Procter & Gamble announced it would raise prices across its portfolio. P&G, which owns over 20 different billion-dollar brands, including Head & Shoulders, Crest, Pampers, and Tide, is making a bet that the power of its brands is greater than consumers’ shrinking wallets. In doing so, the Cincinnati-based consumer goods giant joins the ever-growing list of companies who plan to pass inflation onto consumers. This shouldn’t surprise many people. The announced P&G price increase is in line with what you’d expect given the company’s operations and pricing strategy.

The relationship between pricing and operations

The relationship between pricing and operations is straightforward. If a company’s product is a commodity, it won’t be able to demand higher prices. That means it will struggle to gain any cost advantages through branding and must achieve it through operational efficiencies. Outside of the decline of anti-trust enforcement, this was the core reason Walmart succeeded so rapidly. It flawlessly aligned an every-day-low-price approach with streamlined operations.

TreeHouse Foods, which specializes in private label packaged foods, earns its’ profit this way. Now, faced with rising commodity and transportation costs, the company faces sparse operating margins–around 3%. Meanwhile, P&G, which faces the same headwinds but owns powerful brands, has operating margins of about 22%.

If TreeHouse reduced operating costs by 1%, it would have a massive impact on its profitability. To achieve that same impact via increased sales revenue, it would need to increase revenue by (.01/.026) 39%. That’s not remotely realistic. Meanwhile, P&G, with its high operating margins, would need to increase revenue by (= .01/.22) about 4.5 percentage points.

The table below shows the corresponding revenue increase needed to match a one percent decrease in operational costs across a few private label and branded CPG firms. One interesting thing to point out is that Kimberly-Clark is P&G’s biggest competitor in the disposable diaper market. It also has a significant private label presence.

[table id=2 /]

What does this mean?

Typically, branded companies could drive increased sales through more trade promotions or marketing spend. Trade and marketing drive more volume. This of course comes with added cost.

However, with inflation on everyone’s mind, branded firms seem to be piggybacking on inflation. For the strongest brands, they can add potentially add sales growth entirely through higher prices.

During the investor call, P&G CEO Andre Schulten played down any operational improvement work.

Number one, when you think about cost savings projects, they require line time, that line time is competing with the need to ship cases in a very constrained supply chain. When we think about innovation, we frequently talk about our desire to close price increases with innovation. Innovation also needs line time. So cost savings projects on the line also compete with innovation, and they compete with our desire and need to ship the business. Therefore, in a constrained environment, as you point out, our businesses make the decision to focus on innovation, focus on shipping the business, which is better for retailers better for consumers, better for us in terms of value creation, but it has an impact on cost savings. The good news is these cost savings are available to us in the future; they don’t go anywhere. But you see a little bit slower ramp-up in that context.

The P&G price increase summed up

Essentially, P&G is betting that the higher prices it will charge through innovation will make up for the lack of any increase in operational efficiencies.

Now is the time to point out that P&G is estimating that organic sales revenue for FY22 will increase 4-5%, which is right in line with the simple calculation above.

In 2017, Amazon made a fateful decision. It quit being a retailer who happened to sell online and became a retail media network.

Previously, Amazon’s retail model was simple. Users searched for what they were looking for, and its algorithm delivered the relevant results to purchase. The process was fairly neutral—derived from a straightforward algorithm based on customer reviews. A better product and solid merchandising meant more sales.

Amazon’s search results had evolved from a straightforward, algorithmically ordered taxonomy of products into an over-merchandised display of sponsored ads, Amazon Choice endorsements, editorial recommendations from third-party websites, and the company’s own private brands. In some product categories, only two organic search results appeared on an entire page of results. Since brands and sellers could no longer count on customers finding their products the old-fashioned way, through the site’s search engine, they were even further inclined to open up their wallets and spend money on search ads.

This transition has been incredibly lucrative, and we’ve seen Walmart, Target, Lowe’s, and Dollar General launch their own retail media networks in the last year. According to Forrester Research, the market could be worth $50 billion next year.

What does this mean for CPG companies?

What are Retail Media Networks?

First things first, we need to define what Retail Media is. At its simplest, Retail Media is spending advertising dollars on retailers’ websites. A Retail Media Network is the platform that retailers build to manage that spend. It gets a bit more nuanced as some retailers, like Walmart and Target, have omnichannel capabilities. For example, manufacturers can bid on search results on Walmart.com and purchase in-store video displays through Walmart Connect. In Target’s case, CPG companies can buy advertisements on Target.com, Target in-store, and across NBC Universal media properties.

One way to think about retail media networks are as an evolution of slotting fees.

Traditional brick-and-mortar retailers had limited shelf space. Retailers could only hold so much physical inventory. One way to ensure management optimized revenue/square foot was to charge slotting or pay-to-stay fees. Manufacturers pay slotting fees for the right to be on the shelf. Not all retailers charge slotting fees. EDLP retailers like Costco and Walmart do not–although you could argue they just build it into the price.

Proponents would say that retailers and manufacturers are commerce partners and that the fees offset risk within the system. The reality is retailers charge slotting and pay-to-stay fees because manufacturers have no choice but to pay them. A manufacturer is reliant on the retailer to reach consumers. It makes no money if it can’t reach consumers.

E-commerce is in a similar situation. Online storefronts have unlimited shelf space, but the only real estate that really matters is the first page. Research suggests that first page results command around 91% of search traffic. Enter retail media. This real estate is incredibly valuable, and most retail media networks have some version of “Sponsored Products.” Manufacturers pay-per-click for targeted advertising with a chosen set of keywords.

Slotting

Retail Media Network

Deal Management

Centralized

Centralized

Planning Level

Category

Keyword (arguably PPG)

Shelf Management

Manual – physical store shelf

Automated

Fee Type

Fixed

Variable (CPC)

What explains the rise of Retail Media Networks?

It’s easy money for retailers.

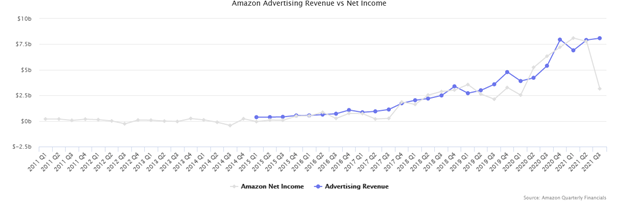

Unlike slotting, which is also easy money, individuals don’t have to stock shelves every time a company outbids another. All this income is effectively free profit. Most retail media networks are self-service portals, and the marginal cost of adjusting product search results is effectively zero. Last year, Amazon Advertising reached $7.5 billion in revenue—all profit.

