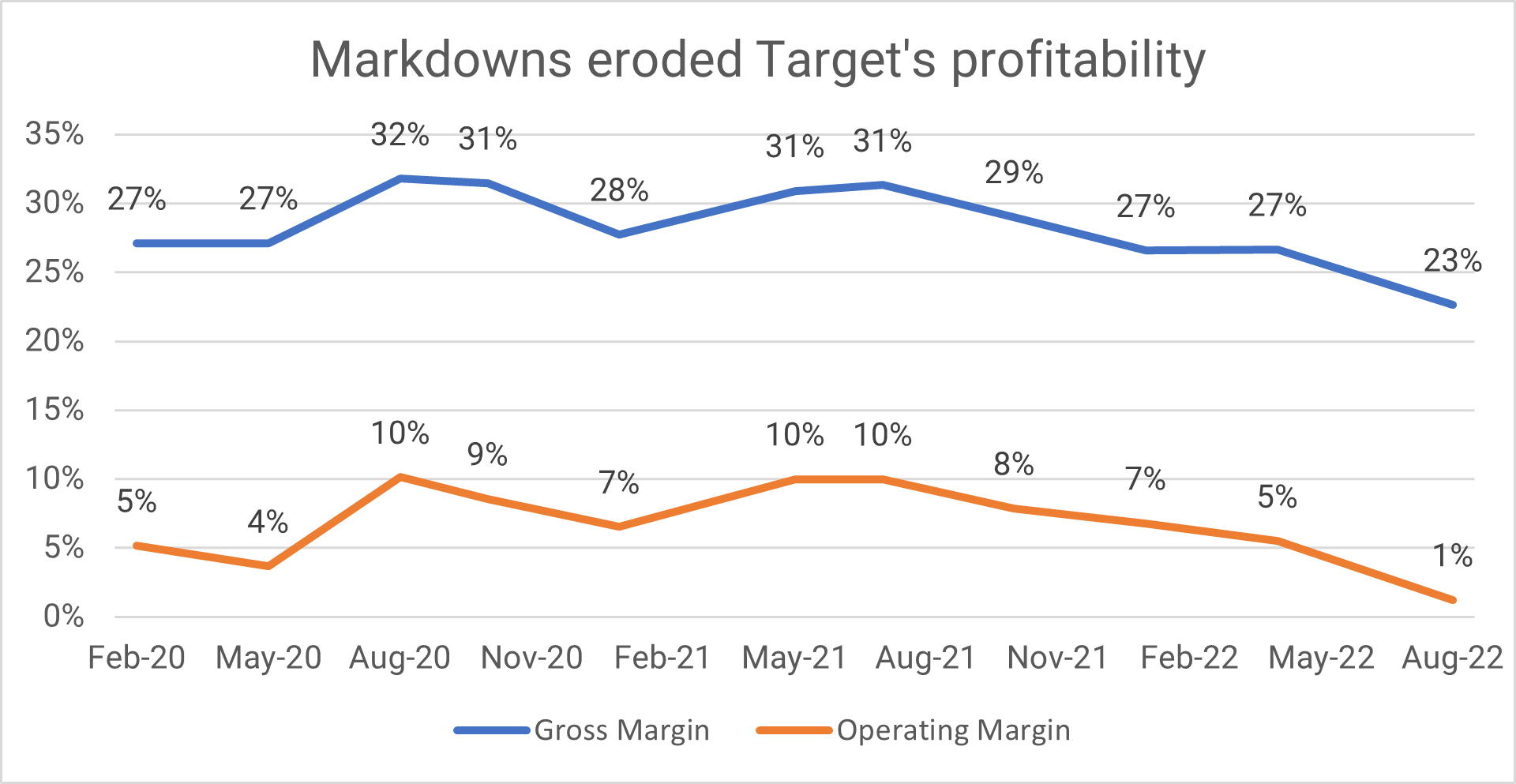

Target saw operating margins crumble after a forecasting miss pushed the company to rapidly mark down billions of dollars of apparel in a few short months. The Minnesota-based retailer typically earns around 30% gross margin across its portfolio but saw that number decline to about 23% this quarter. The numbers fall even further when accounting for operating expenses—down to about 1%. “Our focus throughout the second quarter was to ensure that we took care of the excess inventory of our network and adjust future receipts to reflect the rapid change in sales trends we’ve seen so far this year,” CFO Michael Fiddelke told investors. “We accomplished this goal to the benefit of our operations, our team and our guests.”

Inventory levels should stabilize at Target

According to management, inventory markdowns accounted for almost all margin compression, and it expects profitability to return to normal levels. “Based on the success of our Q2 inventory actions and our current performance,” CFO Michael J. Fiddelke said, “we remain positioned to deliver an operating margin rate in a range around 6% in the fall season.”

Despite the poor profitability, Target had strong sales growth. Overall, comparable sales increased almost 3%–on top of nearly 9% a year ago. Essentially, sales are up 11% from the pre-pandemic era. It isn’t just inflation. According to management, Target is growing in unit share and traffic. Even for discretionary items, where the company had significant markdowns, sales were still strong. There just wasn’t much margin. “Sales were softer than a year ago,” Chief Growth Officer Christina Hennington said, “but remained nearly $3.5 billion or more than 35% higher than the second quarter of 2019.”

As you can imagine, the composition of sales will change moving forward. Target is prioritizing food and beverage while supplementing it with high-margin categories like Beauty, toys, and its brands. The company now boasts 12 $1 billion brands. Given that Target took a big inventory loss over the last two quarters, management feels they have an efficient machine that should start returning significant returns. “Time and time again”, Hennington said. Share and traffic “have proven to be a better barometer for lasting success than growth solely through average retail prices. That’s why I’m so encouraged that across all 5 of our core merchandising categories, we grew unit share in the second quarter.”

