Management at Post Holdings announced earnings last week, and things aren’t looking good for the St. Louis based consumer goods holding company. Net sales increased by 12.7%, but gross profit declined by 6.9% compared to the previous year. They’re bringing in more money, but making less profit. The primary cause? Transportation and commodity inflation. “The business has underperformed.” CEO Robert Vitale told investors.

To Vitale and the rest of Post’s management, the solution to their underperformance isn’t re-evaluating the portfolio, a portfolio that doesn’t quite seem to fit, but price increases. “We’ve been on the wrong side of the pricing versus cost inflation,” Vitale said, “and we are attempting in fiscal ’22 to have a fairly significant catch-up on that.” Post Holding’s attempted price increases will be a good test case for 2022. Can a company with limited brand power, who operates in declining categories, continue to pass costs on to consumers?

Post Consumer Brands competes in a stagnant category with limited power

In a certain way, consumer goods manufacturers are beholden to the whims of consumers. Great marketing only works so well when the category itself is in decline. It’s up to the companies to be ahead of the curve, bringing new products to market.

Grocers and retailers are generally agnostic around what food categories they sell. They want the staples (milk, bread, and meat), but at the end of the day, a department manager isn’t that preferential to the brand on the shelves—just as long as it sells. If a category is down multiple years in a row, the category loses shelf space. It’s simple.

Right now, cereal is a troubled category. The heydays of the mid-eighties are gone. From 1970 to the mid-1980s, cereal sales swelled from $660 million to $4.4 billion. During that era, cereal executives realized that sales would boom if they pumped grain full of sugar and bombarded the airwaves with advertisements. This strategy wasn’t without its drawbacks. It faced a mountain of bad press and eventually led to an FTC investigation.

The category spent the next few decades flipping between a focus on sales, and health. The 1990s are best encapsulated by Rice Krispie Treat Cereal–a cereal whose per-serving sugar content rivaled Coca-Cola. The 2000s are personified by Kashi an organic cereal brand purchased by Kelloggs in 2000. In 2018, after a two decades of trying to sell healthier options, cereal manufacturers went back to the sugar playbook searching for sales.

The Wall Street Journal explained:

After working for years to remove the synthetic dyes in Lucky Charms’ marshmallows, General Mills has abandoned that goal and instead recently came out with a new unicorn-shaped marshmallow to boost sales. The unicorn has gotten a lot more attention from consumers than Ancient Grain Cheerios ever did, Ms. McNabb said. “Unicorns are popular. But unicorns and Lucky Charms are magical.”

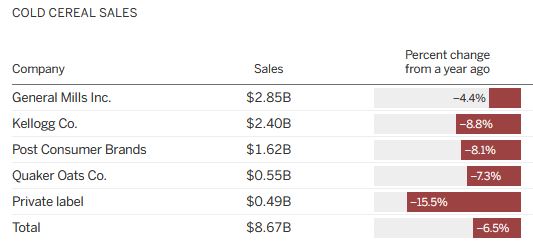

This time the pivot to sugar didn’t work as well. Call it changing consumer sentiment if you want. In the end, category sales continued to decline from around $9 billion in 2018 to $8.6 billion today.

Like most observers, Post CEO Vitale doesn’t see a comeback, telling analysts that his intuition is that cereal, Post’s primary business, is a “zero to 1, maybe 1.5% growth category” in the future. Making matters worse, cereal reflects around 37% of Post’s revenue each year but accounts for only 1.5% of overall grocery spending.

Post is a second-tier player in a stagnant category

Despite the dozens of brands on grocery shelves, the American cereal market is dominated by General Mills, Kellogg, and Post Consumer Brands. It’s been that way for most of our lives. Nearly fifty years ago the FTC brought an antitrust lawsuit against the cereal industry, alleging that the dominant players coordinated pricing actions. The defendants are still the four largest cereal manufacturers in America.

With about 19% of the market, Post is a distant third to its major rivals. Post is also up against some heavy price mix trends. Morningstar estimates that only 15% of its volume is premium priced, meaning the vast majority of the cereal it sells is around $.15 an ounce, while its competitors are selling for upwards of $.20.