Don’t believe me? Let’s take a look at its impact at Amazon. Here’s an amazing graph that charted Amazon Advertising Revenue and the company’s overall net income. There’s a clear correlation.

Are Retail Media Networks a good investment for CPG Brands?

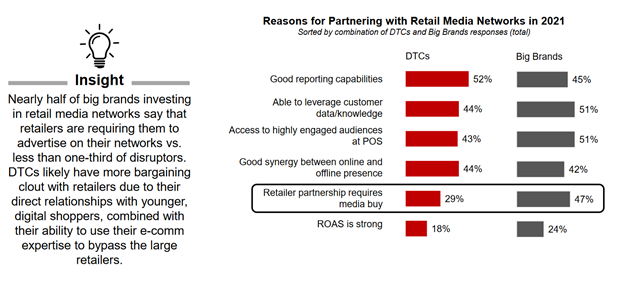

One of the more interesting aspects of the retail media network debates is this idea, often repeated by the well-intentioned analysts, is that manufacturers are okay with paying these fees because it offers unique targeting. While this may turn out to be true in the long run, it’s certainly not backed by data today.

A recent IAB survey asked CPG companies why they paid for placement in Retail Media Networks; 47% of ‘big brand’ consumer goods companies made the investments because the retailer required the media buy. Just 24% did so because of the strong return on their advertising investment.

Via: IAB Brand Disruption 2022

This sentiment is strikingly consistent across the e-commerce landscape.

Again, Brad Stone explains:

A bipartisan report by the U.S. House antitrust subcommittee would later disapprovingly conclude that Amazon “may require sellers to purchase their advertising services as a condition of making sales” on the site since consumers only tend to look at the first page of search results.

However, I don’t think that it’s all negative.

From a brand perspective, right now, the major advantage of retail media networks are twofold: First Mover Advantage and that they’re variable costs.

Right now, e-commerce is still the wild-west of consumer goods retail, and due to the reliance on algorithms, e-commerce features an inherent lock-in effect for many consumers. Once a consumer buys something through Walmart.com, the product will be forever attached to the profile—potentially locking in future sales. Since these costs are variable, rather than up-front flat fees like slotting, make it ideal for new product introductions. After all, would you rather pay $200,000 to introduce an SKU in 40 physical locations without any knowledge of its popularity or run a few targeted tests online?

What does this mean?

I think the writing on the wall is pretty clear. Retail media networks aren’t exciting avenues for growth—but rather an electronic extension of slotting fees.

On January 6, 2022, Conagra Brands held its FY22 Q2 earnings call. Overall, the quarter was worse than expected, with inflation eating significantly into profits. Operating margin dropped to 14.6%, down from almost 20% the quarter prior. However, no one is panicking as most people assume the problems are only temporary. “We expect margins to improve in the second half of the fiscal year,” CEO Sean Connolly told investors, “as a result of the levers we pulled and continue to pull to manage the impact of inflation.” One reason for optimism is Conagra Brands’ e-commerce strategy, which, combined with management’s view on competition, makes the Chicago-based company one of the more interesting companies in the CPG space.

That’s probably a weird sentence to read, and trust me, it was an odd sentence to write but stay with me. Conagra Brand’s biggest portfolio is frozen foods, a category under constant attack by upstarts and effectively incompatible with direct-to-consumer models. Birds Eye, a frozen brand they purchased in 2018, is effectively a commodity. Its most profitable category, snacks, goes against almost all health trends within consumer goods. Its last category, staples, has incredibly low margins. Management still focuses on efficiency, but as this article will show, are still focused on modern industry trends.

In a way, being outside of most trends makes Conagra one of the most interesting companies, precisely because their approach will be different than ones with brands native to new trends.

Conagra Brands’ e-commerce strategy

Conagra Brand’s advertising and promotional (A&P) spending has changed drastically over the last decade. In the past, branded consumer products companies invested heavily in television and radio advertising to build brand awareness among consumers. This can work, but it’s also really inefficient.

Recently, Conagra shifted this spending towards what I’d call algorithmic trade.

Connolly explains emphasis mine:

So I would say, we made the decision a few years back to treat e-commerce as a bit of a start-up business and we said we are going to invest in it.

So we have been, I would say, over investing relative to other areas in e-commerce because it’s far more elastic. We see the business. We get the purchases started in consumers’ basket and it’s both pure blood e-trailers and brick-and-mortar retailers who have built out their e-commerce platforms. Both of them have been very high-growth areas for us and very strong investment areas for us.

And what we found is that, there is a good ROI on these investments in e-commerce, because once we invest to kind of getting into the getting into consumer repertoire and are part of their shopping algorithm online it that translates to a repeat purchase. So, we get them when they come back whatever the purchase cycle is for that product. So that’s been one of our key marketing shift there is to go hard after e-commerce the last few years, and we are very happy with the returns and that’s why we continue to invest there.

Basically, Conagra’s e-commerce strategy involves over-investing in the initial customer acquisition with the idea that products automatically show up in users’ shopping carts. The approach is working. Conagra outpaces its’ competition in terms of e-commerce growth (note: we don’t know if this is profitablegrowth).

In a sense, it’s trade spend because they are spending money for presumably prime placement in search results. On the other hand, it’s not because it’s really about being looped into an algorithm’s recommendation cycle. Either way, it’s very smart, especially if you’re selling staples and frozen foods—things consumers don’t necessarily spend a whole lot of time thinking about.

A view on competition in packaged foods

Earlier in the call, management was asked about price increases and if they’ve experienced any pushback. The short answer is no. The longer answer is a nice statement on how consumer goods companies need to view themselves.

Connolly explains:

Previously, a consumer’s comparison of choices was between close proximity items inside the grocery store. Today, due to the demographic dynamics I talked about around young consumers’ home nesting as well as the huge move to working from home. The biggest comparison taking place from a value standpoint is between away-from-home choices and at-home choices…The comparator today is we are selling a product that might have been $2.69, and it might go up to $2.89 or something like that, versus the alternative is to go away-from-home where prices have increased even faster, and it’s $14.50.

That’s thinking ahead of the curve. Exactly what you’d expect out of a company that sells frozen peas.