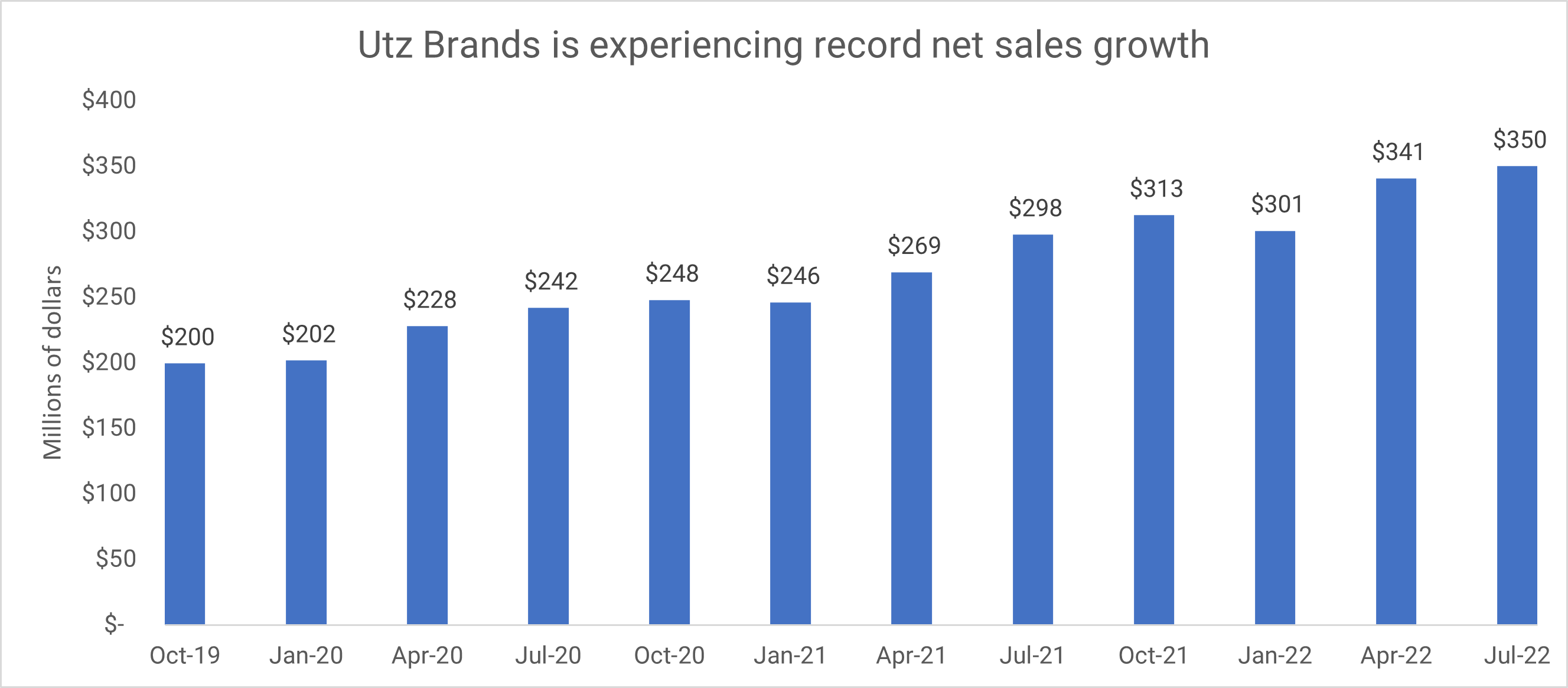

Utz Brands, the Pennsylvania-based company behind Utz and ON THE BORDER chips, delivered record net sales this quarter. During Q2 2022, Utz produced net sales of $350m, an with organic sales increasing 13.6% from the prior year. Most impressive, the company grew its category share. For the 13 weeks ending on July 3, retail sales grew 16% versus an overall category increase of 14.8%. Based on the success and limited price elasticities, Utz raised sales guidance for the year. “We now expect total net sales to grow 13% to 15% and for organic net sales to grow 10% to 12%,” CEO Dylan Lissette told investors on the earnings call.

One of the biggest standouts is the ON THE BORDER brand, which grew 15.4% in the quarter. The company bought the tortilla chip brand in 2020. Today, management estimates that it’s a $350m a year brand and projects it to grow to $450m. Not bad for an investment of $480m.

The Fast Follower Strategy

The fast follower strategy is a common strategy within the CPG world. Here, second-tier brands mimic the strategies and pricing of dominant brands. They get away with it because they’re typically lower priced. Companies maintain reasonable margins because they spend less on R&D. Utz Brands will never have the first exciting entrant in a category, but they’ll always follow shortly after.

Back in June Ajay Kataria, EVP & CFO, of the company, spoke about the strategy with price increases.

So really the entire category has been taking prices multiple rounds in the last 12 months. And the good thing about our salty snack category, it has a very rational category leader, which has an outsized share of the category. And they have been moving price up to cover inflation, and we have been fast following the category leader. And we have been sort of activating pricing as necessary to close the gaps where we see them, and that’s been the plan.

And we have taken three sort of broad-based rounds of pricing Q4 last year, February this year, and then again May this year. And then in between, we have been taking sort of closing the gaps, optimizing mix, doing things here and there across customers, across subcategories and product portfolio that we have.

And we are seeing us do that, and we’ve seen competition do the same. There have been at least three rounds of broad-based pricing in the last 12 months. And then people have been moving up packages and optimizing mix as necessary.

He continued the discussion when talking about the company’s trade promotion plans. Like most consumer goods companies, Utz cut back on promotional activity through the pandemic. Now that things are normalizing, will they increase spend to drive share?

We have found is we have been in lockstep in terms of how we are promoting, where we are promoting with the competition, with the category leaders in every subcategory.

And in most cases, it’s not the frequency of promotions that have come off the table. It’s the depth. So if we were running two for fives before, we were running two for sixes late last year. And we are up to two for sevens now, et cetera — is an example.

So I would say, we are in lockstep with the category leaders. But we are being mindful of what works on the shelf. If you go cold on promotions, that does not work with the consumer. You just have to work with the depth and the form of the promotion as well.

So not really. Utz management will watch and mimick how Frito-Lay approaches promotions.

Just don’t call them a budget alternative. When asked if being a lower-priced alternative for consumers resonated with retailers, here’s what CEO Dylan Lissette had to say.

We’ve never positioned ourselves as a lower price alternative to any of the more national brands.

Sure. Just don’t tell anyone on your strategy or pricing team.

J.M. Smucker Co. (SJM) wrapped up the 2022 fiscal year with good results, but analysts are skeptical that its COVID-19 era success is anything other than being at the right place at the right time. For the fourth quarter, the maker of Jif, Folgers and Uncrustables saw net sales increase 6 percent compared to the same time last year. Management credited a 15% price increase for the sales growth. Surprisingly, they think there’s still room for more price increases. “We don’t believe there’s a (pricing) window,” CEO Mark Smucker told investors. “We’re obviously cognizant of (pricing) pressure on consumers, but as you know, we have a responsibility to our shareholders to protect our dollar profit.” Does J.M. Smucker Co. have the power to command additional price increases despite consumers showing more appetite for private label?