Just to recap the last two sections:

- Cereal is a stable / declining category within the grocery industry

- Cereal sales make up just 1.5% of grocery volumes, which means manufacturers have limited leverage against retailers

- Cereal is Post’s number one product

- Post is a distant third in the category and has limited brand power (evidenced by lower prices)

And yet Post Holdings is looking to raise prices?

The price increase at Post is a major consumer test

For most of the 2000s and 2010s, the BLS’s At Home Food Index increased by 1.5%. Since grocery competition is fierce, manufacturers were mostly shy about increasing prices. Retailers are always looking for the lowest price, and if a manufacturer increased prices, it meant an opportunity for a competitor to swoop in. COVID-19 changed everything. The At Home Food Index ballooned to 6.5% compared to the previous year. Now, since everything is haywire, retailers and manufacturers seem to have implicitly agreed they have justification for mass price increases. You could certainly argue that the price increases bordered on the edge of profiteering.

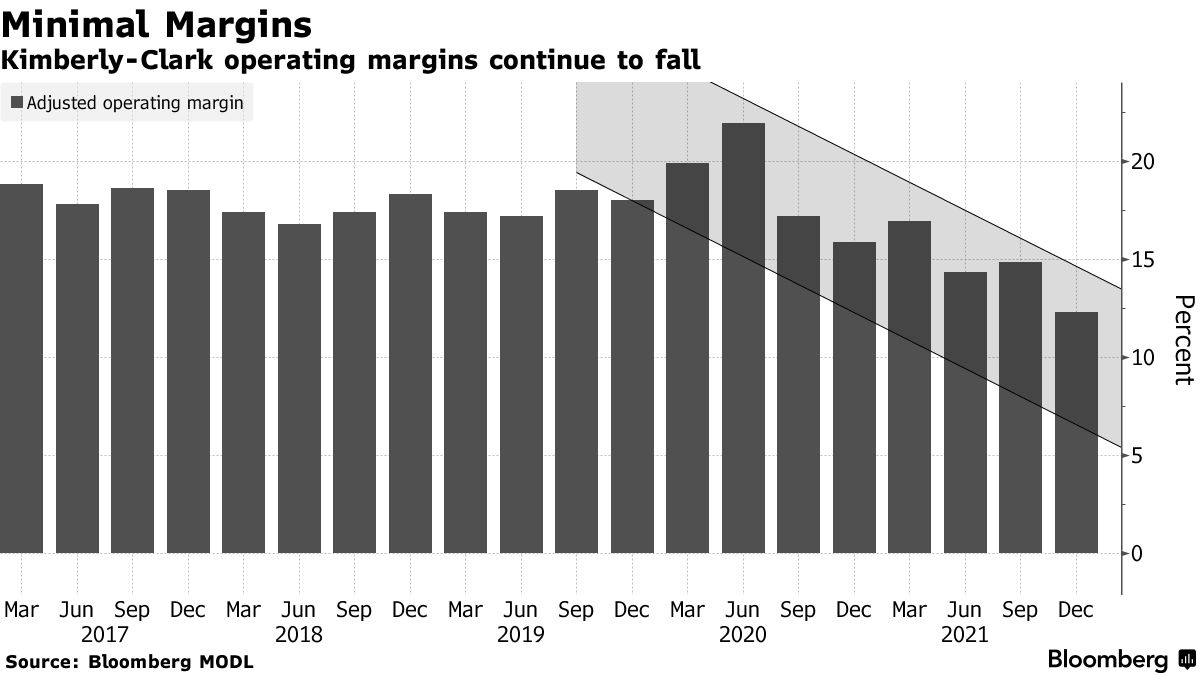

Some companies, like P&G, sell premium products and justify the price increases through an innovation lens. Basically, we’re going to charge more, but we’re giving you more value. Others, like Kimberly-Clark, are betting on the existing power of their premium brands. We’re going to charge more, but you’ll pay because you love us, and we dominate the shelves anyway.

Post Holdings is doing neither. Its brands are neither premium nor dominant. Yet here they are, raising prices.

As I said, it’s going to be a big test.