Another year, another reading list. Honestly, this year might have been my worst year reading in the sense that I read a lot of bad books. 27-23 were startlingly bad. I’d go so far as to say that Guy Raz’s book is the worst book I’ve read since I started making these lists.

Superficial business advice for people more interested in talking about the glory of entrepreneurship than building actual companies. 90% of the “success” stories involve a version of the following line: “he encountered cash flow issues and had to ask his mother-in-law for a $50,000 loan.”

Blue Ocean Strategy is typically viewed as a keystone business book. It’s often brought up with the same reverence of Christenson, Porter, or Drucker. I don’t understand how this book is revered by anyone. The core thesis of the book is that instead of competing in markets with many other options (red oceans), businesses should strive to play in areas without much competition (blue oceans). Really groundbreaking stuff.

Blue Ocean Strategy is poorly researched and dependent on a variety of “gut” assumptions. One of the book’s keystone case studies is Cirque du Soleil. Now clearly, Cirque du Soleil was/is an innovative company that deserves admiration and study, but the author’s analysis of the situation is amateurish.

They write:

Whereas other circuses focused on offering animal shows, hiring star performers, presenting multiple show arenas in the form of three rings, and pushing aisle concession sales, Cirque du Soleil did away with all those factors…Similarly, while the circus industry focused on featuring stars, in the mind of the public, the so-called stars of the circus were trivial next to movie stars or famous singers. Again, they were a high-cost component carrying little sway with spectators.

The authors provide no evidence that labor costs weighed down the companies. No 10-K, no newspaper article citing a record-breaking talent deal. Instead, the idea that Cirque du Soleil transformed the industry by turning to commoditized labor is thrown out there as fact. I have a hard time believing that when circus attendance was declining, an Executive at Ringling Brothers got management into a room and was like, “Here’s the solution to our problem. We’re spending ten million dollars to sign SQUIGGLES the clown.”

A professor at a prestigious university summarizes academic research on career advancement. Most of the research was done with prestigious university graduates–meaning most of the advice is generic and useless unless you went to Stanford.

300 pages of faux-folksy anecdotes without any real insight into the creation of Walmart. It’s genuinely weird to me how this book is on a variety of “best business books ever” lists. It’s also weirdly political. A good 25% of the book is reserved for Walton’s libertarian beliefs, while another 10% is taking shots at cities.

The more I learn about private equity, the more I realize that it’s just a whole bunch of fancy words to describe a relatively simple financial model. This book paints a clear picture of the major private equity figures but sometimes trends more towards a press release than critical reporting.

Seven books that I liked but didn’t provide any crazy insight or anything.

The general premise of this book is that instead of innovation, we should really concentrate on maintaining and upgrading our existing public and corporate structures. Given that I write an operations-focused blog, you can assume I agree with this theory.

Rovell is one of the most-dunkable people on the internet, but his first book is an interesting read on the rise of Gatorade. It’s a fairly interesting story on how to commercialize a scientific product.

I don’t have much to add for what is rightly considered one of the greatest books ever written in any language. There is much to admire, but superficially I couldn’t help but draw an intellectual line from Dostoevsky to Jordan Peterson. I don’t mean that as a compliment. I did a bit of googling, and it turns out that Peterson is a big fan. Why did I draw this connection? Every female character in Brothers is a hysterical insane person, which pairs perfectly with Peterson’s ridiculous disorder/order theory. It’s darkly hilarious and fitting that one of the biggest self-help influencers of the last 10 years read classic literature and his major takeaway wasn’t about the human condition but rather that women are crazy.

It’s not as insightful and deeply reported as a few other recent corporate biographies, but Gryta does a nice job tracing the downfall of one of capitalism’s most important companies. The verdict: General Electric could overcome fraudulent accounting and bad acquisitions, but it couldn’t overcome both.

Every few years, a book comes out that breaks down the grocery industry. Each one promises a big new insight into a thousand-year industry. There isn’t one here, but it’s still a well-written and interesting look at the modern grocery industry.

A deeply reported and nuanced look at how the shipping container transformed commerce. Levinson meticulously looks at the revolution from all angles: commerce, labor, city planning, legal, socio-economic. One of the biggest takeaways was how dependent the industry’s evolution was on regulation. It’s almost as if politics plays a huge role in commerce.

Both of Stone’s Amazon books are must-reads for anyone who lives in America. I’d argue that they’re required reading for anyone who works in the retail industry. The first book looks at how Amazon amassed the power it has. The sequel looks at what Bezos did with all that power. One very interesting dynamic here is the rise of advertising within Amazon. It’s a more powerful and efficient AWS.

It’s hard to imagine that there could be a story written about big tobacco where big tobacco isn’t the villain, but the one saying, “hold on, this might be dangerous.” But that’s exactly what happened in the case of Juul. For those that don’t know, according to its founders, Juul was created to help smokers switch from harmful cigarettes to less harmful vapes. (Note: I find this origin story preposterous) Juul then applied some Silicon Valley moxy to the industry. Juul’s version of moving fast and breaking things was explicitly advertising nicotine to children. In the end, a smoking substitute ended up ensnaring a new generation.

Every so often, business books come along that not only tell a company’s story but reveal how it happened. It’s one thing to say that a company looks to delight customers. It’s another to define “delight” and then describe how a company defined a qualitative idea at scale. Behind the Arches is one of those books. It not only tells the story of McDonald’s evolution, from a small California drive-in to an international corporation, but it describes in painstaking detail how it did so.

At times the book turns into deification, but honestly, it’s kind of understandable. Prior to McDonald’s, there were very few successful chain restaurants. The biggest was probably Howard Johnson, which was a sister company to a hotel chain. The reason was, how do you operationalize and scale food service? It’s one thing to produce an item at scale; it’s another to produce a service.

General Mills had a fairly good quarter, continuing a string of success that most branded consumer goods companies have had over the pandemic. It had $5 billion in revenue over the last three months, 6% higher than the year before. However, profit declined 13%–caused mostly by inflation. How does the Minnesota-based company plan to get that profit back? During its’ recent investor call, General Mills made it clear it will use its pricing power.

What is pricing power?

There’s a lot of different technical definitions of pricing power within the consumer goods industry. It’s a high stakes game with billions of dollars at risk. At a high level, brands want to charge as much as possible for products, but not too much where it impacts the overall demand for it. This interplay between price and demand is called elasticity.