Analysts are skeptical. According to Morningstar, at 6.9% of sales, Smucker’s brand investments far exceed its peer average of 5.4%. Management is paying more for marketing, but its brands are still only treading water. Part of that is because of the categories that Smucker sells. It primarily competes in peanut butter, fruit spreads, at-home coffee and pet food. Of those four, only pet food could be considered a growth market.

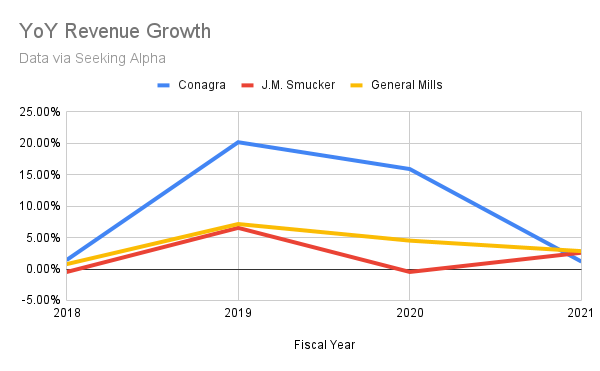

Unlike other food manufacturers, the company has not seen explosive growth during the COVID era. Production issues and a costly peanut butter recall limited the company’s overall sales growth to 2% since FY 2019. Comparatively, General Mills competes with Smucker in pet food and snacks and has seen overall sales growth of 7 percent in that time. Conagra Brands, which sells mostly food basics, experienced an explosive 17%.

Despite the lack of brand power and performance, Smucker raised next year’s sales guidance. For its part, Wall Street was skeptical. “I just think,” said a JP Morgan Analyst, “people are looking at this guidance and thinking, all right, it’s maybe aspirational to some extent.”

This week management at Target and Walmart reported the worst earnings in recent memory, sending both stocks spiraling down. Shares of Target fell by 25%, while Walmart dropped by 11%.

Despite the shock, the news may be a decent sign for the American economy, as the primary culprit is an abrupt shift in consumer demand. The COVID-19 pandemic shifted consumer spending from services to goods as consumers dealt with lockdowns and quarantines. Many have argued that the resulting demand caused an onslaught of inflation by overloading an already fragile system. In the process, it enriched established retailers.

However, this era of outsized retailer profit may be ending. After 2+ years of concentrated buying, consumers finally shifted from goods and back into services.

While we anticipated a post-stimulus slowdown in these categories and we expect the consumer to continue refocusing their spending away from goods and into services, we didn’t anticipate the magnitude of that shift. As I mentioned earlier, this led us to carry too much inventory, particularly in bulky categories, including kitchen appliances, TVs and outdoor furniture.

While it is understandable, a forecasting miss is driving the inventory issue and the resulting markdowns. Forecasting is hard in typical years; translating demand forecasting signals into inventory is almost impossible during COVID. Everyone knew the bubble would pop, but it was essentially impossible to predict when. The result is that most retailers are carrying excess inventory. Target estimates that markdowns accounted for about 3% of its operating margin decline.

The table below shows Walmart and Target’s inventory days. The metric looks at the time it takes for each retailer to sell inventory. Notice that Target dropped significantly during the worst part of the pandemic, only to shoot up this year. Walmart’s legendary operations saw some boost, but stayed pretty constant, until it regressed this year. In both cases, items were flowing in and out of stores at some of the highest levels in history.

Year

Target

Walmart

2016

279

45

2017

260

43

2018

272

43

2019

270

42

2020

216

41

2021

230

39

2022

298

48

Target and Walmart Inventory Days via SEC Filings

The next table shows inventory turnover. It’s a measure of how long each retailer cycles through inventory. Both firms did a great job at increasing turnover during the pandemic, only to see it drop 27% and 15% from the pandemic’s peak.

Year

Target

Walmart

2016

1.32

8.11

2017

1.40

8.39

2018

1.34

8.53

2019

1.35

8.70

2020

1.69

8.88

2021

1.59

9.35

2022

1.22

7.59

Target and Walmart Inventory Turnover via SEC Filings

Walmart faces similar headwinds, but its massive warehousing footprint may let it layer in rollbacks at a more measured pace. Walmart has 210 different warehouses spread across America, each with over 1 million feet of space. Last quarter, it started rolling back prices on high-margin goods like apparel and held back on larger ticket items. Target isn’t going down that route.

It has 51 facilities across the company.

John Mulligan, Target’s COO, explained:

This quarter, we ended up carrying too much inventory in several categories where the slowdown in sales was more pronounced than expected, including home electronics, sporting goods, and apparel. In addition, capacity pressures were compounded by the fact that in several of these categories, including kitchen appliances, furniture, and outdoor living, items are bulkier than average and require higher-than-average amounts of storage capacity…

Rather than jamming store sales floors with excess product, which would have made them more difficult to shop, our team secured temporary storage capacity instead. And as Christina mentioned, rather than carrying items beyond their relevant season, her team made the tougher call and marked items down to clear them and keep our presentations fresh and inspiring.

Management at Post Holdings announced earnings last week, and things aren’t looking good for the St. Louis based consumer goods holding company. Net sales increased by 12.7%, but gross profit declined by 6.9% compared to the previous year. They’re bringing in more money, but making less profit. The primary cause? Transportation and commodity inflation. “The business has underperformed.” CEO Robert Vitale told investors.

To Vitale and the rest of Post’s management, the solution to their underperformance isn’t re-evaluating the portfolio, a portfolio that doesn’t quite seem to fit, but price increases. “We’ve been on the wrong side of the pricing versus cost inflation,” Vitale said, “and we are attempting in fiscal ’22 to have a fairly significant catch-up on that.” Post Holding’s attempted price increases will be a good test case for 2022. Can a company with limited brand power, who operates in declining categories, continue to pass costs on to consumers?

Post Consumer Brands competes in a stagnant category with limited power

In a certain way, consumer goods manufacturers are beholden to the whims of consumers. Great marketing only works so well when the category itself is in decline. It’s up to the companies to be ahead of the curve, bringing new products to market.

Grocers and retailers are generally agnostic around what food categories they sell. They want the staples (milk, bread, and meat), but at the end of the day, a department manager isn’t that preferential to the brand on the shelves—just as long as it sells. If a category is down multiple years in a row, the category loses shelf space. It’s simple.

