The composition of a company’s corporate officers or board can tell you a lot about a company’s operations and culture. “If a corporation has two executives who think alike,” Ray Kroc, the man who transformed McDonald into an international juggernaut, told a bunch of college students. “One of them is unnecessary.” In the case of McDonald’s corporate officers, during Kroc’s time, the group’s diverse background was viewed as a key strategic asset.

In Kroc’s mind, McDonald’s wasn’t building a typical company. At that time, franchise businesses made most of their money off up-front franchising fees. Kroc wanted to invert that model. Instead of charging $50,000 for a franchise fee, McDonald’s would charge just $950 upfront and 1.5% of future revenue. To ensure that 1.5% generated sustainable income, Kroc had to perfect the firm’s business operations—a first for a food service company.

He didn’t want to hire a bunch of MBAs to manage his business because they were all trained in a specific management approach–one that prioritized upfront fees over a long term partnership. In McDonald’s: Behind the Arches author John F. Love summarized Kroc’s situation, “Even the best hotel and restaurant schools had no notion of the type of business Kroc was building.”

McDonald’s corporate officers: Kroc’s ideal

This ethos resulted in a preference for hiring action-orientated people over academics. College and advanced degrees weren’t needed. What McDonald’s needed was people who had common sense and were willing to work the long hours necessary to build an innovative new model.

Love highlights the McDonald’s commitment to this ideal.

When he joined McDonald’s personnel department in 1962, Jim Kuhn was greatly relieved to learn that McDonald’s did not require (and still does not) a college degree for managerial slots. ‘ ‘The thing that I loved at McDonald’s,” Kuhn says, “was that they just told me to go out and get the best damn people I could get and to look at them, not their credentials. We hired people that would not have gotten through the door at other companies, not because they were losers but because they were not traditional.”

That philosophy is intact today and is reflected in the surprising lack of college degrees inside McDonald’s executive suite. Of the twenty-six executives at the senior management level of McDonald’s Corporation, fully twelve are without college degrees, including Chairman Turner. Among the company’s eighty corporate officers—from assistant vice president on up—forty-three (or 54 percent) do not have baccalaureates. For its size, McDonald’s also has relatively few MBAs (twenty-eight), and it is likely the only company in America with more than $1 1 billion in sales that does not boast a single Harvard MBA. “Our people all have real-world degrees,” Kuhn says.

This ideal turned hiring into a core strategic asset. While its competitors focused on perfecting the now, they were building towards the future.

Modern composition..still an asset?

Does McDonald’s carry on this same preference for action and results over academic achievement? Well, the short answer seems to be no. Obviously, times have changed. America’s view towards college attainment has shifted tremendously. In 1960, when Kroc was laying the foundation of the McDonald’s empire, just 7.7% of Americans were college graduates. In 1986, when Behind the Arches was published, the number was around 20%. Today, that number is 35%. But still, I was surprised by the results.

According to their website, there are 14 corporate officers. Of these McDonald’s corporate officers, all 14 have college degrees. 8 of the 14 (57%) have advanced degrees. 5 have MBAs.

As McDonald’s heads into new and unproven areas of business, namely e-commerce, it’s easy to wonder if Kroc’s vision may be better suited.

But on the bright side, there is now at least one Harvard MBA within the company: CEO Chris Kempczinski.

For as long as there has been business, there have been theories that attempt to explain the outcomes of the market. Some, like creative destruction and the innovator’s dilemma, are far-reaching and offer a universal framework to analyze the political economy. Others, like the wheel of retailing, concentrate on individual industries—and attempt to explain specific niches.

What is the Wheel of Retailing?

The wheel of retailing is fairly straight forward. Here is how Professors Peter Scott and James Walker defined it at Business History:

New retail modes frequently emerge at the bottom end of the price and service spectrum, using low-cost, low margin, `no frills’ formats to undercut incumbent competitors. However, once well-established, such retailers typically up-grade services and facilities, raising costs and prices and leaving themselves vulnerable to a new wave of low-cost entrants.

Walmart is proof of the theory. Founded in 1962 on the mantra of “Always Low Prices,” the company spread like wildfire when fair trade laws left America. Manufacturers were no longer able to control the retail pricing of their products, and Walmart took advantage. It used its size to demand steep discounts and passed the savings to consumers. This newfound pricing power was supported by cutting edge real estate strategies, operations, and logistics—leading to it becoming the most dominant retailer of a generation.

In the late 2000s, Walmart’s strategy switched. Walmart entered grocery and created “superstores.” Low prices were still important to the company’s strategy, but so was the overall shopping experience. In 2019, the company announced plans to invest $11 billion updating over 500 storefronts, which includes redesigning automotive and cosmetics. They aren’t selling the cheapest or the best—but somewhere in between. The company’s mantra is now “Save Money. Live Better.”

As Walmart moved up the wheel of retailing, a new discounter followed in its wake—Dollar General. Like Walmart in the 1960s, Dollar General offers low prices. The low prices are profitable because of their operations. Consider assortment. A typical Walmart superstore carries about 120,000 items. That’s 10x as many items as a Dollar General. From a staffing perspective, Walmart averages one associate per 475 square feet of sales space. Dollar General averages one to about 777 square feet. Dollar General offers less selection, with less customer service, but lower prices.

Will Dollar General ever move up the wheel of retailing?

I don’t think so, but before I get into why it’s important to understand why discounters become successful, and why the transition up the wheel of retailing is often difficult.

Strategy differ across the wheel of retailing

In their 2017 history of five-and-dime stores, Peter Scott and James Walker argue that earlier discounters (like Woolworth) declined because the operations that allowed them to discount profitability didn’t translate when the stores attempt to move up the wheel of retailing.

One of those operations is their personnel strategy.

Today, both Dollar General and Walmart rely on low-wage workers to serve as sales associates. Dollar General pays around $8.50 an hour; Walmart is around $12. Here’s Woolworth’s CEO describing the same sentiment in 1892:

We must have cheap help or we cannot sell cheap goods. When a sales clerk gets so good she can get better wages elsewhere, let her go –for it does not require skilled and experienced salesladies to sell our goods.

This business strategy may work when the store is selling commodity goods like toilet paper and sponges. It falls flat when selling specialized products like clothing and automotive parts. Scott and Walker quote another discounter in 1932, who recently transitioned up the wheel of retailing, highlighting the importance of suggestive selling and bemoaning low-paid worker’s ability to execute it.

You should possess this information in order to properly train your salesgirls in the art of increasing each sale. Of equal importance is a thorough understanding of the best methods for presenting your merchandise to the customer in such a manner that interest is aroused and the salesgirls’ service appreciated…Verbal suggestions must be followed up by intelligent comment… Few salesgirls are instinctively able to do this.

Walmart has been able to manage this transition. History isn’t so kind to others.