Products whose demand doesn’t change much with price are considered inelastic. When demand for a product is heavily influenced by the price it is considered elastic. Products that feature an inelastic demand have pricing power.

Given increased inflation, it’s a great time to have pricing power. General Mills has it. In the last few months, the company has increased prices by an average of 9% across North America. Executives don’t comment on forward-looking prices, but CEO Jeff Hermening said more increases are coming. “We have pricing already in the marketplace that we’ve already announced to our customers,” he told investors, “and so we’re confident that, that it will be higher in the second half of the year. “

Why are higher prices coming? Quite frankly, they can, so they will.

Pricing, reality vs perception

According to General Mills, price increases are due to inflation. “We’ve seen about half a billion dollars more in costs than we were expecting this year,” chief executive Jeff Harmening told investors. This is more or less standard across the consumer goods industry. But what are the costs specifically? Kofi Bruce, General Mill’s CFO explained:

About 55% of our input costs are sitting in raw packaging materials, 30% in manufacturing and the remainder in logistics.

And what we really saw that kind of accelerated was our raw and packaging materials moving out to double digits, logistics which we now expect to was already in the double digits, continued to survive the loss of that base, and in fact remained in the low single digits.

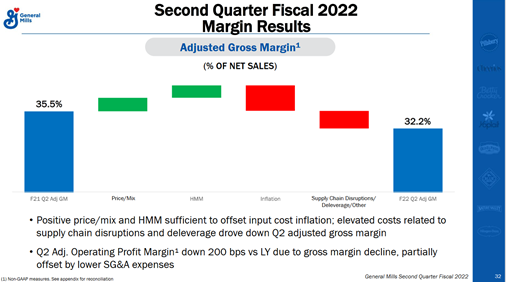

This is certainly true. A look at General Mill’s margin waterfall shows inflation has a large impact on margins. It also shows that it’s been able to offset inflation through a mixture of pricing and HMM (holistic margin management).

In How Brands Grow, Bryon Sharp explains the concept of a reference price.

The academic research on pricing emphasizes the notion of a consumer reference price—especially the consumer’s internal reference price, which is the memory or expectation of what prices should be.

In the case of TreeHouse Foods, it manufactures products that compete strictly on price. Its reference price will always be of a low-cost alternative. Its demand will always be somewhat elastic. General Mills competes on quality and brand. Its products are more inelastic.

Sharp continues:

This expectation of price is thought to be generated by exposure to prices in the past, either by purchasing or observing communications such as ads. The idea of a reference price is that ‘past prices matter’ and if consumers encounter a price above their reference price, this dampens their propensity to buy.

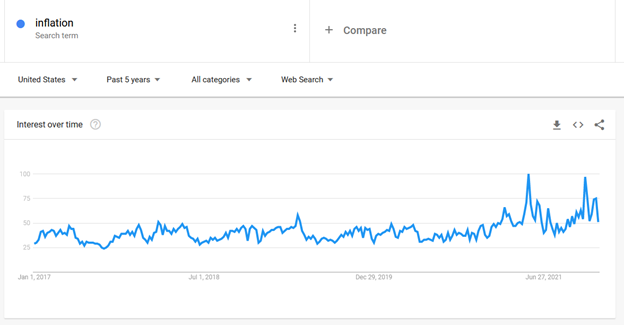

In this case, the reference price is distorted, not through advertisements, but through media talk about inflation. The image below shows Google searches for “inflation”. As you can see, it’s skyrocketed over the last few months. People believe inflation is widespread, and so they’ve adjusted their attitudes to expect price increases.

Since General Mills has inealstic products with pricing power, they’re exercising it. TreeHouse Foods isn’t so lucky.

Something weird happened this year. There was a great cream cheese shortage that occurred overnight. Seemingly without warning, cheesecake producers and bagel shops were stuck looking for a product that was a dying category a decade before. Yes, you read that right. Cream Cheese was a dying category in the recent past.

In 2010, after years of stagnant sales, Kraft enlisted Paula Deen to boost Philadelphia Cream cheese. She was set loose on America’s morning shows promoting a cooking competition. It was a tremendous success for the legacy brand, generating a 5 percent sales increase in just two years. The competition quietly ended when Deen announced she had diabetes.

Fast forward ten years, and cream cheese consumption is through the roof. Foodservice sales are up 35% and at-home consumption is 18% higher than 2019. The result is a cream cheese shortage for America’s bagel shops. In the last two weeks, USA Today, New York Times, and Bloombergran articles looking to explain the central question: why is there a cream cheese shortage?

Why is there a cream cheese shortage?

It depends on who you ask. Most articles have focused on three key factors: increased demand, the quick churn nature of dairy, and a cyber-attack.

Increased Demand

People are working from home and buying more cream cheese for their morning bagels. Combined with the holidays (which feature a lot of cream cheese in certain deserts), people are just buying more cream cheese, and manufacturers can’t keep up.

Quick Churn

Unlike other shelf-stable products, manufacturers can’t stockpile cream cheese for later sales because it’s dairy and has a quick expiration date. What they make goes out the door almost instantly.

Cyber Attack

Schreiber Foods, a privately held dairy processor in Wisconsin, was the victim of a cyber attack in late October. The company stopped production for about a week after hackers took control of its facilities. It may seem like a small event, but Schreiber is such a large cheese processor that it plunged the industry’s spot market by 17%. All of that production was off the market.