Right now, cereal is a troubled category. The heydays of the mid-eighties are gone. From 1970 to the mid-1980s, cereal sales swelled from $660 million to $4.4 billion. During that era, cereal executives realized that sales would boom if they pumped grain full of sugar and bombarded the airwaves with advertisements. This strategy wasn’t without its drawbacks. It faced a mountain of bad press and eventually led to an FTC investigation.

The category spent the next few decades flipping between a focus on sales, and health. The 1990s are best encapsulated by Rice Krispie Treat Cereal–a cereal whose per-serving sugar content rivaled Coca-Cola. The 2000s are personified by Kashi an organic cereal brand purchased by Kelloggs in 2000. In 2018, after a two decades of trying to sell healthier options, cereal manufacturers went back to the sugar playbook searching for sales.

After working for years to remove the synthetic dyes in Lucky Charms’ marshmallows, General Mills has abandoned that goal and instead recently came out with a new unicorn-shaped marshmallow to boost sales. The unicorn has gotten a lot more attention from consumers than Ancient Grain Cheerios ever did, Ms. McNabb said. “Unicorns are popular. But unicorns and Lucky Charms are magical.”

This time the pivot to sugar didn’t work as well. Call it changing consumer sentiment if you want. In the end, category sales continued to decline from around $9 billion in 2018 to $8.6 billion today.

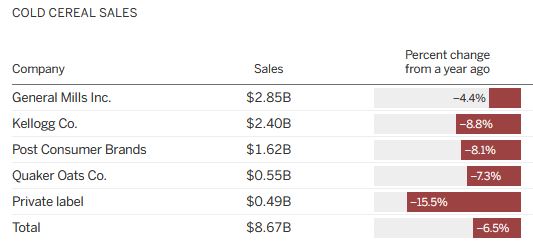

Like most observers, Post CEO Vitale doesn’t see a comeback, telling analysts that his intuition is that cereal, Post’s primary business, is a “zero to 1, maybe 1.5% growth category” in the future. Making matters worse, cereal reflects around 37% of Post’s revenue each year but accounts for only 1.5% of overall grocery spending.

Post is a second-tier player in a stagnant category

Despite the dozens of brands on grocery shelves, the American cereal market is dominated by General Mills, Kellogg, and Post Consumer Brands. It’s been that way for most of our lives. Nearly fifty years ago the FTC brought an antitrust lawsuit against the cereal industry, alleging that the dominant players coordinated pricing actions. The defendants are still the four largest cereal manufacturers in America.

With about 19% of the market, Post is a distant third to its major rivals. Post is also up against some heavy price mix trends. Morningstar estimates that only 15% of its volume is premium priced, meaning the vast majority of the cereal it sells is around $.15 an ounce, while its competitors are selling for upwards of $.20.

Just to recap the last two sections:

Cereal is a stable / declining category within the grocery industry

Cereal sales make up just 1.5% of grocery volumes, which means manufacturers have limited leverage against retailers

Cereal is Post’s number one product

Post is a distant third in the category and has limited brand power (evidenced by lower prices)

And yet Post Holdings is looking to raise prices?

The price increase at Post is a major consumer test

For most of the 2000s and 2010s, the BLS’s At Home Food Index increased by 1.5%. Since grocery competition is fierce, manufacturers were mostly shy about increasing prices. Retailers are always looking for the lowest price, and if a manufacturer increased prices, it meant an opportunity for a competitor to swoop in. COVID-19 changed everything. The At Home Food Index ballooned to 6.5% compared to the previous year. Now, since everything is haywire, retailers and manufacturers seem to have implicitly agreed they have justification for mass price increases. You could certainly argue that the price increases bordered on the edge of profiteering.

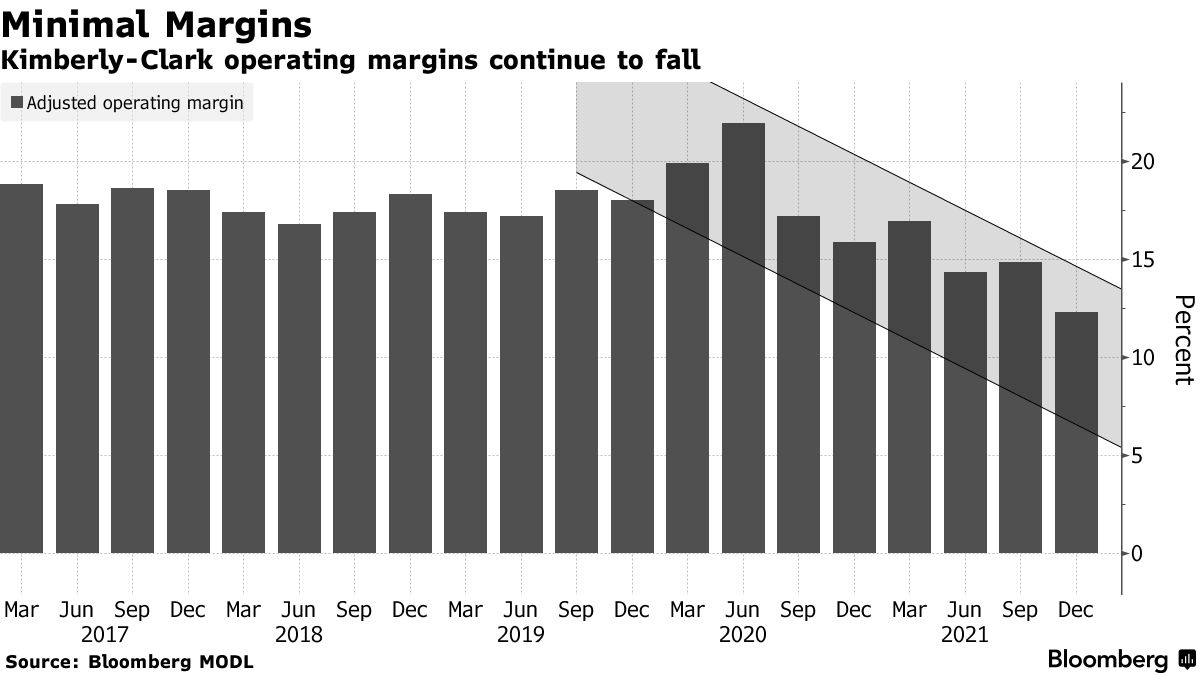

Kimberly-Clark, the personal care giant, is facing unprecedented inflation across most aspects of its business and is struggling to maintain operating margins. “We are committed to recovering and eventually expanding our margins,” CEO Mike Hsu told investors. The company, which owns Huggies and Kleenex brands, saw a rapid decline in its operating margin since June 2020. The recovery strategy is almost singlehandedly reliant on price increases. While it could work, it also means that diaper inflation is still on the menu for 2022.