Discount strategies struggle when selling higher-value goods

Discount retailers ran into department stores when they attempted to move into high margin products. Retailers like Macy’s, and JP Penny, carried high-end products, carefully purchased by specialized buyers, and sold by well-paid salespeople.

Function

Discounter

Department Store

Advertising

No-advertising, rely on word-of-mouth generated by low prices.

Incremental volume driven by frequent sales and newspaper promotions.

Assortment

Standardized products via centralized and direct purchasing at HQ.

Individual department managers are category specialists who have wide discretion in what they purchase and carry.

Personnel

Low wage hourly sales associates.

Associates are relatively well paid by sales commission.

Discounters never really had a chance. Discounters were designed to bulk purchase a variety of commoditized goods and sell them cheaply—the opposite of higher-end retail.

So this begs the question, why did previous discounters move up the wheel of retailing?

Market saturation moves discounters up the wheel of retailing

Scott and Walker conclude that discounters moved up the wheel of retailing because they had nowhere else to go for growth. Given that the business model relied on no advertising and standardized commodity products, the only way in a new market was to cut prices—a disaster in waiting. They couldn’t enter new territories, because all the territories were taken. According to their analysis, Woolworth, a dominant player, faced competition in just 22 percent of their 238 locations.

Our model views shifts from low to higher value merchandise as being driven by retail format saturation in the low price niche. No frills retail formats compete primarily on price. However, for very low price merchandise substantial gross margins are necessary to cover high handling cost to price ratios. Price wars between rival stores adopting the same format are thus potentially ruinous. The alternative is to move into higher value lines, but this necessarily involves adding more services –to meet the minimum expectations of consumers and provide the information and advice they require. (Emphasis mine)

Dollar General faces different social dynamics

Scott and Walker were writing about an era of unbridled economic growth. As more Americans became middle class, more and more Americans wanted to purchase higher quality goods.

The opposite is now true.

As long as the economy continues to drive inequality, modern dollar stores will continue to excel, giving no incentive to move up the wheel of retailing.

From a New Yorker article detailing how Dollar General became a target for crime:

The chains’ executives are candid about what is driving their growth: widening income inequality and the decline of many city neighborhoods and entire swaths of the country. Todd Vasos, the CEO of Dollar General, told The Wall Street Journal in 2017, “The economy is continuing to create more of our core customer.”

Given what we’ve seen in the last ten years, it seems highly unlikely that Dollar General will ever need to move up the wheel of retailing.

General Electric announced it would sell its lighting business to Savant Systems in a deal valued at $250 million. The agreement itself was long rumored but still comes as a surprise. In a way, the transaction signifies the death of an era–almost as if Coca-Cola sold of its sugary beverage line. General Electric didn’t invent the light bulb, but it did invent consumer light bulbs—the first affordable and mass-produced version. This spring boarded General Electric into the pantheon of history’s great companies. In the mid-2000s, G.E. was in everything from consumer goods to entertainment, and it boasted annual revenues on par with a middle-income country. Then, mismanagement forced the company to rethink the conglomerate strategy. “It has shifted its focus to making heavy equipment,” the WSJ wrote in its coverage, “like power turbines, aircraft engines, and hospital machines.” In 2019 G.E.’s revenue dropped to around $30 billion.

Sometimes significant shifts beg simple questions. If G.E. was one of history’s best companies and it was a conglomerate, what is a conglomerate? Is there a standard conglomerate definition? What was the rationale for becoming one? Did the conglomerate strategy lead to General Electrics’ decline?

A conglomerate is simply a holding company or corporation that operates in multiple industries, usually owning individual divisions that could stand apart as separate businesses on their own. Early conglomerates were initially focused on a suite of related activities, like G.E. and electrical system in the 1900s or branded food conglomerates of the 1920s.

Like all aspects of business, the conglomerate structure evolved as American politics evolved. Founded in 1892 by five titans, including J.P. Morgan and Thomas Edison, General Electric combined a variety of small electrical component companies under one umbrella.

As both businesses expanded, it had become increasingly difficult for either company to produce complete electrical installations relying solely on their own patents and technologies. In 1892, the two companies combined. They called the new organization the General Electric Company.

Several of Edison’s early business offerings are still part of G.E. today, including lighting, transportation, industrial products, power transmission, and medical equipment. The first G.E. Appliances electric fans were produced at the Ft. Wayne electric works as early as the 1890s, while a full line of heating and cooking devices were developed in 1907. G.E. Aircraft Engines, the division’s name only since 1987, actually began its story in 1917 when the U.S. government began its search for a company to develop the first airplane engine “booster” for the fledgling U.S. aviation industry. Thomas Edison’s experiments with plastic filaments for light bulbs in 1893 led to the first G.E. Plastics department, created in 1930.

Basically, through a variety of mergers and acquisitions, General Electric was able to monopolize all aspects of the early American electrical system—from the technical standards and power generation by industry—to the light bulbs screwed into sockets by consumers.

Throughout the Great Depression, America’s attitudes toward corporate concentration changed. The consensus view was that monopoly power, like General Electric held, was bad for society. The result was a variety of New Deal regulations designed to stop conglomerates from rolling up entire industries.

Stoller explains what happened next:

But in the early 1960s a new type of conglomerate emerged, although this time these corporations were shaped by strict antitrust laws. In this instance, cash-rich corporations like RCA and LTV invested in entirely unrelated lines of business—Hertz or Wilson Sporting Goods,say—the argument being that an excellent executive team could manage any line of business well. One of the highest-flying conglomerates at the time, LTV, bought business lines in missiles, electronics, electrical cable, sporting goods, meat and food processing, and pharmaceuticals.

Essentially, General Electric was generating enormous amounts of cash and could no longer use that money to acquire businesses within its core industry.

General Electric, like many monopoly-based conglomerates, decided to expand outward.

The benefits of a conglomerate

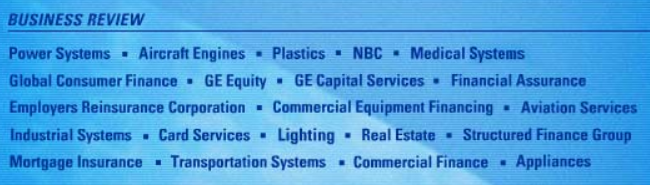

The following image lists every industry General Electric operated in 2000. That year it had revenues of about $130 billion. Adjusted for inflation, that’s about $190 billion of revenue in modern times. To put things in perspective, in 2019 the IMF estimated the New Zealand had a total GDP of about $204 billion.

General Electric was incredibly diverse. It had its hands in everything from entertainment production (NBC) to Lighting and Medical systems.

Here’s the revenue break down by business unit:

Business Unit

Revenue (millions)

Percentage of total Revenue

Margin

Aircraft Engine

$10,770

8%

23%

Appliances

$5,887

5%

12%

Industrial Products and Systems

$11,848

9%

19%

NBC

$6,797

5

26%

Plastics

$7,776

6%

25%

Power Systems

$14,861

11%

19%

Technical Products and Services

7,915

6%

22%

GECS (Financial Services)

$66,177

51%

28%

The smallest business unit had revenues of over $5 billion; larger than many best-of-breed companies. It was the definition of a conglomerate.