Why Manufacturer / Retailer Relationships matter

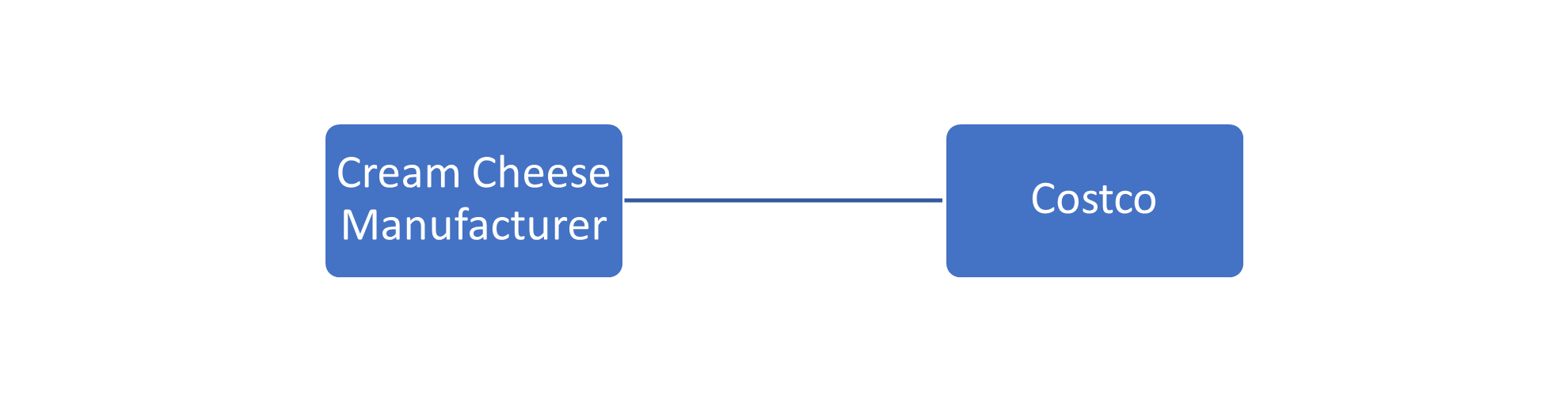

One thing none of this analysis touches is the power dynamics at play. Cream cheese shortages haven’t been spread equally across the market. Take this comment from Richard Galanti, Executive Vice President and CFO of Costco, in last week’s investor call:

I mean I had — it was a little bit of a chuckle at a call just yesterday from a reporter asking about how are we doing on cream cheese. And so I checked, and we’re — there’s a cream cheese shortage out there, and the bagel shops are being challenged. We actually got — as the buyer said, it took a little extra work, but we’ve got all the cream cheese we need. So I think we’ve done a good job in merchandising.

You may be tempted to agree with Galanti, that Costco’s buyers are just a bit better than others. I’m sure they’re talented, but a hidden issue here is power.

Costco is a large retailer that places massive bulk orders of cream cheese. From a manufacturer’s perspective, it’s considered a Direct account. A Costco buyer works directly with the manufacturer to place an order. Costco orders enough that the manufacturer probably has an internal sales team to manage an account. Not only does Costco’s large order give it the pricing power to demand discounts, if something goes wrong with a delivery or an order, Costco can contact a person who solves the problem.

Typical Direct Relationship

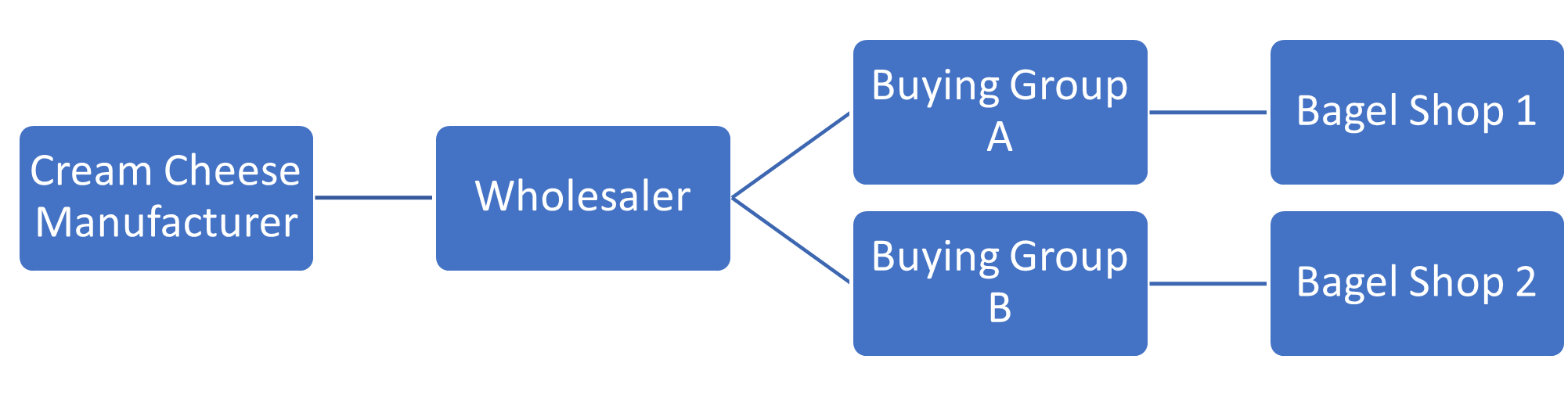

A random bagel shop has a different experience. From a manufacturer’s perspective, they probably don’t even know that a bagel shop orders their product. Rather, the manufacturer sells products to a wholesaler (C&S, Sysco, and US Foods are major wholesalers) who then sell and deliver the cream cheese to the Bagel Shop. Within the CPG industry, wholesalers are considered indirect accounts.

Typical indirect food service account.

Where it gets kind of complicated is that within each wholesaler are different buying groups. Buying groups are basically price discounts that wholesalers offer customers based on volume or bundled products (e.g., get 5% off if you purchase $100,000 or more or get 3.5% off if you are buying all your dairy from the wholesaler). They’re typically one-year contracts.

The Bagel Shop is competing for attention with shops inside and outside its buying group. If something goes wrong with an order, the Bagel Shop can’t contact the cream cheese manufacturer directly; rather, it works through the wholesaler. Complicating matters, typically, a manufacturer will outsource the management of wholesaler accounts to third-party brokers, who receive a yearly management fee based on a percentage of sales.

Basically, if something goes wrong with Costco, they’re a phone call away from a solution. If something goes wrong with the bagel shop? Well, it’s going to be a while.

Sure. I’m sure Costco has tremendous buyers, but having a direct line to the manufacturer helps explain why they’re flush with goods and others are stuck with out.

The last six months or so have seen an explosion of news articles about rising retail theft rates.

The general narrative across most media organizations is that shoplifting/retail theft is getting out of control and causing retailers to close stores and adjust financial expectations. Last week executives at Best Buy, a $52B retailer, reported that retail theft was beginning to impact gross margins. Now there are plenty of reasons to be skeptical of the rising retail theft narrative. The biggest is that from 2010-2020, the FBI’s own robbery data shows that cases have declined by a third.

Retail lobbyists and their Tough On Crime allies have found an extremely effective narrative vehicle to undermine Black Lives Matter and criminal legal reform efforts, and they will almost certainly attempt to duplicate it elsewhere for years to come.