A mixture of supply chain bottlenecks, COVID-19, and increased demand means that almost every consumer goods company is facing unprecedented inflation right now. Kimberly-Clark is no different. The company saw input costs rise by $1.5 billion year-over-year. According to management, that’s double the previous high of 2018.

Manufacturers like Kimberly-Clark often manage commodity purchases through yearly contracts. These contracts reset every year. With most of the inflation happening in the back half of 2021, the contracts reset to higher prices in January. Here’s how CFO Mario Henry estimated the impact of key components:

Fluff Pulp – UP

Recycled Fiber – UP

Nonwoven – UP

Super-absorbents – UP SIZABLY

Distribution – UP

Traditional Commodities – DOWN

Based on the rising cost of these commodities, Kimberly-Clark estimates an additional increase of $750m – $900m in 2022.

Diaper inflation is just the start

Last year I wrote about how KMB management signaled that the company would manage inflation via targeted price increases on premium products. Well, that was wishful thinking. Last March, the company raised prices on 60% of its consumer business by mid-to-high single digits. That action continued, with the company raising prices across North America every quarter in FY2021. Hsu expects more down the line. “I would say we’re expecting our teams to be able to price to offset the majority of the inflation,” he reassured investors.

Q1 – 2021

Q2 – 2021

Q3 – 2021

Q4 – 2021

2%

2%

5%

5%

Average KMB NA Price Increase across all SKUs (via company communications)

Although it may just be incidental, one thing that is interesting to me is the framing. P&G announced similar price increases this month. However, management framed the increases around innovation. P&G’s strategy is based around combining new product benefits with price increases—resulting in consumers “trading up” the category.

I haven’t seen much pretense of this in Kimberly-Clark’s management’s remarks. It’s somewhat odd because the company has a rich history of innovation—creating 5 of the major product categories it competes in today.

This approach seems somewhat risky, as management admits that the unprecedented times means forecasting isn’t as insightful as it once was—particularly around elasticities. “The trick of the elasticity modeling,” Hsu said, “is we’re beyond the range of estimations, So you’re kind of estimating what’s happened historically, and the price points are higher than they’ve been.”

Instead, the company is betting on the power of its brands and existing sales and distribution network.

Hsu concludes:

What I can tell you though is that I’m very confident that we will take take the right actions to recover the margins of the business, whatever that looks like. So we’ve shared with you what our assumptions are for 2022 in terms of all of the moving pieces. And if it turns out to be different than that, if there turns out to be upside, that’s great for all of us. If it turns out that the environment is rougher than what we’re thinking, we’ll take the right action.

So if inflation continues to run, we’ll continue to price. We’ll continually look at the cost structure of the business and take the right actions.

In 2017, Amazon made a fateful decision. It quit being a retailer who happened to sell online and became a retail media network.

Previously, Amazon’s retail model was simple. Users searched for what they were looking for, and its algorithm delivered the relevant results to purchase. The process was fairly neutral—derived from a straightforward algorithm based on customer reviews. A better product and solid merchandising meant more sales.

Amazon’s search results had evolved from a straightforward, algorithmically ordered taxonomy of products into an over-merchandised display of sponsored ads, Amazon Choice endorsements, editorial recommendations from third-party websites, and the company’s own private brands. In some product categories, only two organic search results appeared on an entire page of results. Since brands and sellers could no longer count on customers finding their products the old-fashioned way, through the site’s search engine, they were even further inclined to open up their wallets and spend money on search ads.

This transition has been incredibly lucrative, and we’ve seen Walmart, Target, Lowe’s, and Dollar General launch their own retail media networks in the last year. According to Forrester Research, the market could be worth $50 billion next year.

What does this mean for CPG companies?

What are Retail Media Networks?

First things first, we need to define what Retail Media is. At its simplest, Retail Media is spending advertising dollars on retailers’ websites. A Retail Media Network is the platform that retailers build to manage that spend. It gets a bit more nuanced as some retailers, like Walmart and Target, have omnichannel capabilities. For example, manufacturers can bid on search results on Walmart.com and purchase in-store video displays through Walmart Connect. In Target’s case, CPG companies can buy advertisements on Target.com, Target in-store, and across NBC Universal media properties.

One way to think about retail media networks are as an evolution of slotting fees.

Traditional brick-and-mortar retailers had limited shelf space. Retailers could only hold so much physical inventory. One way to ensure management optimized revenue/square foot was to charge slotting or pay-to-stay fees. Manufacturers pay slotting fees for the right to be on the shelf. Not all retailers charge slotting fees. EDLP retailers like Costco and Walmart do not–although you could argue they just build it into the price.

Proponents would say that retailers and manufacturers are commerce partners and that the fees offset risk within the system. The reality is retailers charge slotting and pay-to-stay fees because manufacturers have no choice but to pay them. A manufacturer is reliant on the retailer to reach consumers. It makes no money if it can’t reach consumers.

E-commerce is in a similar situation. Online storefronts have unlimited shelf space, but the only real estate that really matters is the first page. Research suggests that first page results command around 91% of search traffic. Enter retail media. This real estate is incredibly valuable, and most retail media networks have some version of “Sponsored Products.” Manufacturers pay-per-click for targeted advertising with a chosen set of keywords.

Slotting

Retail Media Network

Deal Management

Centralized

Centralized

Planning Level

Category

Keyword (arguably PPG)

Shelf Management

Manual – physical store shelf

Automated

Fee Type

Fixed

Variable (CPC)

What explains the rise of Retail Media Networks?

It’s easy money for retailers.

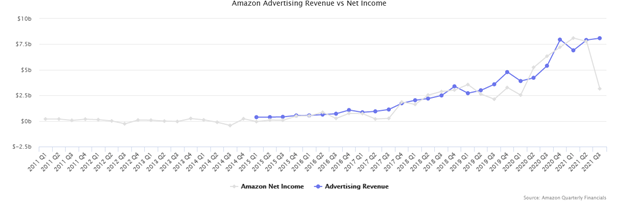

Unlike slotting, which is also easy money, individuals don’t have to stock shelves every time a company outbids another. All this income is effectively free profit. Most retail media networks are self-service portals, and the marginal cost of adjusting product search results is effectively zero. Last year, Amazon Advertising reached $7.5 billion in revenue—all profit.