So we know what conglomerates are and why they became diversified across a variety of industries. Any definition of a conglomerate needs to explain the benefits of the structure. There are three major pieces.

Rise of Management

G.E. viewed businesses as interchangeable. In the eyes of leadership, a great manager could manage a microwave division just as successfully as they could manage a production company. If there was an opportunity, even if it was completely unrelated to their core competency, the company would jump headfirst. General Electric was proved right during expansionary economic conditions and was dead wrong the minute things went south.

Reduced Short Term Risk

Appliances and Industrial Products don’t have high margins like entertainment or finance, but they involve less risk and generate large amounts of cash flow—that the company can use to fund other deals and reduce risky ones.

Writing in The Master Switch, Tim Wu describes how this enabled G.E. to purchase Universal, a film production company.

Universal would enjoy as much of a hedge as any entertainment firm could hope for. By 2008, G.E. had annual revenues of over $183 billion, while Universal had income of $5 billion, less than 3 percent of the total. With a holding company of that size, the prospect of losing millions on a single film, while not pleasant, is no existential threat. Here was the ultimate defense against even the biggest movie bomb: a corporate structure so titanic that the fate of a $200 million film can be a relatively minor concern.

Synergy!

Being a conglomerate in a variety of disparate industries allows the company to augment itself across a variety of transactions. Synergy is a terrible word, but it’s the best one I can think of.

The relationship is symbiotic. G.E. Capital helps G.E. by financing the customers that buy G.E. power turbines, jet engines, windmills, locomotives, and other products, offering low interest rates that competitors can’t match. In the other direction, G.E. helps G.E. Capital by furnishing the reliable earnings and tangible assets that enable the whole company to maintain that triple-A credit rating, which is overwhelmingly important to G.E.’s success. Company managers call it “sacred” and the “gold standard.” Immelt says it’s “incredibly important.”

That rating lets G.E. Capital borrow funds in world markets at lower cost than any pure financial company. For example, Morgan Stanley’s cost of capital is about 10.6% (as calculated by the EVA Advisers consulting firm). Citigroup’s is about 8.4%. Even Buffett’s Berkshire Hathaway has a capital cost of about 8%. But G.E.’s cost is only 7.3%, and in businesses where hundredths of a percentage point make a big difference, that’s an enormously valuable advantage. And thanks to the earnings strength of G.E.’s industrial side, G.E. Capital can maintain its rating without holding much capital on its balance sheet.

Combined with a rising stock market, in the mid-2000s, G.E.’s conglomerate strategy looked like a great deal.

Until it wasn’t.

The Weakness of a Conglomerate

No definition of a conglomerate would be complete without the structures weaknesses. If you look at G.E.’s 2000 income statement, something should stick out. It was ostensibly an industrial conglomerate that made everything from MRI machines, power turbines, and microwaves. However, around 50 percent of its revenues came from financial services—most of them intertwined with the industrial business. Again, management looked great during boom times, but it became clear how incompetent management was in bad times.

As entangled as it was in the mortgage bubble and the shadow banking sector, G.E. Capital toppled over. At the height of the 2008 crisis, literally no one would lend to it in the overnight markets. G.E. Capital was only saved by an emergency injection of $12 billion from Warren Buffet and other investors. It turned out that the good reputation and credit rating of G.E.’s traditional businesses had essentially been used to gamble wildly in the financial markets.

General Electric said Wednesday that the federal government had agreed to insure as much as $139 billion in debt for its lending subsidiary, G.E. Capital. This is the second time in a month that G.E. has turned to a federal program aimed at helping companies during the global credit crisis.

G.E. Capital is not a bank, but granting it access to a new program from the Federal Deposit Insurance Corporation may reassure investors and help the lender compete with banks that already have government-protected debt, a G.E. spokesman, Russell Wilkerson, told Bloomberg News.

“Inclusion in this program will allow us to source our debt competitively with other participating financial institutions,” Mr. Wilkerson said.

Essentially, all three of the benefits of a conglomerate were so grossly mismanaged that laws had to be shifted to classify G.E. as a bank. If it wasn’t reclassified, it could of brought down large portions of the world’s economy.

Compounding matters, G.E. followed up the financial crisis with a series of bad acquisitions across its’ entire portfolio—including, the largest industrial purchase in the company’s history.

Turns out it’s only easy to manage a large corporation when the stock market is rising.

Conclusion

Rephrasing Matt Stoller’s definition of a conglomerate:

General Electric was simply a corporation that operated in eight different industries, including medical devices, light bulbs, and power generation. At its’ peak, each division generated over $5 billion a year. In boom years, the structure reduced short-term risk, created synergies, and allowed managers to shine. In bad years, the inefficiencies and mismanagement, often masked by its size, brought the firm down.

Consumer packaged goods (CPG) companies are everywhere. However, most consumers know the brands not the companies. Sprite, Tide, and Moleskine notebooks are all packaged goods brands purchased and used by millions every day. Coca-Cola, P&G, and Moleskine are the CPG companies that produce them. From an operational perspective, a CPG company manufactures products, sells them to retailers, who then sell them to consumers.

The table below gives a few more examples:

CPG Company

Brands

Coca-Cola

Coca-Cola, Diet Coke, Honest Tea

Conagra

Slim Jim, Duncan Hines, Hunts

FritoLay

Lay’s, Doritos, Cheetos

Nestle

Cheerios, Gerber’s, Pellegrino

Proctor and Gamble

Crest, Gillette, Tide

Uniever

Axe, Dove, Lipton

CPG Brands have been around for hundreds of years, although in modern times, CPG categories are mostly considered to be fast moving goods like food, drinks, and cleaning products. Put it this way, if you buy it regularly, it’s probably a CPG. Today, CPG brands are marketed around a variety of traits. Some like Clif Bar and Gatorade are performance-based. Others, like Dove soap, are centered around equality and self-love. Originally, CPG brands were built around one thing: safety.

Why is this? In the early 1900s, most goods were effectively brandless, sold out of general stores from bulk supplies. This led to manufacturers and retailers taking advantage of an unwitting public.

Lemon extract often contained no lemon. Bottled soft drinks used coal tar, a carcinogen, as a colorant. Some ketchups used saccharine, even then suspected as a hazardous adulterant, as a preservative. The “tin” in tin cans contained as much as 12 percent lead, which leached into the fruits and vegetables. Zinc chloride, used to prepare the tops for soldering, often ran into the cans during the soldering process, poisoning the food inside.