Now I don’t know if retail theft has skyrocketed post-pandemic. I find Johnson’s argument plausible. I also find it equally likely that it is rising, but we’re just experiencing a data lag in incident reporting. With that in mind, earlier this month, there was some very interesting testimony from Brendan Dugan, the Director of Organized Retail Crime and Corporate Investigations at CVS. Dugan was testifying at the Senate Judiciary Committee’s hearing on “Cleaning up Online Marketplaces.”

He begins his testimony by outlining some key statistics surrounding retail theft rates. According to CVS internal data, it loses $200 million every year due to retail theft—with an average take of $2,000 per incident. In 2020, CVS’s Retail/LTC (Long Term Care) segment reported revenue of $91.2 billion, and about $21 billion (23 percent) of that revenue was from retail sales. Using these numbers, a rough calculation reveals that retail theft accounts for about one percent of that segment’s sales.

Dugan pivots to describe how retail theft rings operate. He makes it clear that there’s a difference between shoplifting and retail theft. In retail theft, a Booster steals goods from a brick-and-mortar store, and the stolen merchandise is sold to a Fence who off-loads it to online resellers who sell the products on Amazon to consumers. “When stolen goods make their way online,” he told the Senate Committee, “the unsuspecting customer has no idea the product they just purchased was stolen.”

He continues:

Last year, my team identified and resolved over $40 million in e-commerce fraud across all online marketplaces. Our biggest case last year involved a business named D-Luxe that sold over-the-counter drugs on Amazon. D-Luxe was listed as one of Amazon’s “Top Rated Sellers.” The company was owned by a man named Danny Drago. He was known by boosters and fences as “The Medicine Man.” CVS Health investigators were led to Mr. Drago after weeks of surveilling booster activity in the San Francisco area brought them to a warehouse in nearby Concord, California.

Dugan then describes how Amazon was uncooperative with the investigation and claimed it had no information to offer even after the local police department issued Amazon a subpoena. Generally speaking, I am pro-privacy and appreciate the spirit of Amazon’s stance. However, it’s easy to contemplate that perhaps the company is more interested in protecting its business model of a largely unregulated and unmonitored network than adherents to a strict privacy policy.

Later:

Mr. Drago and his wife were involved in a nearly $40 million operation which operated at least two Amazon accounts, selling more than $5 million a year in stolen goods on Amazon and through multiple other Amazon sellers. Amazon suspended one of their accounts in 2019 but did not close the other accounts operated by Mr. Drago or the associated sellers until weeks after the CVS Health investigation resulted in his arrest and seizure of the stolen goods.

So to recap, CVS alleges that it uncovered an Amazon seller account selling over $5 million a year in stolen goods. CVS worked with the local police department, which resulted in the perpetrator’s arrest and recovery of the goods. Amazon did not fully remove the Seller from its listings until weeks after the Seller was arrested.

I can’t help but be reminded of a section in Brad Stone’s Amazon Unboundthroughout this story.

In it, Stone describes one of Amazon’s key operating principles: leverage. Amazon is willing to invest hundreds of millions of dollars in technology systems if it means it can remove humans from the operation of the system. It started when Amazon automated its own procurement system and quickly spread across the organization. It’s currently the key driver of its third-party Seller ecosystem, which accounts for over 60% of the company’s retail sales.

Stone writes:

Building such systems required a significant up-front investment and added to Amazon’s fixed costs. But over the ensuing years, those expenses paid off as they replaced what would have been even larger, variable costs. It was the ultimate in leverage: turning Amazon’s retail business into a largely self-service technology platform that could generate cash with minimum human intervention.

If you combine Stone’s reporting and Dugan’s testimony, it’s clear Amazon has limited systems in place to ensure the chain of custody of its merchandise. This is a deliberate design decision, made to maximize Amazon’s profit. Amazon’s devotion to leverage has already had a serious impact on CPG innovation. It seems likely that its pursuit of leverage may have created the nation’s largest clearinghouse for stolen merchandise.

Suppose it turns out that organized retail theft is on the rise, and authorities are serious about stemming it. In that case, policymakers should look not at individuals on the ground but at the legitimate business networks that facilitate it.

If you’ve been paying attention to any branded consumer goods company’s COVID-era financial returns, you’ll notice a familiar refrain: Things are crazy, but overall, business is going great. Private label companies? Not so much.

Before discussing the company’s financial results, CEO Steven Oakland led with a bombshell. The $4.3 billion private label product juggernaut, which makes store brands for everyone from Walmart to Wholefoods, is looking to sell off its largest division—meal prep. “We have talked about those businesses as growth engines and cash engines,” Oakland told investors. The meal prep division, which includes products like condiments and mac-and-cheese, is a cash engine. It produces relatively low-margin staples that generate a lot of cash as products fly off the shelves. TreeHouse can use that cash to in higher-margin products within its snack and beverage portfolio. If that sales goes through, “We would simply have that cash available sooner and be able to execute that strategy a little faster.”

How TreeHouse Foods is currently structured. Via 2020 Annual Report

To understand why management is pursuing this new strategy, it’s best to take a step back and look at three things: The value proposition for a private label company, the operations that enable it, and how COVID upended it all.

A private label company’s value proposition

Private label brands have been around for about as long as large retail stores have existed. Private-label goods are nothing new, of course,” Matthew Boyle wrote in Fortune Magazine back in 2003, “having been around since the days when A&P owned vast coffee plantation in South America.” For most of the 20th century, private label was associated with cheapness and low quality. Then, in the last 30 years, something changed.

He continued:

Retailers—once the lowly peddlers of brands that were made and marketed by big, important manufacturers—are now behaving like full-fledged marketers. And here’s the earthquake part: It is their brands—not those of traditional powerhouses like Kraft or Coke—that are winning over the (consumers) in the greatest numbers.

Private label manufacturers produce products that retailers can then brand under their own umbrella. However, most retailers don’t want to own their own factories, and with few exceptions, they rely on companies like TreeHouse foods for that. This setup worked pretty well before COVID-19. In the years leading up to the pandemic, sales of private label products typically grew at twice the rate of branded products.

The operations of a private label company

Since private label companies don’t handle the sales or marketing of their products, the companies have different core competencies than branded CPG companies.