Don’t believe me? Let’s take a look at its impact at Amazon. Here’s an amazing graph that charted Amazon Advertising Revenue and the company’s overall net income. There’s a clear correlation.

Are Retail Media Networks a good investment for CPG Brands?

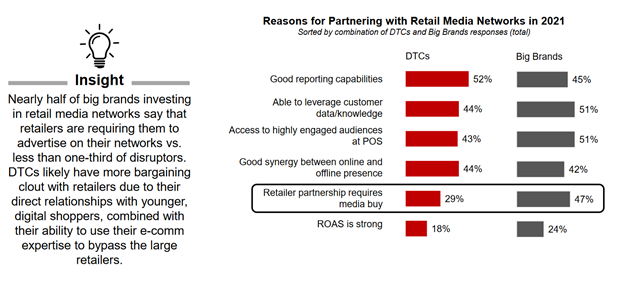

One of the more interesting aspects of the retail media network debates is this idea, often repeated by the well-intentioned analysts, is that manufacturers are okay with paying these fees because it offers unique targeting. While this may turn out to be true in the long run, it’s certainly not backed by data today.

A recent IAB survey asked CPG companies why they paid for placement in Retail Media Networks; 47% of ‘big brand’ consumer goods companies made the investments because the retailer required the media buy. Just 24% did so because of the strong return on their advertising investment.

Via: IAB Brand Disruption 2022

This sentiment is strikingly consistent across the e-commerce landscape.

Again, Brad Stone explains:

A bipartisan report by the U.S. House antitrust subcommittee would later disapprovingly conclude that Amazon “may require sellers to purchase their advertising services as a condition of making sales” on the site since consumers only tend to look at the first page of search results.

However, I don’t think that it’s all negative.

From a brand perspective, right now, the major advantage of retail media networks are twofold: First Mover Advantage and that they’re variable costs.

Right now, e-commerce is still the wild-west of consumer goods retail, and due to the reliance on algorithms, e-commerce features an inherent lock-in effect for many consumers. Once a consumer buys something through Walmart.com, the product will be forever attached to the profile—potentially locking in future sales. Since these costs are variable, rather than up-front flat fees like slotting, make it ideal for new product introductions. After all, would you rather pay $200,000 to introduce an SKU in 40 physical locations without any knowledge of its popularity or run a few targeted tests online?

What does this mean?

I think the writing on the wall is pretty clear. Retail media networks aren’t exciting avenues for growth—but rather an electronic extension of slotting fees.

The last six months or so have seen an explosion of news articles about rising retail theft rates.

The general narrative across most media organizations is that shoplifting/retail theft is getting out of control and causing retailers to close stores and adjust financial expectations. Last week executives at Best Buy, a $52B retailer, reported that retail theft was beginning to impact gross margins. Now there are plenty of reasons to be skeptical of the rising retail theft narrative. The biggest is that from 2010-2020, the FBI’s own robbery data shows that cases have declined by a third.

Retail lobbyists and their Tough On Crime allies have found an extremely effective narrative vehicle to undermine Black Lives Matter and criminal legal reform efforts, and they will almost certainly attempt to duplicate it elsewhere for years to come.

Now I don’t know if retail theft has skyrocketed post-pandemic. I find Johnson’s argument plausible. I also find it equally likely that it is rising, but we’re just experiencing a data lag in incident reporting. With that in mind, earlier this month, there was some very interesting testimony from Brendan Dugan, the Director of Organized Retail Crime and Corporate Investigations at CVS. Dugan was testifying at the Senate Judiciary Committee’s hearing on “Cleaning up Online Marketplaces.”

He begins his testimony by outlining some key statistics surrounding retail theft rates. According to CVS internal data, it loses $200 million every year due to retail theft—with an average take of $2,000 per incident. In 2020, CVS’s Retail/LTC (Long Term Care) segment reported revenue of $91.2 billion, and about $21 billion (23 percent) of that revenue was from retail sales. Using these numbers, a rough calculation reveals that retail theft accounts for about one percent of that segment’s sales.

Dugan pivots to describe how retail theft rings operate. He makes it clear that there’s a difference between shoplifting and retail theft. In retail theft, a Booster steals goods from a brick-and-mortar store, and the stolen merchandise is sold to a Fence who off-loads it to online resellers who sell the products on Amazon to consumers. “When stolen goods make their way online,” he told the Senate Committee, “the unsuspecting customer has no idea the product they just purchased was stolen.”

He continues:

Last year, my team identified and resolved over $40 million in e-commerce fraud across all online marketplaces. Our biggest case last year involved a business named D-Luxe that sold over-the-counter drugs on Amazon. D-Luxe was listed as one of Amazon’s “Top Rated Sellers.” The company was owned by a man named Danny Drago. He was known by boosters and fences as “The Medicine Man.” CVS Health investigators were led to Mr. Drago after weeks of surveilling booster activity in the San Francisco area brought them to a warehouse in nearby Concord, California.

Dugan then describes how Amazon was uncooperative with the investigation and claimed it had no information to offer even after the local police department issued Amazon a subpoena. Generally speaking, I am pro-privacy and appreciate the spirit of Amazon’s stance. However, it’s easy to contemplate that perhaps the company is more interested in protecting its business model of a largely unregulated and unmonitored network than adherents to a strict privacy policy.

Later:

Mr. Drago and his wife were involved in a nearly $40 million operation which operated at least two Amazon accounts, selling more than $5 million a year in stolen goods on Amazon and through multiple other Amazon sellers. Amazon suspended one of their accounts in 2019 but did not close the other accounts operated by Mr. Drago or the associated sellers until weeks after the CVS Health investigation resulted in his arrest and seizure of the stolen goods.

So to recap, CVS alleges that it uncovered an Amazon seller account selling over $5 million a year in stolen goods. CVS worked with the local police department, which resulted in the perpetrator’s arrest and recovery of the goods. Amazon did not fully remove the Seller from its listings until weeks after the Seller was arrested.

I can’t help but be reminded of a section in Brad Stone’s Amazon Unboundthroughout this story.

In it, Stone describes one of Amazon’s key operating principles: leverage. Amazon is willing to invest hundreds of millions of dollars in technology systems if it means it can remove humans from the operation of the system. It started when Amazon automated its own procurement system and quickly spread across the organization. It’s currently the key driver of its third-party Seller ecosystem, which accounts for over 60% of the company’s retail sales.