As a result, CPG companies began to brand themselves in terms of quality and safety. If a consumer saw Dove soap on the shelf, they knew it was a quality bar that floated, and they’d purchase it with confidence. Manufacturers were now incentivized to differentiate their products. If you’re looking to learn about the business processes and operations that enabled this differentiation, check out this article, which details the rise of Kraft-Heinz. If you’re looking to learn about private label business strategies read this article on TreeHouse Foods. The rest of this post focuses on the high level business strategy of a CPG company. The goal of each is to try and sell as many products as they can, to as many customers as they can reach.

Today, most CPG companies adopt a business model that pushes towards horizontal or vertical integration to accomplish the goal.

CPG, P&G, and Horizontal Integration

Up until about twenty years ago, the definition of a CPG company was straight forward. P&G was a CPG company that manufactured a variety of household products that customers purchased at retail stores.

Research and development: Creating a product that consumers want.

Production: Figuring out how to manufacture the improved product at scale.

Supply Chain: Ensuring that you have enough raw commodities to manufacture the product.

Transportation: Getting the product to the customer (retailer).

Sales: Ensuring the product gets prime placement for a customer through negotiations and pricing.

Marketing: Generating consumer awareness and demand through advertising.

These processes are incredibly scalable and repeatable across multiple categories of goods. Once a company builds up a production system or a sales department, it can sometimes seamlessly plug new items and offerings into the established business process.

Horizontal integration is simply when a company in one category, expands into another category. In the case of P&G, it started in bath soap, moved to laundry soap, then paper products, coffee, potato chips, and even dog food. Each category may seem different, but the core business processes are the same. The general process of producing, selling, and distributing aspirin and cough medicine to retailers is identical. The more products that a CPG company can sell into a retailer, the more leverage it generates. Fifty years ago, a lot of vertical integration was done organically, through research and development. Today, it’s primarily done through acquisitions. The logic is simple. Lax anti-trust enforcement means that retailers are becoming more and more powerful, which means that a CPG company needs more brands to bargain with.

CPG Companies and Retailer Segmentation

Just because the goal of a CPG company is “to sell as as many products as they can, to as many customers as they can reach,” it doesn’t, however, mean that a CPG company will sell its products to all retailers. The retailers it chooses to sell to should fit within the brand’s perceived segment.

Initially, a branded CPG company like P&G was hesitant to sell products through discount stores—as it believed the stores tarnished their middle-class identity. But money talks. Many opted to sell smaller pack sizes and value options when dollar stores became a consistent revenue driver for manufacturers.

On the other hand, Nike is a premium brand. It’s mostly an apparel company, but they certainty produce some CPG-like products. You will probably never see Nike products at Dollar General. Instead, it opted to target high-end retailers and athletic stores, but even that is changing.

Nike plans to continue working closely with 40 partners, ranging from brick-and-mortar standbys like Foot Locker Inc. and Nordstrom Inc. to newer partners like Amazon and online luxury boutique Farfetch, on new apps and in-store experiences. It said it wouldn’t eliminate the thousands of other retail accounts that it currently manages, but Nike Brand president Trevor Edwards said “undifferentiated, mediocre retail won’t survive.”

Nike’s decision to abandon Amazon had many drivers. The first is probably Amazon’s refusal to combat counterfeiting. The second is perhaps Nike’s desire to integrate vertically. Vertical integration is when a company internalizes every business process—from 1-6. Instead of buying another brand to create more leverage against retailers, it buys a commodity supplier or builds its own storefront to create efficiencies within production and distribution.

This strategy obviously can’t be executed by all CPG companies—especially fast-moving consumer goods (FMCG). It would be completely unrealistic for Coca-Cola or Campbell Soup Company to open stores that only sold their products. It’s also entirely impractical for a FMCG to develop a profitable direct-to-consumer business. Customer acquisition costs are too high for the products given that Facebook and Google own an effective duopoly on online advertisement. Most CPG vertical integration comes from retail stores themselves–who do so through private label.

Private Label CPG and Retailer Vertical Integration

So far we’ve focused primarily on branded CPG. That is, the name brand products that every knows and loves. But brands do not operate in a vacuum. Coke is not just competing against Pepsi, but against Walmart’s Sam’s Cola. For as long as chain retailers have existed they’ve sold some level of unbranded or private label products.

For the bulk of the 20th-century private label, brands were considered inferior to branded products. That changed, however, when many products became standardized through better production and supply chain practices. Today, private labels aren’t just low-priced offerings, but brand builders for the retail chains themselves.

The three best-selling private label categories in food and nonfood may still be predictable—milk, eggs, and bread in food; food-storage and trash bags, cups and plates, and toilet tissue in nonfood. However, today’s large and sophisticated retailers are able to develop credible private label offerings for categories where traditionally customers were more wary of straying from their favorite manufacturer brand names. Nowadays, store brands are present in over 95 percent of consumer packaged goods categories. Among the fastest-growing categories for private label sales are lipstick, facial moisturizers, and baby food.

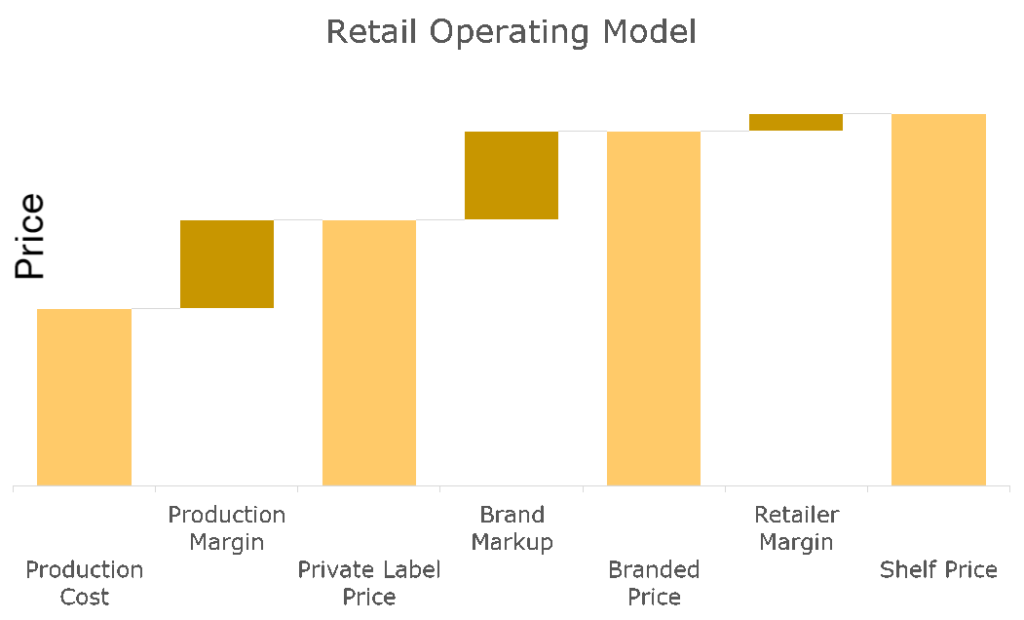

Once you see a Retailer’s operating model, you’ll understand why there is such a push from retailers.

