How did things go so wrong for Kraft Heinz, one of the nation’s largest, most recognizable food companies that’s backed by one of the nation’s most beloved investors? In February, Kraft Heinz announced a 2.7% decline in net sales for 2019. This comes just one year after the company wrote down $15.4 billion because legacy brands like Oscar Mayer and Kraft failed to keep up with changing consumer tastes. Its long-term debt was downgraded to junk bond status after management refused to cut its dividend. Oh, and it also was investigated by the Securities and Exchange Commission for misrepresenting financial results.

During a scheduled conference call reviewing the past year, CEO Miguel Patricio told investors that “2019 was a very difficult year for Kraft Heinz.” The situation is a far cry from just four years ago when the company headlined its annual report “Kraft Heinz Reports Solid Financial Performance with Integration on Track.”

So what happened? To understand Kraft Heinz’s fall, you need to understand how the company came to be and how its strategy and approach to budgeting differs from the traditional model of a consumer packaged goods (CPG) company.

Private equity comes to town

This all goes back to when 3G Capital, a Brazilian private equity firm, entered the picture in 2013. The firm had earned itself a reputation for generating profits. Like most PE firms, its model was based on cash flow and cost cutting. The general strategy looked like this:

- Identify an established brand that 3G management believed it could manage more efficiently.

- Acquire it with other people’s money.

- Maximize its efficiency through cost cutting.

- Use the resulting profitability to finance additional deals.

The firm had used the formula to turn Burger King and Budweiser into cash machines; it sold 1,200 Burger King locations to outside investors and reduced the head count by almost 36,000. In three years, net income rose 34%. “These things are seemingly working at Burger King,” an analyst told Businessweek in 2014, “and causing questions to be asked about the strategy of others in fast food.”

With financing from Warren Buffett, arguably America’s most respected investor, 3G gained control of H.J. Heinz for around $23 billion in 2013. Two years later, the group acquired Kraft for $49 billion. The result was the fourth-largest food company in America with a roster of stable brands, including Oscar Mayer, Jell-O, Maxwell House, and Planters. “This is my kind of transaction,” Buffett said after the deal went through, “uniting two world-class organizations and delivering shareholder value.”

Financial Times describes what happened next:

Since 2013, more than 10,000 people — one-fifth of the workforce — have been laid off from Kraft and Heinz, with seven plants shut, highlighting the human cost and upheaval involved in producing the highest profit margins in the food industry. The founders of 3G have transformed the beer, fast food, and food manufacturing industries with bold acquisitions, which are quickly followed by a brutal but disciplined attack on costs, a surge in profitability, and high returns to shareholders.

The “brutal but disciplined attack on cost” has a name: zero-based budgeting. The logic behind it is compelling while being simultaneously against the branded CPG industry’s entire business model.

How zero-based budgeting works

Traditional corporate budgets are derived from historical information. Imagine that you’re in charge of in-store marketing at Kraft. Last year, you spent $15 million on a variety of in-store marketing events. After analyzing inflation, competitor data, and new item distributions, you estimate you’ll need an additional $500,000 in funding to support the business. Your boss agrees, so you get the budget.

Zero-based budgeting doesn’t work that way. In zero-based budgeting, every single company expense (from in-store food samples to pencils) is classified into a specific category. Each category is assigned a manager who builds a budget from scratch, justifying every single expense. Budgets are analyzed and awarded a cap. Managers are then incentivized based on how much they spend under the cap.

The result is a ruthless accounting of company expenses.

In the first few years, Kraft Heinz eliminated over $1.7 billion in annual spending. This included excessive expenses like private executive jets. It also included eliminating things that don’t cost a lot, like taking away free Kraft snacks in break rooms and limiting each employee to 200 printed pages a month. Workers may have hated it, but investors loved it. According to Berstein Research, for every dollar of sales, the food industry typically earns about 16 cents. Eighteen months under the new regime, 3G was earning 26 cents for every dollar it sold.

There’s nothing inherently wrong with documenting and assigning responsibilities to spend. In fact, 10 to 15 years ago, you could almost certainly make the argument that many CPG firms were bloated. But the problem with this approach is threefold:

- It assumes the underlying brands independently operate with stable and strong business infrastructure — and that both are capable of doing more with less.

- It discounts the fact that legacy brands — almost all of Kraft Heinz’s portfolio — require promotional spending to maintain past sales performance.