Stone writes:

Building such systems required a significant up-front investment and added to Amazon’s fixed costs. But over the ensuing years, those expenses paid off as they replaced what would have been even larger, variable costs. It was the ultimate in leverage: turning Amazon’s retail business into a largely self-service technology platform that could generate cash with minimum human intervention.

If you combine Stone’s reporting and Dugan’s testimony, it’s clear Amazon has limited systems in place to ensure the chain of custody of its merchandise. This is a deliberate design decision, made to maximize Amazon’s profit. Amazon’s devotion to leverage has already had a serious impact on CPG innovation. It seems likely that its pursuit of leverage may have created the nation’s largest clearinghouse for stolen merchandise.

Suppose it turns out that organized retail theft is on the rise, and authorities are serious about stemming it. In that case, policymakers should look not at individuals on the ground but at the legitimate business networks that facilitate it.

If you’ve been paying attention to any branded consumer goods company’s COVID-era financial returns, you’ll notice a familiar refrain: Things are crazy, but overall, business is going great. Private label companies? Not so much.

Before discussing the company’s financial results, CEO Steven Oakland led with a bombshell. The $4.3 billion private label product juggernaut, which makes store brands for everyone from Walmart to Wholefoods, is looking to sell off its largest division—meal prep. “We have talked about those businesses as growth engines and cash engines,” Oakland told investors. The meal prep division, which includes products like condiments and mac-and-cheese, is a cash engine. It produces relatively low-margin staples that generate a lot of cash as products fly off the shelves. TreeHouse can use that cash to in higher-margin products within its snack and beverage portfolio. If that sales goes through, “We would simply have that cash available sooner and be able to execute that strategy a little faster.”

How TreeHouse Foods is currently structured. Via 2020 Annual Report

To understand why management is pursuing this new strategy, it’s best to take a step back and look at three things: The value proposition for a private label company, the operations that enable it, and how COVID upended it all.

A private label company’s value proposition

Private label brands have been around for about as long as large retail stores have existed. Private-label goods are nothing new, of course,” Matthew Boyle wrote in Fortune Magazine back in 2003, “having been around since the days when A&P owned vast coffee plantation in South America.” For most of the 20th century, private label was associated with cheapness and low quality. Then, in the last 30 years, something changed.

He continued:

Retailers—once the lowly peddlers of brands that were made and marketed by big, important manufacturers—are now behaving like full-fledged marketers. And here’s the earthquake part: It is their brands—not those of traditional powerhouses like Kraft or Coke—that are winning over the (consumers) in the greatest numbers.

Private label manufacturers produce products that retailers can then brand under their own umbrella. However, most retailers don’t want to own their own factories, and with few exceptions, they rely on companies like TreeHouse foods for that. This setup worked pretty well before COVID-19. In the years leading up to the pandemic, sales of private label products typically grew at twice the rate of branded products.

The operations of a private label company

Since private label companies don’t handle the sales or marketing of their products, the companies have different core competencies than branded CPG companies.

1. Research and development: Creating a product that consumers want.

2. Production: Figuring out how to manufacture the improved product at scale.

3. Supply chain: Ensuring that you have enough raw commodities to manufacture the product.

4. Transportation: Getting the product to the customer (retailer).

5. Sales: Ensuring the product gets prime placement for a customer through negotiations and pricing.

6. Marketing: Generating consumer awareness and demand through advertising

The result is:

Consumers get relatively high-quality and low-cost products.

Retailers capture higher margins and generate brand loyalty through their own offerings (think Costco and Kirkland).

Private label companies operate as manufacturing partners and supply chains for retailers.

How COVID upended the private label business model

If you’ve followed this blog, you’ll know that branded CPG companies have excelled in COVID by maximizing each business process outlined above. Due to the nature of private label products, TreeHouse Foods can’t. “One thing I think to remember about us,” Oakland told analysts, “Is that we are only a supply chain business. We don’t have marketing levers. We don’t have many of the other levers that you have in your branded lives.”

Here are the levers he is referring to.

TreeHouse Foods couldn’t increase production to meet demand through third-parties.

When the initial lock-down started in March of 2020, panicked consumers flooded retail outlets. Stock-outs of common products became a regular occurrence as manufacturers couldn’t keep pace with demand. Most branded consumer goods companies opted to subcontract the production out to third parties to deal with the onslaught. In the case of General Mills, it added 50 additional partners to its production capacity. “If demand starts to taper off, that is the capacity that we will shed first,” Kofi Bruce, the CFO of General Mills, told the Wall Street Journal. Since TreeHouse Foods was the one making the already low-margin products, it didn’t have that luxury.

Faced with overwhelming demand and production constraints, managers at branded CPG companies embarked on SKU rationalization projects. “We’ve made some choices in our supply chain to — we’ve reduced some of the tail of our portfolio,” the CEO of Pepsi told investors back in July 2020. The company met with its retailers and prioritized production of the best selling SKUs. “We both agreed that it’s probably the best thing to do, to eliminate the smaller SKUs in the portfolio to maximize the best-selling SKUs and be in stock.”

Private label companies were out of luck. Since they’re focused on producing basic products, their SKU assortment is relatively limited.

In frozen waffles, TreeHouse temporarily cut flavored ones, like chocolate chip, to focus on making the basics. The leading brand, Kellogg’s Eggo, suspended production of more obscure varieties and continued selling popular flavors like chocolate chip. TreeHouse’s frozen-waffle sales took a hit as a result, Mr. Oakland said.

Private label products have less pricing power.

Most branded consumer product companies have raised prices to offset rising covid-19 induced inflation. The smart ones have used revenue growth management techniques in a targeted way that boosts profitability.

Kimberly-Clark is looking to leverage these same insights. RGM will bring in reams of data that will allow them to understand opportunities. Currently, a 32 pack of Huggies is $8.29 at Target online. Given the current level of online competition, it seems unlikely that the company could increase this SKU price.

However, done right, RGM will allow K-C to understand the true cost of selling at each customer—by SKU. RGM uses a variety of COGS, Transportation, and Trade data to reveal profitability. Maybe they can increase the base cost of a less popular item by 25%, but make up the lost volume with a promotional coupon on the 32 pack.

TreeHouse Foods doesn’t have this flexibility because its products are unbranded. In fact, the cost of producing each item is rising, but the retail price is staying the same. TreeHouse Foods is taking this cost increase! Management claims it’s to maintain good relations with their customers, but in reality, the retailers hold power in the relationship and there isn’t another option.