Retailer’s Operating Model

The image below is a typical retail operating model.

The shelf price is the price consumers pay a retailer. The margin is the difference between what the retailer paid the CPG company, minus the retailer’s labor and fixed costs. As you can see, there isn’t much in the retailer’s margin. This graph doesn’t include all retailer considerations (consumer preferences, product demand via mass advertising, differences in revenue per square foot of shelf-space, etc.). Still, you can certainly see why retailers want to get to vertically integrate through private label.

If a retailer owns the production of private label good, they mostly capture all the margin between the production cost and the shelf price. The high fixed cost associated with production gave manufacturers power in a negotiation, but as retailers have become larger and larger, the cost became a non-issue.

The end result of this is that established CPG brands aren’t just facing competition from other manufacturers, but they’re facing intense competition from retailers–who used to be their partners.

In Conclusion, What is a CPG Company?

It’s tough to give a complete and exhaustive definition of a CPG company. That’s because they are so varied in what they produce and how they sell. But definitions help, and hopefully, this helps better understand what a consumer packaged goods company is and the business model it uses to makes money.

At a high level, a CPG company is a firm that manufacturers products that consumers regularly buy. It then sells those products to retailers, who sell them to the end consumer. The goal is to sell as many products, to as many consumers as possible. Today, CPG companies succeed by generating leverage over retailers by offering a variety of goods through horizontal integration. Conversely, retailers are vertically integrating, and offering their own private label goods to compete with CPG companies.

How did things go so wrong for Kraft Heinz, one of the nation’s largest, most recognizable food companies that’s backed by one of the nation’s most beloved investors? In February, Kraft Heinz announced a 2.7% decline in net sales for 2019. This comes just one year after the company wrote down $15.4 billion because legacy brands like Oscar Mayer and Kraft failed to keep up with changing consumer tastes. Its long-term debt was downgraded to junk bond status after management refused to cut its dividend. Oh, and it also was investigated by the Securities and Exchange Commission for misrepresenting financial results.

During

a scheduled conference call reviewing the past year, CEO Miguel

Patricio told investors that “2019 was a very difficult year for Kraft

Heinz.” The situation is a far cry from just four years ago when the company headlined its annual report “Kraft Heinz Reports Solid Financial Performance with Integration on Track.”

So

what happened? To understand Kraft Heinz’s fall, you need to understand

how the company came to be and how its strategy and approach to

budgeting differs from the traditional model of a consumer packaged

goods (CPG) company.

Private equity comes to town

This

all goes back to when 3G Capital, a Brazilian private equity firm,

entered the picture in 2013. The firm had earned itself a reputation for

generating profits. Like most PE firms, its model was based on cash

flow and cost cutting. The general strategy looked like this:

Identify an established brand that 3G management believed it could manage more efficiently.

Acquire it with other people’s money.

Maximize its efficiency through cost cutting.

Use the resulting profitability to finance additional deals.

The firm had used the formula to turn Burger King

and Budweiser into cash machines; it sold 1,200 Burger King locations

to outside investors and reduced the head count by almost 36,000. In

three years, net income rose 34%. “These things are seemingly working at

Burger King,” an analyst told Businessweek in 2014, “and causing questions to be asked about the strategy of others in fast food.”

With financing from Warren Buffett, arguably America’s most respected investor, 3G gained control of H.J. Heinz

for around $23 billion in 2013. Two years later, the group acquired

Kraft for $49 billion. The result was the fourth-largest food company in

America with a roster of stable brands, including Oscar Mayer, Jell-O,

Maxwell House, and Planters. “This is my kind of transaction,” Buffett said after the deal went through, “uniting two world-class organizations and delivering shareholder value.”

Since 2013, more than 10,000 people — one-fifth of the workforce — have been laid off from Kraft

and Heinz, with seven plants shut, highlighting the human cost and

upheaval involved in producing the highest profit margins in the food

industry. The founders of 3G have transformed the beer, fast food, and

food manufacturing industries with bold acquisitions, which are quickly

followed by a brutal but disciplined attack on costs, a surge in

profitability, and high returns to shareholders.

The

“brutal but disciplined attack on cost” has a name: zero-based

budgeting. The logic behind it is compelling while being simultaneously

against the branded CPG industry’s entire business model.

How zero-based budgeting works

Traditional

corporate budgets are derived from historical information. Imagine that

you’re in charge of in-store marketing at Kraft. Last year, you spent

$15 million on a variety of in-store marketing events. After analyzing

inflation, competitor data, and new item distributions, you estimate

you’ll need an additional $500,000 in funding to support the business.

Your boss agrees, so you get the budget.

Zero-based

budgeting doesn’t work that way. In zero-based budgeting, every single

company expense (from in-store food samples to pencils) is classified

into a specific category. Each category is assigned a manager who builds

a budget from scratch, justifying every single expense. Budgets are

analyzed and awarded a cap. Managers are then incentivized based on how

much they spend under the cap.

The result is a ruthless accounting of company expenses.

In

the first few years, Kraft Heinz eliminated over $1.7 billion in annual

spending. This included excessive expenses like private executive jets.

It also included eliminating things that don’t cost a lot, like taking

away free Kraft snacks in break rooms and limiting each employee to 200

printed pages a month. Workers may have hated it, but investors loved

it. According to Berstein Research, for every dollar of sales, the food industry typically earns about 16 cents. Eighteen months under the new regime, 3G was earning 26 cents for every dollar it sold.

There’s

nothing inherently wrong with documenting and assigning

responsibilities to spend. In fact, 10 to 15 years ago, you could almost

certainly make the argument that many CPG firms were bloated. But the

problem with this approach is threefold:

It

assumes the underlying brands independently operate with stable and

strong business infrastructure — and that both are capable of doing more

with less.

It

discounts the fact that legacy brands — almost all of Kraft Heinz’s

portfolio — require promotional spending to maintain past sales

performance.

It

fails to take into account that businesses aren’t linear. They are a

collection of interdependent processes, each one influencing and

impacting the bottom line in aggregate. It isn’t always possible to

account for and rationalize every single expense because the results are

often dependent on numerous factors.

In

year one, a cut in marketing and promotional spending may not impact

much. Change doesn’t happen overnight. The initial success means the

cuts are repeated for three straight years — because why not? The

manager is incentivized to cut. Everything is fine until reality catches

up. A legacy brand with reduced promotional support in an ever-changing

category is a recipe for disaster. Suddenly, sales stop and management

is forced to take one of the largest write-downs in a decade.

Creating true value

CPG

companies are valuable because of the sum of their interlocking parts. A

company can have the best product in the world with a great marketing

campaign, but what does it matter if it can’t consistently manufacture

it? The following major business processes drive consumer product

companies:

Research and development: Creating a product that consumers want.

Production: Figuring out how to manufacture the improved product at scale.

Supply chain: Ensuring that you have enough raw commodities to manufacture the product.

