Earlier this month, in a move that harks of fascism, President Donald Trump decreed that TikTok, the Chinese based social application popular with teens, must sell off its U.S. operations. TikTok, which allows users to create and share short videos, boasts over 100 million monthly users and is largely viewed as Facebook’s biggest competitor. Initially, the usual suspects emerged as possible purchasers. Now, it looks as if Walmart may acquire TikTok (with an assist from Microsoft).

The retail giant’s entry into the global sweepstakes was a surprise and comes as the parties grapple with a valuation for TikTok, which is facing a potential ban in the U.S. from the Trump administration over national-security concerns.

TikTok’s Beijing-based owner ByteDance Ltd. is asking about $30 billion for the U.S. operations, but bidders thus far haven’t been willing to meet that price, according to people familiar with the negotiations. By comparison, Twitter Inc. in recent weeks informally floated a bid closer to $10 billion as part of a range of pricing and scenarios, said some of the people.

Microsoft’s joint bid with Walmart is considered the front-runner, according to people familiar with the matter, while a second consortium including Oracle Corp. remains in the running.

Founded in 1962 on the mantra of “Always Low Prices,” the company spread like wildfire when fair trade laws left America. Manufacturers were no longer able to control the retail pricing of their products, and Walmart took advantage. It used its size to demand steep discounts and passed the savings to consumers. This newfound pricing power was supported by cutting edge real estate strategies, operations, and logistics—leading to it becoming the most dominant retailer of a generation.

Basically, Walmart buys goods from manufacturers, distributes them to physical locations, and then sells them at a mark-up to consumers. It’s a basic framework, as old as civilization, that gets complicated when you get into specifics. Although TikTok is a new technology, its’ business model is old–it sells advertisements to its userbase of over 100 million monthly users. How do these two business models work together?

While Walmart has provided few details of its rationale, in confirming its intentions it highlighted TikTok’s potential to expand two particular parts of the US retailer’s business: advertising and its online third-party marketplace. Ecommerce industry experts believe the success of both could be critical to enabling Walmart to compete successfully online against the might of Amazon…The appeal is in the extraordinary digital reach of TikTok, which has more than 100m active US monthly users. They are predominantly young, tech savvy and likely to shop online. An acquisition would give Walmart the chance to “get more eyeballs”, said Charlie O’Shea, retail analyst at Moody’s.

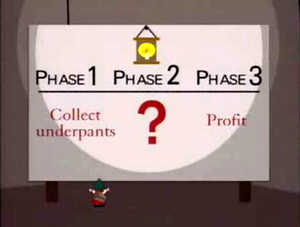

So, according to a lot of smart people, the strategic rationale is to spend billions of dollars on a network that makes user acquisition easier. This sounds a whole lot like underpants gnomes to me.

Why I’m skeptical of Walmart’s potential acquisition of TikTok

Walmart is a revolutionary brick-and-mortar retailer that created an empire by using scale and technology to take advantage of changing US commerce laws. It has done an admirable job integrating technology into its operations—becoming a true omnichannel retailer. It’s core strategic assets are a) buying power and b) footprint of over 5,000 physical locations. There’s a lot of money to be made in this space.

It’s also relatively boring.

There’s not a lot of headlines for companies that sell low-cost consumer basics. Walmart has spent the last decade throwing away billions of dollars to make itself relevant. First with Jet.com, where it spent $3 billion to buy an Amazon clone—despite having just 20 fulfillment centers to Amazon’s 120. It quietly shut down the website after losing $1 billion a year on about $20 billion in revenue.

Walmart has also spent almost half a billion dollars on unprofitable, but hip brand acquisitions.

Jason Del Rey explained:

Lore has overseen the acquisitions of the menswear brand Bonobos for $310 million, the vintage-style clothing brand ModCloth for less than $50 million, and, most recently, the women’s plus-sized fashion brand Eloquii for $100 million. Part of the thinking was that those deals would give Walmart and its online stores exclusive merchandise that shoppers can’t find on Amazon, which could help the Middle America retail giant appeal to a new generation of consumers who typically wouldn’t shop at Walmart.

But all three businesses are still unprofitable, sources say. And in recent months, Walmart has discussed the potential sale of both Bonobos and ModCloth to separate outside buyers, according to multiple sources familiar with the discussions.

Now it’s looking to spend up-to $30 billion on an app, with a business model it has no core competencies in.

