Last week Nestlé, the world’s largest packaged food company, posted solid earnings as consumers continued to pivot towards grocery stores amid the pandemic. Overall, the company saw organic growth rise by 3.6%, putting it in between rivals Kraft Heinz (6.3%) and Unilever (1.9%). Much of this growth is due to smart acquisitions and divestitures, recently headlined by its $4.3 billion sale of its North American bottled water business to private equity firm One Rock Capital Partners. What I find interesting is what these acquisitions mean about the Nestlé e-commerce strategy and how it might just be the future of the CPG industry.

The Nestlé M&A approach

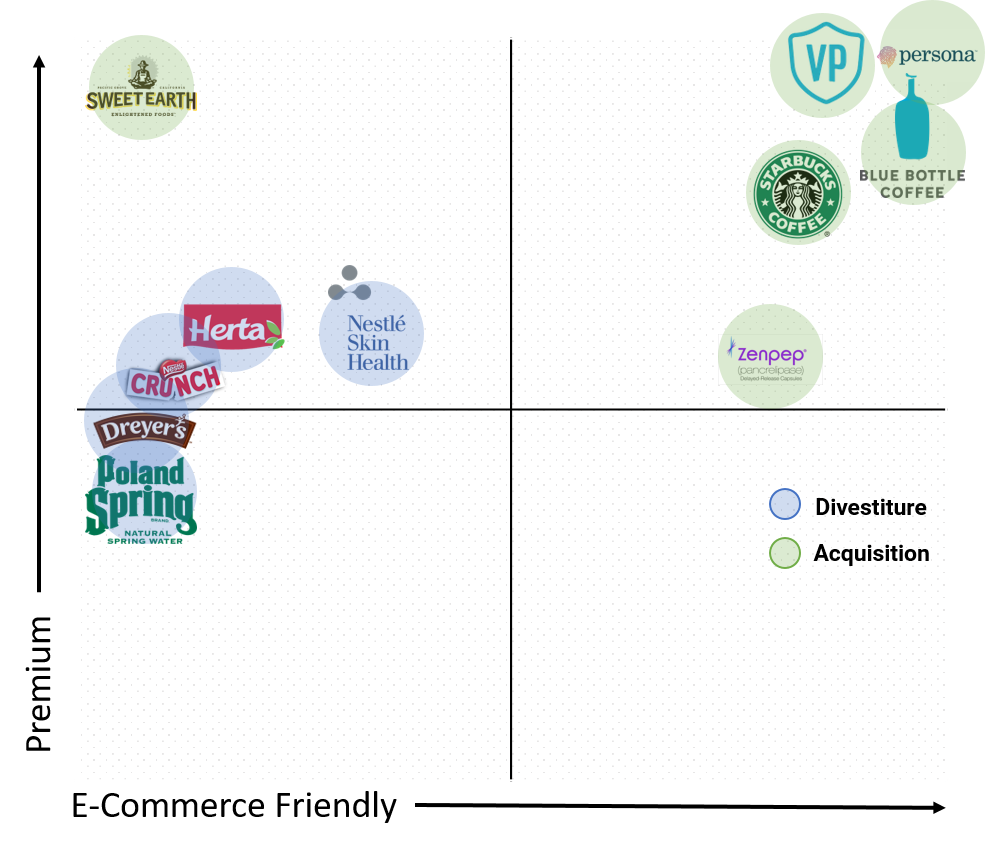

In 2017 Nestlé missed earnings estimates and found itself struggling to compete in the U.S. market. Since then, the company has completely revamped its offerings. It sold off non-core assets like Gerber Life insurance for $1.5 billion. Its CPG catalog divested from bottled water, Nestlé skin health, U.S. candy business, U.S. ice cream, and packaged meats. The company entered 75 separate transactions—turning over about 18% of the company’s sales. As the below graphic shows, the major strategy can be summed up as: Get Premium and Get E-commerce.

I went ahead and categorized the company’s recent major transactions across two measures: Premium and E-Commerce Friendly.