Transportation: Getting the product to the customer (retailer).

Sales: Ensuring the product gets prime placement for a customer through negotiations and pricing.

Marketing: Generating consumer awareness and demand through advertising.

Zero-based

budgeting is about making each process the most efficient version of

its current state. But despite how zero-based budgeting operates in

theory, business processes aren’t independent. Businesses typically get a

greater return on sales spend if they’re backed by a marketing campaign

and vice versa. Some processes, like research and development, are not

linear. It may take years for a product innovation to break through.

For

an example of a more successful way to acquire a company and integrate

it into the core processes — rather than trying to grow through cuts —

we can look at what happened with P&G and Charmin.

Building new value through acquisition

In

1957, P&G acquired a Green Bay, Wisconsin-based papermaker named

Charmin. At that time, Charmin wasn’t the national powerhouse we know

today. It was a regional afterthought with about $20 million in sales.

To put the acquisition in perspective, P&G had an advertising budget of over $80 million the same year.

Like

the more recent Kraft Heinz deal, the logic for the acquisition was

compelling. Acquisitions are evaluated based on how well they plug into a

company’s existing operations and strategy — both vertically and

horizontally. Vertically, P&G had technical experience with

pulp-making, a key component of papermaking itself, through the Buckeye

Cotton Seed Oil, a company it owned that manufactured component

materials for film. Horizontally, it had a long history — first with

soap, then with detergent — in marketing and distributing low-cost

consumer products. On paper, everything looked fantastic. P&G had

both the technical and business skills to build the brand.

What could go wrong?

For starters, Charmin wasn’t a product consumers wanted. Today it’s the most popular branded toilet paper in America,

but in the 1950s, it regularly placed last in blind tests against

products from paper powerhouses Kimberly Clark and Scott Paper. The poor

quality meant that Charmin only controlled about 14% of the Midwest and

Great Lakes market. Out-of-market retailers weren’t willing to give

shelf space to a product that couldn’t win in its own territory.

When P&G went up to Green Bay, it realized that Charmin failed in just about every process — specifically production. Rising Tide, the history of P&G, explains:

Charmin

benefited almost immediately from P&G’s more sophisticated

financial and marketing techniques, but the transfer of technical

knowledge proved troublesome. At the time, papermaking was considered an

art, in the same way soap making had been earlier in the century.

Charmin “had no clearly established product or process standards.”

Despite

having technical paper experience, P&G struggled to develop a new

product. Mass production requires a strong paper to withhold against the

stress of the pushing and pulling of papermaking machinery. But making

it strong meant a thicker, harder paper — not exactly the words people

want to be associated with toilet paper.

After

years of experiments, P&G engineers developed CPF, a paper

manufacturing process based on a Japanese technique that involves

inserting an air drying step into the manufacturing process. CPF

resulted in a softer and more absorbent paper that had a cheaper

per-unit production cost than traditional methods. Rival firms got wind

of the new process but were powerless to respond because they were

locked into extensive and costly legacy manufacturing systems.

Adapting existing processes

Investing

in research and development and production processes resulted in

P&G having a better product, but retailers didn’t want to sell it.

Competitors made sales presentations that showcased how poorly the old

version of Charmin performed. “Who needs a brand that’s been on the

market for five or six years and is a weak number two or a weak number

three in its category?” P&G’s former sales director later told

interviewers.

This

is where P&G’s existing horizontal sales and marketing processes

came into play. P&G put its marketing skills to use, inventing a new

branding campaign, “Don’t squeeze the Charmin.” It then redesigned the

packaging. Toilet paper was traditionally sold in opaque paper

packaging. Charmin marketers put it in clear plastic, creating an

attention-grabbing effect on the shelf.

Armed

with a superior product, a revamped brand, and better packaging,

Charmin launched pilot programs in select cities. Within months, Charmin

climbed to the top of each test market. The initial success gave sales

representatives a story to sell. It’s hard to imagine now, but as the

brand expanded into new cities, retailers couldn’t keep it stocked. “The

thing just took off like nothing had ever taken off before,” Ed Artzt, a

sales and marketing executive, recalls.

After

two years, Charmin was the bestselling toilet paper in every region it

competed in. R&D created a better product, which led to a great

marketing plan, which led to big sales increases in retail stores. The

process was long, difficult, and cost millions of dollars, but it was

worth it. “The acquisition of Charmin,” David Dreyer wrote in the

company’s history book, “became the basis of several billion-dollar

brands and one of the company’s leading growth producers.”

Where does research and development go at Kraft Heinz?

It’s

staggering to contrast Kraft Heinz’s integration approach to P&G

and Charmin. It’s even more staggering when you look at one specific

business process: research and development.

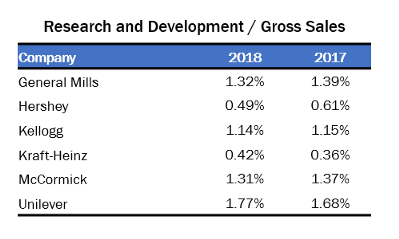

As the Charmin example showed, research and development is at the center of a branded CPG firm. Consumer preferences change, and it’s up to manufacturers to develop new products that consumers want. In the food industry, consumers are transitioning away from fatty packaged food and toward healthy and fresh alternatives. According to Businessweek, from 2014 to 2017, the top 10 packaged food companies lost over $16 billion in revenue. No one is entirely sure what this means for legacy manufacturers like Kraft Heinz, but during this transition, Kraft Heinz slashed R&D budgets. In the three years before the merger, Kraft spent about 0.8% of revenue on research and development, already somewhat low for CPG firms. The table below shows how it only got worse once Kraft Heinz merged:

Data via firm annual reports

Making

matters worse, when Kraft Heinz actually made an investment in R&D,

it chose poorly. In an attempt to compete with healthier products, the

company invested $10 million to reformulate hot dogs — at about the same time the World Health Organization labeled the food as a contributor to the risk of colon cancer.

A different approach

To be clear, 3G management took on an almost impossibly tall order with a $72 billion acquisition of Kraft and Heinz. First, history is littered with failed mergers and acquisitions. Billion-dollar transactions rarely work out unless you’re the bank booking the M&A fee. Second, both companies were established CPG firms. Unlike P&G and Charmin, there was no real value in bringing Kraft’s products into Heinz’s existing business processes because Kraft’s processes were probably just as efficient. It’s not like Heinz hadn’t mastered producing and selling ketchup for the last 100 years.

P&G

acquired a regional toilet paper brand and spent enormous sums of money

developing a better toilet paper. It supported the product with

world-class marketing and sales. Charmin dominated the industry for the

last 60 years. 3G could have mimicked this approach. It could have

acquired Kraft and then targeted smaller, regional brands that produce

healthy options that would benefit from the company’s established scale

and business processes.