1. Research and development: Creating a product that consumers want.

2. Production: Figuring out how to manufacture the improved product at scale.

3. Supply chain: Ensuring that you have enough raw commodities to manufacture the product.

4. Transportation: Getting the product to the customer (retailer).

5. Sales: Ensuring the product gets prime placement for a customer through negotiations and pricing.

6. Marketing: Generating consumer awareness and demand through advertising

The result is:

Consumers get relatively high-quality and low-cost products.

Retailers capture higher margins and generate brand loyalty through their own offerings (think Costco and Kirkland).

Private label companies operate as manufacturing partners and supply chains for retailers.

How COVID upended the private label business model

If you’ve followed this blog, you’ll know that branded CPG companies have excelled in COVID by maximizing each business process outlined above. Due to the nature of private label products, TreeHouse Foods can’t. “One thing I think to remember about us,” Oakland told analysts, “Is that we are only a supply chain business. We don’t have marketing levers. We don’t have many of the other levers that you have in your branded lives.”

Here are the levers he is referring to.

TreeHouse Foods couldn’t increase production to meet demand through third-parties.

When the initial lock-down started in March of 2020, panicked consumers flooded retail outlets. Stock-outs of common products became a regular occurrence as manufacturers couldn’t keep pace with demand. Most branded consumer goods companies opted to subcontract the production out to third parties to deal with the onslaught. In the case of General Mills, it added 50 additional partners to its production capacity. “If demand starts to taper off, that is the capacity that we will shed first,” Kofi Bruce, the CFO of General Mills, told the Wall Street Journal. Since TreeHouse Foods was the one making the already low-margin products, it didn’t have that luxury.

Faced with overwhelming demand and production constraints, managers at branded CPG companies embarked on SKU rationalization projects. “We’ve made some choices in our supply chain to — we’ve reduced some of the tail of our portfolio,” the CEO of Pepsi told investors back in July 2020. The company met with its retailers and prioritized production of the best selling SKUs. “We both agreed that it’s probably the best thing to do, to eliminate the smaller SKUs in the portfolio to maximize the best-selling SKUs and be in stock.”

Private label companies were out of luck. Since they’re focused on producing basic products, their SKU assortment is relatively limited.

In frozen waffles, TreeHouse temporarily cut flavored ones, like chocolate chip, to focus on making the basics. The leading brand, Kellogg’s Eggo, suspended production of more obscure varieties and continued selling popular flavors like chocolate chip. TreeHouse’s frozen-waffle sales took a hit as a result, Mr. Oakland said.

Private label products have less pricing power.

Most branded consumer product companies have raised prices to offset rising covid-19 induced inflation. The smart ones have used revenue growth management techniques in a targeted way that boosts profitability.

Kimberly-Clark is looking to leverage these same insights. RGM will bring in reams of data that will allow them to understand opportunities. Currently, a 32 pack of Huggies is $8.29 at Target online. Given the current level of online competition, it seems unlikely that the company could increase this SKU price.

However, done right, RGM will allow K-C to understand the true cost of selling at each customer—by SKU. RGM uses a variety of COGS, Transportation, and Trade data to reveal profitability. Maybe they can increase the base cost of a less popular item by 25%, but make up the lost volume with a promotional coupon on the 32 pack.

TreeHouse Foods doesn’t have this flexibility because its products are unbranded. In fact, the cost of producing each item is rising, but the retail price is staying the same. TreeHouse Foods is taking this cost increase! Management claims it’s to maintain good relations with their customers, but in reality, the retailers hold power in the relationship and there isn’t another option.

Private Label products aren’t optimized for E-commerce.

In 2021, it’s anticipated that online grocery sales will reach $100 billion. Unfortunately for private label manufacturers, the private label industry isn’t optimized for e-commerce.

Private labels products mainly differentiate through price. Once consumers are in a retail store, they compare and contrast products side-by-side. E-commerce isn’t optimized for that. It’s optimized for keywords, and mobile ordering often shows one product (often promoted) at a time.

In conclusion

In 2014, I wrote an article on Li & Fung, the massive Asian supply chain magnate. In it, I argued that their business model was becoming obsolete. Its reliance on just-in-time production across multiple borders made it especially susceptible to the shocks associated with climate change.

The question is, what will Li & Fung do? Their product isn’t soda or shoes. It is a network that is dependent on the system that is becoming unstable. If they don’t change, they will go from the company that no one knows about to the company no one cares about.

You can lump the current iteration of TreeHouse Foods into that category. Its entire business model was built around acquiring a massive production infrastructure to produce unbranded products.

I think management would agree.

“We had built this supply chain designed for tremendous efficiency but very low volatility,” Steven Oakland said. “When the pandemic hit, we had complexity meet volatility.”

The recent Keurig Dr. Pepper (KDP) earnings call focused on the popular industry topics of late: Supply chain disruptions, commodity inflation, and transportation shortages. With sales up almost 7%, the company is doing a solid job managing all three. There was one point in the Q&A that I found very interesting. “We think our DSD asset is a competitive advantage,” CEO Robert Gamgort told analysts, “We’ll look for ways to continue to consolidate distribution and drive more efficiency and effectiveness through that really important asset to us.” It’s clear that to Gamgort, Keurig Dr. Pepper’s strategy is guidedby its route to market strategy. To understand its strategic importance, you need to understand KDP’s broader route to market strategy.

What is a Route to Market strategy?

Stated simply, a route to market strategy is how a company plans to get its product in a position where consumers can purchase it. It doesn’t really matter if a company has a phenomenal product if consumers don’t know about it or can’t find it to buy. It also doesn’t matter if it has a great product that is readily available if the cost associated with the first two are exorbitantly expensive.

In the consumer goods world, a route to market strategy typically entails generating consumer demand through advertising and then selling goods to a customer (retailer) and delivering them via a 1. direct shipment to the retailer’s warehouse, 2. direct-store-delivery (DSD) or 3. wholesaler who acts as a mixture of 1 and 2.

The Keurig Dr. Pepper Route to Market strategy

From a high level, KDP’s RTM strategy doesn’t look like a strategic asset. In fact, it’s what you’d assume any beverage company would look like. Note, brands fit into each one of these strategies differently. For example, company-owned DSD is dominated by brands Snapple and Bai. In 2018, around 40% of Dr. Pepper volume was through the hospitability route.

Company-owned DSD: A fleet of KDP owned trucks that deliver goods directly to stores. The truck drivers act as account managers, who do everything from unloading products onto shelves to negotiating sales deals.