- It fails to take into account that businesses aren’t linear. They are a collection of interdependent processes, each one influencing and impacting the bottom line in aggregate. It isn’t always possible to account for and rationalize every single expense because the results are often dependent on numerous factors.

In year one, a cut in marketing and promotional spending may not impact much. Change doesn’t happen overnight. The initial success means the cuts are repeated for three straight years — because why not? The manager is incentivized to cut. Everything is fine until reality catches up. A legacy brand with reduced promotional support in an ever-changing category is a recipe for disaster. Suddenly, sales stop and management is forced to take one of the largest write-downs in a decade.

Creating true value

CPG companies are valuable because of the sum of their interlocking parts. A company can have the best product in the world with a great marketing campaign, but what does it matter if it can’t consistently manufacture it? The following major business processes drive consumer product companies:

- Research and development: Creating a product that consumers want.

- Production: Figuring out how to manufacture the improved product at scale.

- Supply chain: Ensuring that you have enough raw commodities to manufacture the product.

- Transportation: Getting the product to the customer (retailer).

- Sales: Ensuring the product gets prime placement for a customer through negotiations and pricing.

- Marketing: Generating consumer awareness and demand through advertising.

Zero-based budgeting is about making each process the most efficient version of its current state. But despite how zero-based budgeting operates in theory, business processes aren’t independent. Businesses typically get a greater return on sales spend if they’re backed by a marketing campaign and vice versa. Some processes, like research and development, are not linear. It may take years for a product innovation to break through.

For an example of a more successful way to acquire a company and integrate it into the core processes — rather than trying to grow through cuts — we can look at what happened with P&G and Charmin.

Building new value through acquisition

In 1957, P&G acquired a Green Bay, Wisconsin-based papermaker named Charmin. At that time, Charmin wasn’t the national powerhouse we know today. It was a regional afterthought with about $20 million in sales. To put the acquisition in perspective, P&G had an advertising budget of over $80 million the same year.

Like the more recent Kraft Heinz deal, the logic for the acquisition was compelling. Acquisitions are evaluated based on how well they plug into a company’s existing operations and strategy — both vertically and horizontally. Vertically, P&G had technical experience with pulp-making, a key component of papermaking itself, through the Buckeye Cotton Seed Oil, a company it owned that manufactured component materials for film. Horizontally, it had a long history — first with soap, then with detergent — in marketing and distributing low-cost consumer products. On paper, everything looked fantastic. P&G had both the technical and business skills to build the brand.

What could go wrong?

For starters, Charmin wasn’t a product consumers wanted. Today it’s the most popular branded toilet paper in America, but in the 1950s, it regularly placed last in blind tests against products from paper powerhouses Kimberly Clark and Scott Paper. The poor quality meant that Charmin only controlled about 14% of the Midwest and Great Lakes market. Out-of-market retailers weren’t willing to give shelf space to a product that couldn’t win in its own territory.

When P&G went up to Green Bay, it realized that Charmin failed in just about every process — specifically production. Rising Tide, the history of P&G, explains:

Charmin benefited almost immediately from P&G’s more sophisticated financial and marketing techniques, but the transfer of technical knowledge proved troublesome. At the time, papermaking was considered an art, in the same way soap making had been earlier in the century. Charmin “had no clearly established product or process standards.”

Despite having technical paper experience, P&G struggled to develop a new product. Mass production requires a strong paper to withhold against the stress of the pushing and pulling of papermaking machinery. But making it strong meant a thicker, harder paper — not exactly the words people want to be associated with toilet paper.

After years of experiments, P&G engineers developed CPF, a paper manufacturing process based on a Japanese technique that involves inserting an air drying step into the manufacturing process. CPF resulted in a softer and more absorbent paper that had a cheaper per-unit production cost than traditional methods. Rival firms got wind of the new process but were powerless to respond because they were locked into extensive and costly legacy manufacturing systems.

Adapting existing processes

Investing in research and development and production processes resulted in P&G having a better product, but retailers didn’t want to sell it. Competitors made sales presentations that showcased how poorly the old version of Charmin performed. “Who needs a brand that’s been on the market for five or six years and is a weak number two or a weak number three in its category?” P&G’s former sales director later told interviewers.

This is where P&G’s existing horizontal sales and marketing processes came into play. P&G put its marketing skills to use, inventing a new branding campaign, “Don’t squeeze the Charmin.” It then redesigned the packaging. Toilet paper was traditionally sold in opaque paper packaging. Charmin marketers put it in clear plastic, creating an attention-grabbing effect on the shelf.

