Bartlett examines the rise of one of America’s most notorious and profitable leveraged buyout firms—KKR. Abe Books

4. Narrative and Numbers: The Value of Stories in Business – Aswath Damodaran

If you’re starting out in finance, I highly recommend checking out the work of Professor Damodarn. Here he’s produced a book on the importance of crafting stories out of finance. Columbia University Press

3. The Night the Lights Went Out: A Memoir of Life After Brain Damage – Drew Magary

A suspenseful and empathetic book about surviving a brain hemorrhage. Website

2. A Memory Called Empire – Arkady Martine

A mystery science fiction novel that is both gripping and thought-provoking. Martine delves into the nature of consciousness while simultaneously examining colonialism. It deservedly won the 2020 Hugo Award for Best Novel. Wikipedia

1. The Lords of Easy Money: How the Federal Reserve Broke the American Economy – Christopher Leonard

For my money, Christopher Leonard is one of the best business writers working in America. Here, he takes a look at qualitative easing and its spiraling effects on the economy. Very modern business writers understand monetary policy. Leonard is one of them, and he explains it brilliantly. Website

Photo by Alexander Grey on Unsplash