Private Label products aren’t optimized for E-commerce.

In 2021, it’s anticipated that online grocery sales will reach $100 billion. Unfortunately for private label manufacturers, the private label industry isn’t optimized for e-commerce.

Private labels products mainly differentiate through price. Once consumers are in a retail store, they compare and contrast products side-by-side. E-commerce isn’t optimized for that. It’s optimized for keywords, and mobile ordering often shows one product (often promoted) at a time.

In conclusion

In 2014, I wrote an article on Li & Fung, the massive Asian supply chain magnate. In it, I argued that their business model was becoming obsolete. Its reliance on just-in-time production across multiple borders made it especially susceptible to the shocks associated with climate change.

The question is, what will Li & Fung do? Their product isn’t soda or shoes. It is a network that is dependent on the system that is becoming unstable. If they don’t change, they will go from the company that no one knows about to the company no one cares about.

You can lump the current iteration of TreeHouse Foods into that category. Its entire business model was built around acquiring a massive production infrastructure to produce unbranded products.

I think management would agree.

“We had built this supply chain designed for tremendous efficiency but very low volatility,” Steven Oakland said. “When the pandemic hit, we had complexity meet volatility.”

Foodservice is a different animal than traditional CPG retail. In traditional retail, CPG manufacturers sell goods to retailers, who then sell goods to consumers. CPG companies generate bargaining power through strong brands and horizontal acquisitions. The stronger your brand is, and the more strong brands you own, the more you can dictate pricing.

Foodservice is different. Since the products are inputs into a finished product (e.g., a meal), branding doesn’t matter. An end consumer does not care if the milk in their milkshake is from Deans or Organic Valley. It’s effectively a volume-based commodity business that is supplied by branded CPG companies. In this model, CPG manufacturers sell goods to foodservice distributors, who then sell goods to restaurants/hotels/schools, who use the goods to make products that consumers buy.

It’s all about pricing, which is why foodservice distributors are the major power player and gatekeepers in the industry.

Foodservice Distributors in the USA

Before I get into the upcoming platform wars, it’s important to take a step back and define foodservice distributors. From an overall market perspective, most analysts consider foodservice distribution in America a highly fragmented market. The latest estimates place the number of food distributors at 16,500 and value the market at $268 billion a year. Personally, I view that as slightly misleading. Based on 2019 data, the top 6 distributors capture around 50 percent of the market’s revenue.

Company, Region, Tractors, Distribution Centers

Company

# of Trailers

# of Distribution Centers

Revenue

Sysco

8,577

236

$60B

US Foods

5,336

168

$26B

Performance

2,047

25

$19B

McLane

2,178

80

$16B*

Gordon Foodservice

3,000

12

$13B

Reinhart

1,379

9

$6B

McLane does not break out foodservice revenue. Estimation based on proportion.

Distributors are typically drawn from three categories: broadline, system, and specialty.

Broadline: Offer a wide variety or “broadline” of products and services.

System: Provide goods for specific large chains.

Specialty: Concentrate on a niche segment (e.g., cheese, fresh fish).

The major players dominate the broadline and system categories, and as you can imagine, the major distributors are becoming bigger and bigger. Since the early 2010s, Sysco and US Foods have completed over 30 acquisitions—increasing their revenue by $12 and $4 billion.

How do foodservice distributors make money?

In simplest terms, foodservice distributors buy products from manufacturers, hold products in warehouses, sell products to restaurants/venues, and deliver the products once sold. The goal for a foodservice distributor is basically that of a Vegas sport’s book. Just as Westgate sets a betting line to get equal money on both sides, foodservice distributors are trying to balance inbound products and outbound orders. Buy too much product, and the distributors have to pay for unnecessary storage and transportation. Buy too little, and customers jump ship because they aren’t meeting their needs.

The key business assets are the physical distribution centers, trucking network and sales network. The distribution and trucking network are huge capital expenditures—reducing the threat of new entrants into the industry. Amazon is often praised for its 100+ distribution facilities across America. Sysco has 236 locations. US Foods has 168. Unlike Amazon warehouses, they are refrigerated. Allowing both to service effectively every single place in America that sells food. (Note. In 2020, Amazon made a huge investment in food wholesaler Spartan Nash. Food wholesalers aren’t exactly foodservice distributors, but it’s an adjacent market.)

The sales network is a little less concrete but just as important. Independent restaurants figured out that they can gain more pricing leverage against the industry if they join together in what is commonly called buying groups. Buying groups often sign short-term agreements with food distributors around negotiated prices. It’s not uncommon for a buying group to switch their distributor every year. That means that distributors routinely ask for massive price discounts from manufacturers. If manufacturers don’t agree, a food distributor can drop the entire SKU from the buying group and the larger catalog.

COVID – 10 years of foodservice evolution in 10 months

COVID crated the foodservice industry in America. McKinsey estimates that restaurant sales dropped by 40-50 percent.

A McKinsey analysis explains what happened next:

Immediately after coronavirus-related shutdowns, outbound orders suddenly stopped because of government-mandated closures of restaurants, even though inbound orders of food kept coming in from farmers, foodservice producers, and processors. That led to logistical bottlenecks and storage-space shortages as distributors worked to cancel incoming shipments of inventory from farmers.

Large companies could use their scale to absorb the shock—small and medium operators were left with unsold inventory—often perishable. Perhaps even more strategically important, larger operators used the downtime to focus on sales.

Our sales teams are actively engaged with new customers and helping existing customers maximize their business during this recovery period. We continue to win business at the national and contract sales level. We have now posted over $1.8 billion of net new wins since the start of the pandemic with another strong quarter of new contracts signed. I’ve said on prior calls, the contracts we are writing are at historic profit margins.

For nationally managed customers, which, remember, includes national chains, healthcare, and hospitality, you will remember that in 2020 we added $800 million of new customer wins, which is driving some of the increases we are seeing. In the first quarter of 2021, we added $200 million of new customer wins, and our pipeline for the balance of the year is very healthy.

To restate: it’s estimated that restaurant sales dropped by 40-50 percent and the large players are adding billions of dollars of high profit margin business.

Translation: That margin isn’t coming from restaurants. CPG manufacturers are going to be squeezed.

With a handful of distributors controlling 50% of the market, distributors are going to increasingly demand price concessions–putting branded CPG firms in an uncomfortable position.