Armed with a superior product, a revamped brand, and better packaging, Charmin launched pilot programs in select cities. Within months, Charmin climbed to the top of each test market. The initial success gave sales representatives a story to sell. It’s hard to imagine now, but as the brand expanded into new cities, retailers couldn’t keep it stocked. “The thing just took off like nothing had ever taken off before,” Ed Artzt, a sales and marketing executive, recalls.

After two years, Charmin was the bestselling toilet paper in every region it competed in. R&D created a better product, which led to a great marketing plan, which led to big sales increases in retail stores. The process was long, difficult, and cost millions of dollars, but it was worth it. “The acquisition of Charmin,” David Dreyer wrote in the company’s history book, “became the basis of several billion-dollar brands and one of the company’s leading growth producers.”

Where does research and development go at Kraft Heinz?

It’s staggering to contrast Kraft Heinz’s integration approach to P&G and Charmin. It’s even more staggering when you look at one specific business process: research and development.

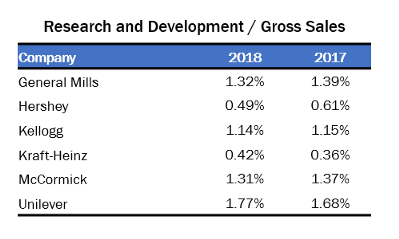

As the Charmin example showed, research and development is at the center of a branded CPG firm. Consumer preferences change, and it’s up to manufacturers to develop new products that consumers want. In the food industry, consumers are transitioning away from fatty packaged food and toward healthy and fresh alternatives. According to Businessweek, from 2014 to 2017, the top 10 packaged food companies lost over $16 billion in revenue. No one is entirely sure what this means for legacy manufacturers like Kraft Heinz, but during this transition, Kraft Heinz slashed R&D budgets. In the three years before the merger, Kraft spent about 0.8% of revenue on research and development, already somewhat low for CPG firms. The table below shows how it only got worse once Kraft Heinz merged:

Making matters worse, when Kraft Heinz actually made an investment in R&D, it chose poorly. In an attempt to compete with healthier products, the company invested $10 million to reformulate hot dogs — at about the same time the World Health Organization labeled the food as a contributor to the risk of colon cancer.

A different approach

To be clear, 3G management took on an almost impossibly tall order with a $72 billion acquisition of Kraft and Heinz. First, history is littered with failed mergers and acquisitions. Billion-dollar transactions rarely work out unless you’re the bank booking the M&A fee. Second, both companies were established CPG firms. Unlike P&G and Charmin, there was no real value in bringing Kraft’s products into Heinz’s existing business processes because Kraft’s processes were probably just as efficient. It’s not like Heinz hadn’t mastered producing and selling ketchup for the last 100 years.

P&G acquired a regional toilet paper brand and spent enormous sums of money developing a better toilet paper. It supported the product with world-class marketing and sales. Charmin dominated the industry for the last 60 years. 3G could have mimicked this approach. It could have acquired Kraft and then targeted smaller, regional brands that produce healthy options that would benefit from the company’s established scale and business processes.

Instead, it pursued a strategy centered on two tactics: optimizing operations through cost cutting and generating leverage against retailers by creating the fourth largest food company in America. The former slowly and then suddenly deteriorated the value of the company’s legacy brands. The latter hasn’t materialized. In the case of the reformulated hotdogs, Kraft Heinz struggled to sell them to Walmart, which constitutes about 20% of the company’s yearly sales. The grocery goliath preferred Ballpark Franks and its own private label, leaving the new company in the same position facing many legacy manufacturers.

The result is a company with legacy brands hemorrhaging sales to healthy upstarts and an organization ill-prepared for the new reality. “[Innovation] is a big driver for growth for the future, has to be especially in the food industry,” Patricio, Kraft Heinz’s CEO, told investors in 2019. “But we have to do bigger innovation. We have to do fewer innovation[s]. We have to do bolder innovation.”

But because Kraft Heinz is spending so little on R&D, these innovations have yet to yield meaningful results. That’s because without properly funded R&D, Kraft Heinz is stuck either treading the same path while ignoring consumer trends or failing to innovate significantly and quickly enough. Last year, in fact, one of the biggest new product launches from Kraft Heinz was salad frosting.

Yes, salad frosting.

Something tells me that salad frosting isn’t the healthy and fresh choice consumers have been looking for.

Note: This article was originally featured over at Medium’s Marker Magazine.

Photo by Pedro Ribeiro on Unsplash