Instead, it pursued a strategy centered on two tactics: optimizing operations through cost cutting and generating leverage against retailers by creating the fourth largest food company in America. The former slowly and then suddenly deteriorated the value of the company’s legacy brands. The latter hasn’t materialized. In the case of the reformulated hotdogs, Kraft Heinz struggled to sell them to Walmart, which constitutes about 20% of the company’s yearly sales. The grocery goliath preferred Ballpark Franks and its own private label, leaving the new company in the same position facing many legacy manufacturers.

The

result is a company with legacy brands hemorrhaging sales to healthy

upstarts and an organization ill-prepared for the new reality.

“[Innovation] is a big driver for growth for the future, has to be

especially in the food industry,” Patricio, Kraft Heinz’s CEO, told investors in 2019. “But we have to do bigger innovation. We have to do fewer innovation[s]. We have to do bolder innovation.”

But

because Kraft Heinz is spending so little on R&D, these innovations

have yet to yield meaningful results. That’s because without properly

funded R&D, Kraft Heinz is stuck either treading the same path while

ignoring consumer trends or failing to innovate significantly and

quickly enough. Last year, in fact, one of the biggest new product

launches from Kraft Heinz was salad frosting.

In November 2019, during an economic expansion, Dean Foods declared bankruptcy. The nation’s largest dairy company, with the number one white and chocolate milk brand, could not make money. In January 2020, Borden Dairy followed suit. Most post-mortems dealt with the fact that both companies produced dairy — a product that fewer and fewer people consume. This is true. According to the USDA, from 2000 to 2017, per capita milk consumption in America declined 24 percent. Very few companies can survive a massive decline in their keystone product. But it’s not the full story.

To understand how two of America’s largest dairy companies found themselves with hundreds of million in debt and few good options, you need to understand the competitive forces that drove the evolution of the dairy industry.

The Five Competitive Forces that Shape Strategy

The most common way to analyze industrial competition was first popularized in Michael Porter’s classic 1979 paper “The Five Competitive Forces That Shape Strategy.” According to Harvard Business School, Porter’s article has been cited over 6,000 times, making it arguably the most influential management paper of all time. The general crux of Porter’s argument is that five disparate forces drive competition within any industry. The forces continuously change based on advances in technology and policy. It is a manager’s job to position the company to compete where they are the weakest.

In his 2008 update, Porter explained how the five forces drive profitability in the airline sector.

Rivalry Among Existing Competitors: How incumbents compete. For the vast majority of consumers, airlines aggressively compete on price.

Bargaining Power of Suppliers: There are only a few plane and engine manufacturers — giving each one additional leverage over airlines.

Threat of New Entrants: It’s a high-profile industry that new flight providers continuously enter. Some succeed (JetBlue) and some fail (Virgin and Hooters)

Threat of Substitute Products or Services: Train and car travel are always options

Bargaining Power of Buyers: Limited customer loyalty (except business travelers).

I would add a sixth driver to the list: political economy. Essentially, political economy is how the government decides to organize the economy. If you analyze the dairy industry from this modified Porter’s model, it becomes evident that changing customer tastes were not the primary cause of Deans or Bordens’ problems. Rather, the companies are caught in a vice from all sides, driven by longstanding government policy. The bankruptcies are a warning for all CPG manufacturers. To see why, you need to understand how political economy shaped the retail industry.

A Brief History of Dairy Processing (1900–1950)

Before the 1950s, dairy was an intensely local industry. That’s because dairy is a unique industry from an operational point of view. Raw milk supply is effectively constant. Unlike fruits or vegetables that have defined growing and harvesting seasons, cows must be milked every day. Once the raw milk is out in the world, it must be processed immediately, or it goes bad. Once it’s processed, milk must be delivered to consumers quickly for the same reason. The entire system operated under the threat of a couple week countdown. This led to an industry framework where dairy processors congregated outside of major metropolitan areas. Rural farmers provided raw milk to processors, who expanded the shelf-life via processing and distributed it to urban consumers.

During this era, farmers (suppliers) had limited bargaining power with processors. Unlike farmers, dairy processors were well-capitalized, few in numbers, and could easily drive raw milk prices down by playing small farmers against each other. After years of predatory behavior by processors, the Federal government regulated the industry by prioritizing a co-op model. Essentially, farmers were encouraged to join together to negotiate better prices with dairy processors.

Firms that produce fluid milk and dairy products are either dairy cooperatives or proprietary companies. Many of the proprietaries are large companies in themselves or are subsidiaries of some larger company. Dairy cooperatives are businesses owned by the farmers who supply them with milk. Farmer cooperatives range from very small, either by volume or membership criteria, to very large. Proprietary companies have gravitated toward the fluid milk and ice cream businesses, cooperatives have dominated butter manufacturing, and both have been important to cheese.

Today, co-ops handle about 85% of consumer milk.

From 1900–1950, a Porter’s model of the dairy industry would look something like this.

Rivalry Among Existing Competitors: Competed mostly on price and distribution networks. Distribution through a costly direct-to-consumer “milk-man” system.

Bargaining Power of Suppliers: Primarily small farmers with no individual bargaining power. Government intervention led to co-ops and greater equality between processors and suppliers.

Threat of New Entrants: Milk processing was a capital-intensive industry with high production and distribution costs. A perishability moat protected incumbents from geographic expansion. The primary threat was dairy co-ops transitioning from selling groups to processors.

Threat of Substitute Products or Services: Limited. Milk was a consumer staple.

Bargaining Power of Buyers: Buyers were primarily individual consumers. Limited leverage due to perishability, transportation issues, and small purchase size. A single consumer could not really play processors off each other.

Political Economy: Geared towards regulated competition. The government enforced anti-trust laws to ensure that dairy processors, farmers, and retailers shared an equitable balance of power.

The model held until technological innovation drastically altered the playing field.

Technical Disruption (1950s — 1980s)

The dominance of local dairy processors unraveled in the 1950s. Driven primarily by technology, the industry progressed from a local industry to a regional industry and then finally national.

However, throughout the second half the of 20th century, several factors combined to reduce the cost of moving milk from producers to consumers and ensuring a transition to what is now a national milk and dairy product market. These factors included improved roadways (e.g., the interstate highway system) and larger and faster trucks for bulk transport of milk (tanker trucks). By the 1970s, most retail milk was purchased in stores (or through food service), primarily in lightweight plastic or paper containers.

Essentially, technology destroyed the perishability moat that protected small local dairy processors. There was now a massive incentive for processors to expand into new geographies — and building a regional brand was the best way to do so.

At the same time, local grocery stores evolved into regional chains. Now with regional scale, retailers looked to expand to new geographies and viewed low-cost private label milk as a key traffic driver.

In the 1960’s, most large supermarket chains installed central milk programs. Some built their own plants, especially to capture guaranteed margins in those States where wholesale and retail prices of milk were set by a State agency. The others contracted with one milk company for private label milk at significantly lower prices made possible both by larger volume (one processor instead of three or four) and limited service (delivery to the retailer’s platform instead of arranging individual cartons in the case).