You’ll see the Y-axis is labeled Premium. That effectively means, can Nestlé charge a premium price for the product? The answer for almost all the divestitures is “no”. Poland Spring is a budget brand; Herta will always be a convenience option to freshly sliced meats.

The X-axis, E-commerce Friendly, is a bit more nebulous. Essentially, does the product and brand lend themselves to e-commerce? When thinking about e-commerce, ask yourself:

- Can it be easily stored in a non-climate-controlled warehouse?

- Does it lend itself to bulk pack sizes?

- Can buying be personalized via a website?

The answer for almost all the divestitures is no. Dreyer’s is not only a mid-tier ice cream brand—unable to compete against high-end gelato and healthy options like Halo Top—but it’s also a category dependent on in-store distribution. Ice cream requires refrigeration, which does not lend itself to easy e-commerce sales. U.S. candy is almost entirely single-serve, impulse-driven, and often involves refrigeration during transit (prevent melting), making it a tougher sell online.

Meanwhile, nearly all the acquisitions are premium products and/or native to e-commerce. Like Dreyer’s, Sweet Earth is dependent on refrigeration. Unlike Dreyer’s, it offers premium vegetarian offerings priced a dollar or two higher than the competition. Persona offers personalized vitamins through a digitally native sales experience. Starbucks was the first premium coffee brand in America, and Blue Bottle Coffee takes it to another level. Both have product offerings that are easily shipped and sold over the internet.

I should point out that my graph doesn’t include Freshly and Mindful Chef, two digitally native meal prep companies Nestlé acquired.

It also says nothing about PetCare, a category ripe for e-commerce that Nestlé is positioned to conquer.

The Nestlé e-commerce strategy

Mark Schnieider, CEO of Nestlé, talked about its evolution in e-commerce—with an eye towards pet care.

I think the best area to exemplify that is PetCare where, clearly, we’ve been for years patiently building up what I call a PetCare ecosystem when it comes to the total advice around pet ownership, and nutrition, of course, being a big part of that. Then increasingly bundling in e-commerce opportunities including bespoke, such as Tails.com and Just Right in the U.S. So I think this is a major opportunity. PetCare being one example.

I think you’re seeing similar opportunities in other major categories, but PetCare does stand out. So I agree with you that this is a key area of focus for us going forward.

Most CPG companies talk about using technology to build ecosystems or platforms. Honestly, a lot of it is nonsense marketing speak, but Nestlé is actually doing it in pet food. Many manufacturers are selling the same exact products (they may change the pack size) but through Amazon or Walmart.com. When you go to Just Right, you fill out a quick survey about your dog, and moments later, you have a completely custom food blend—priced at a premium, of course—ready to be delivered to your door. It’s the type of product that can’t be sold in traditional retail but perfect for online.

This begs the question, “How much of this infrastructure should Nestlé build and how much should it create through partnership?”

In terms then of acquisitions, I mean, when it comes to just digital enablers, I feel more often, this is about partnerships and it’s about licensing. When it comes to business models, yes, and take as an example our investment in Freshly, where clearly, you have a business model and there’s a strong digital component to it. Or take our acquisition of majority stake several years ago in Tails.com, where you have bespoke pet food, and clearly digital is the way to order pet food and to get into those subscriptions. So,this is where I would see the sweet spot. So,we have a digital model with the business model combined. Just digital tools alone, frankly, I’m not sure we should be the only owner of that. I think there, it’s better to license in or to partner.

Translated — if the core business model is reliant on technology, it could make sense to own–if not, partner.

Later, he described the results.

Let me highlight on top that for a category like pet food that indexes very well in e-commerce; there is frequency of consumption and shopping, it’s bulky, so that’s prone to subscription models. There we grew, in the U.S. last year, 65%, and it is close now to 20% of sales.

Potentially 20% of sales!

It sounds like a winner. It sounds like the future of CPG.

Photo by inma · santiago on Unsplash