Independent DSD Partners: Like Company-owned DSD. These partners typically concentrate on territories the manufacturer lacks a footprint, or on small niche retailers.

Cola System: Coke and Pepsi-affiliated bottlers buy concentrate, manufacture soda, and distribute it within their areas. Dr. Pepper is the major brand here, and a National Accounts team manages it.

Warehouse Direct: The company ships the product directly to retailer warehouses. This is mostly smaller brands like Hawaiian Punch.

On-premise, Office, Hospitability: Think fountain systems and other foodservice arrangements. Unlike Coke and Pepsi, Dr. Pepper isn’t restricted by franchise agreements and can be placed in both Coke and Pepsi systems.

E-Commerce: Sales directly from the Keurig Dr. Pepper website. The lynchpin of this route is Keurig. It has built a rare ecosystem around a self-service machine and recently launched the Supreme Plus SMART platform—which features auto-replenishment. Overall, this category is now over 10%.

How does Keurig-Dr. Pepper maximize each route?

Technology basically.

According to the KDP investor day presentation, the company has made substantial technology investments that allow it to optimize each route. Here’s an example for the Company-owned DSD-system.

KDP has a platform that tracks sales to each individual retailer. Before each sales call, the system generates a recommended order based on past sales.

This recommended order is fed into a customized handheld system. A recommended driving route is generated, as are different promotional options.

The salesperson negotiates a deal with the customer, using recommended pricing, and promos—after driving to the retailer in the most efficient way possible.

They take pictures of the shelves using the handheld—which are then analyzed by corporate.

An innovative Route to Market strategy

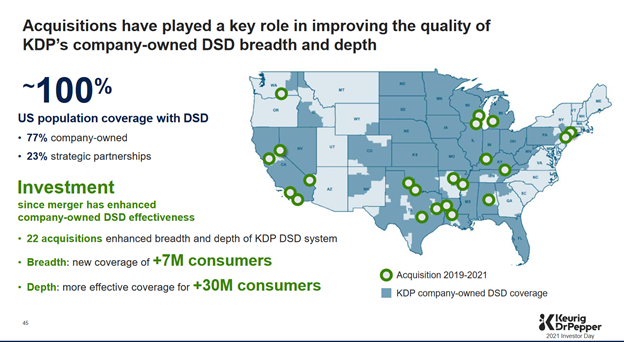

Here’s why I think KDP’s RTM plan could be exceptional. Keurig Dr. Pepper has executed a series of strategic moves to build out the company’s DSD system. From 2019-2021 the management acquired 22 different companies, adding delivery coverage for 7 million consumers in the process. Thinking ahead, this network gives the beverage company the potential ability to bypass retailers and third-party shipping fees—delivering products directly to consumers.

via KDP’s 2021 Investor Day presentation

More exciting is that KDP can sell access to this network to other manufacturers. This is exactly what the company did in 2020 when it signed a distribution agreement to double their volume in New York and New Jersey. “We’ve been putting more volume through our system,” Gamgort told investors during a recent annual meeting. This volume not only improves their return on invested capital but is a key driver of the company’s overall strategy. “We brought in more partner brands, and importantly, we’ve brought in a number of territories that have actually added volume to our existing territories.”

It may have turned a traditional cost into a stream of revenue.

If you live on earth, you’ve purchased consumer goods. After a manufacturer takes raw ingredients and processes them into a final product, any item purchased and utilized by a consumer is considered a consumer good. Flour, plastic cups, alcohol—all consumer goods.

Suppose you want to view things from an economic lens. In that case, everything you buy and consume within three years is considered a non-durable consumer good. Everything that you purchase and use for more than three years is regarded as a durable consumer good. Deli meat, pencils, and cleaning supplies? Non-durable consumer goods. Clothes dryer and microwave? Durable consumer goods. I mostly write about non-durable consumer goods companies and the strategies they use to make money. I’m not particularly unique. When most people talk about consumer goods, they’re talking about the nondurable kind.

Classification is always somewhat flexible. Newell Brands is a major consumer goods company with over $14 billion in annual revenue. One of Newell Brands’ keystone brands is Rubbermaid, and Rubbermaid storage containers will last well over three years. However, most people still consider the Georgia-based company a consumer goods manufacturer. If you can buy it at Walmart, Target, or Amazon, it’s probably a consumer good.

Given that you purchase consumer goods every week the companies who make them are incredibly powerful. When thinking and analyzing those companies, it’s helpful to break them into distinct categories, where NAICS codes come in.

NAICS Codes and Categorization

One of the standard ways to categorize and organize consumer goods companies is through the North American Industry Classification System—NAICS codes for short. NAICS codes are a joint classification system developed by the US, Mexico, and Canada. It’s an attempt to organize a variety of economic activities into a hierarchy. The top of each hierarchy is incredibly broad, with more granular detail in each subsequent level.

Here’s an example of how you could classify General Mills.

NAICS Code

Name

Level

31-33

Manufacturing

Sector

311

Food Manufacturing

Sub-Sector

3112

Grain and Oilseed Milling

Industry Group

31123

Breakfast Cereal Manufactring

NAICS Industry

Like the Newell example above, General Mills is a massive company that crosses many categories. Not only does General Mills sell Cheerios, but it also sells Pillsbury (3118 – Bakeries and Tortilla Manufacturing) and Hagen-Dazs (3115 – Dairy Product Manufacturing). For this reason, when you’re comparing and analyzing General Mills against other companies, it’s probably best to compare companies at the Sub-sector or Industry Group level.

Who are the major consumer goods companies?

The consumer goods industry is immensely profitable and competitive in America. It generates about $654 billion each year and accounts for 34 companies on the Fortune 500. The table below contains the 34 consumer goods companies on the Fortune 500 list, along with their corresponding subsectors, revenue, profit, and net profit margin.

[table id=1 /]

Judged by revenue, the top ten are dominated by food, beverage, and tobacco manufacturers. Branded homegoods giant P&G is the only company to reach the top 10 (coming it at #1).

But metrics matter. Suppose you sort the table by net profit margin (how much profit is generated by each $ of revenue). In that case, chemical consumer goods companies occupy three of the top ten. Ask yourself, why the sudden change?

There are many correct answers to the question above, but I hope that after reading this article, you now understand what consumer goods are and why categorization is important when analyzing the major companies.