The following competitive framework developed

Rivalry Among Existing Competitors: Milk processors competed on price and distribution network via a direct-store-delivery network. Regional and private-label milk brands were now common.

Bargaining Power of Suppliers: Advancements in road and refrigeration technologies allowed farmer co-ops to expand their shipment radius and increase their bargaining power. A farm in Iowa could now easily sell to a dairy processor in Wisconsin.

Threat of New Entrants: Advancements in road and refrigeration technologies allowed local processors to expand into new geographies. The perishability moat was removed. There was still a significant capital cost for net-new entrants (distribution, production.) Large retail chains enter the market through private label.

Threat of Substitute Products or Services: Limited. Milk was a consumer staple.

Bargaining Power of Buyers: Primary buyers are now grocery and retail customers — not individual consumers. Most grocery chains are still local — ensuring leverage for processors. But retail chains have more leverage than individual consumers — enabling volume discounts.

Political Economy: Still geared towards regulated competition.

CPG manufacturers, like dairy processors, excelled in the post-world era of regulated competition. In the 1980s, the political economy changed. Slowly, but surely, the groundwork was being laid for their demise.

Consolidation lays the groundwork for Bankruptcy at Dean Foods (1980s — on)

As I’ve explained, the dairy industry was originally structured around a balance of power between suppliers, processors, and retailers. If a proposed acquisition was deemed to give too much power to one party, it was rejected. This framework was true for every CPG company. Starting around the 1980s, the political economy of America became focused on one thing: lowering prices for consumers.

It may seem like a small thing, but in reality, it drastically changed the power dynamic for every CPG firm. In the 1960s, the US government blocked a grocery store merger because it would control seven percent of the Los Angeles Market. Today, Walmart controls fifty percent of the grocery market in 43 metro areas. This hands-off approach shifted the balance of power to retailers and large manufacturers. Consolidation was now the principal growth strategy for almost every actor. The bigger a company was, the more it can dominate negotiations.

Last year, Kroger Co. announced plans to buy Ralphs Grocery Co. from parent Fred Meyer Inc. and Albertson’s said it would buy American Stores Co., which owns Lucky. A year earlier, Safeway Inc. took over Vons Cos. before later moving into Chicago to buy Dominick’s Supermarkets Inc. Roughly 10% of the supermarkets in the United States have merged just in the last six months.

Dean Foods did not stand idle. It kicked off the 1990s with a torrent of acquisitions. From 1989–1992 it added $300 million in revenue by acquiring food processors in California, Tennessee and Washington. The strategy was simple. It purchased an established regional brand, modernized the processing plant with cutting edge technology, and folded the operations into the company’s existing infrastructure. The result was more leverage against suppliers, retailers, and the ability to expand into new geographies. The company repeated that strategy throughout the decade.

That same year, Suiza purchased Dean Foods for $1.6 billion.

In the end, the new Dean Foods / Suiza divested 11 plants, won regulatory approval and the new Dean Foods became the largest dairy processor in American history. It’s inconceivable that the two companies would even consider the merger just twenty years before.

The power of buyers increased exponentially, and dairy processors reacted. The result was a new competitive framework.

Rivalry Among Existing Competitors: Milk is still a commodity, but with some innovation — Dean introduced new bottle types. Overall, pricing drives competition. Private label drives prices down. Dairy processors look to get bigger in order to assert leverage.

Bargaining Power of Suppliers: Decreased substantially. Consolidation means fewer processors and less leverage. Family farms enter a crisis.

Threat of New Entrants: Large. Suiza did not exist in 1980. By 2000 it owned Dean Foods.

Threat of Substitute Products or Services: Limited. Milk was a consumer staple.

Bargaining Power of Buyers: Immense. Consolidation enabled retailers to demand, and receive, massive price discounts.

Political Economy: Regulated competition is no longer a priority. Lowering consumer prices drive policy.

You’d be hard pressed to say that consolidation outright caused the Dean Foods’ or Borden bankruptcy. The Dean / Suiza merger was profitable for a decade. However, it pushed the company to acquire a large and expensive fixed cost production footprint across the nation.

It seemed like a safe bet. Milk was a consumer staple for 80 years.

Then that changed.

Changing consumer tastes

We’re about 2,500 words into this post. Now is a good time to bring up changing consumer tastes. In the last decade, people quit drinking milk.

U.S. milk consumption has been falling for decades. In 1984, milk consumption represented a 15% share of all eating occasions, according to the NPD Group. By 2019, milk represents only a 9% share.

In the last four years, sales of non-dairy milks have risen 23%, according to Nielsen data. Alternatives like soy and almond milk have become popular as health-conscious consumers have grown wary of dairy.

Putting this all into context, to defend itself against predatory retailers, dairy processors took on an incredible amount of debt to acquire a massive milk production infrastructure. Then people quit drinking milk.

The bottom drops out

Retailers view milk as a traffic driver. They want it as cheap as possible in order to drive store traffic. This isn’t a new development. Dean Foods’ revenue is split 50:50 between private label and branded. It makes sense for Dean and other dairy processors to produce both because it controls a massive production infrastructure. Now, what happens when profits driven by retail consolidation allows a major customer to capture more value by producing its own commodity? In 2017, Walmart built its own milk processing plant in Indiana.

The result was a loss was an immediate 2.2% loss in net sales for Dean.

By 2017, Dean Foods owned a sprawling and expensive production footprint for a commodity CPG. People no longer demanded the product. Its customers then decided it was more cost-effective for them to produce it. A Dean Foods’ bankruptcy went from a possibility to almost a guarantee.

The Competitive Framework of the Dean Foods Bankruptcy

If you look at the milk industry from a modified Porter’s model, it’s clear the company had nowhere to go but down.

Rivalry Among Existing Competitors: Brands exists, but competition is primarily based on price — which is continually pushed down by private label.

Bargaining Power of Suppliers: Limited. Approximately two dairy farms go bankrupt in Wisconsin every day.

Threat of New Entrants: Intense. Milk is increasingly viewed as a traffic driver for groceries. Larger chains like Walmart are building their own processing plants in order to offer lower prices that drive traffic.

Threat of Substitute Products or Services: High. Health concerns and changing consumer tastes have increased the demand for milk alternatives.

Bargaining Power of Buyers: Immense. Retailer consolidation is at an all-time high leading to take-it-or-leave-it negotiations.

Political Economy: Regulated competition is no longer a priority. Policy is driven by consumer price — not competition.

It’s easy to point to changing consumer preferences as the cause of Dean Foods’ bankruptcy. After all, people are drinking less milk.

But it isn’t that simple.

By 2019, dairy processors faced incredible pressure from nearly every aspect of Porter’s model. This pressure was evolutionary; driven by a changing political economy, technology, and changing consumer taste. And remember—the same forces that caused Dean Foods’ bankruptcy apply towards every CPG manufacturer in America.