Early in her newest book, Break ‘Em Up,Zephyr Teachout retells the story of an Amazon air hockey seller. The seller, whose air hockey table was one of the top-3 search results until Amazon introduced sponsored ads. Coincidently, despite years of sales and popular reviews, the product dropped off the search charts with their arrival—even the free organic results. Potential buyers in the America’s largest online market could no longer find the product. In a desperate act to regain volume, the seller decided to spend $5,000-$10,000 a month on Amazon sponsored advertisements. As if magic, a product that mysteriously dropped off Amazon’s organic search results, found its way back to the top after it bought thousands of dollars of advertisements.

Zephyr Teachout explains:

The resulting system is the opposite of a competitive market — it’s a kickback regime. Amazon sets up an allegedly neutral system , and then charges fees to game that system, calling those fees “ advertisements. ” Sellers compete over how much they can pay Amazon to get access to consumers.

This example speaks to the heart of Break ‘Em Up. Teachout argues that large private monopolies are forms of tyranny that destroy our economy and democracy. The small air hockey seller is not free to conduct business if they’re forced to purchase thousands of dollars of advertisements from the only online market that matters. According to Teachout, the only way to combat the tyranny is to target the heart of the issue: the business model itself.

About Zephyr Teachout

In my opinion, Zephyr Teachout is one of the most important figures within the modern progressive movement. She’s a lawyer, law professor, author, and multiple time candidate for public office. Unlike a lot of her contemporaries, her arguments and solutions aren’t driven solely from a moral standpoint. Instead, she provides a moral vision with a fierce defense of competitive markets and cost-savings—something every business minded person should hold dear to their heart. Take the popular progressive position of Medicare (universal health care). Zephyr supports it, but wants to move past the discussion of universal coverage and into the structural issues driving health care cost: private monopolies.

Here’s the rub: driving down prices is much harder when the government is negotiating with a powerful monopoly than when it is negotiating in a competitive market. Healthcare expert Phillip Longman has written several persuasive articles about consolidation in the drug market, and the healthcare industry more generally, and the risk that this consolidation poses to nationalizing plans. If a single payer plan was enacted without additionally addressing the monopoly problem, he argues, government could end up effectively subsidizing big pharma, and big hospitals, and keep paying enormously high prices. Those costs would shift back to the public—in the form of taxes.

Single payer care is necessary for humane reasons, and for the extraordinary reduction in administrative costs. But why not demand both single payer and breaking up drug monopolies?

Basically, Zephyr Teachout has the courage and the moral conviction of Ralph Nader, but the vision to see the structural issues driving our society.

Private Taxes

Break ‘Em Up is structured into two parts. The first argues that private monopolies have destroyed a lot of what we consider society. The second is what to do about it. One of my favorite things about this book is how she frames business taxes. The earlier $5,000 to $10,000 ‘advertising’ fee that the small business pays every month isn’t advertising. It’s a private tax, imposed by Amazon in order to access the market. Unlike public taxes, which go to fund roads and schools, this goes straight into the pocket of Jeff Bezos—who is current worth around $200 billion.

She walks us through a variety of industries and the monopolies that impose private destructive taxes on each: Tyson and Farming, Facebook and Journalism, Amazon and Retail. The stats are particularly damning in farming. In 1985 farmers were paid about 40 cents for every dollar Americans spent on food. Today, that number is down to 15 cents. The money has shifted from small producers, to large manufacturers and retailers.

The first part of the book is well written, but unless you’re new to the anti-monopoly thought, it isn’t particularly groundbreaking. In my opinion, The Curse of Bigness by Tim Wu (who she ran for governor with) and Matt Stoller’s Goliath do a little bit better job explaining the evolution, history, and impact of the rise of private monopolies. Where Break ‘Em Up really shines is in the second part—what to do about it.

Break ‘Em Up!

If you regularly read this blog, you know that I write and work at the intersection of politics, technology and consumer products. I’m generally partial to the plight of consumer products companies—this isn’t to say they’re blameless—but most are effectively powerless against large retailers. The reason for this is quite simple–we quit enforcing free trade laws.

For most CPG companies, two retailers (Walmart and Kroger) constitute 30-35% of sales. If one of them says an item’s price needs to be lowered—it’s going to get lowered—and the manufacturer is going to take the margin bite. They simply can’t risk getting their item take out of the store. The only way they’re able to negotiate is if they have a large portfolio—either raising prices elsewhere or making it up in overall volume. Either way, the underlying structure pushes companies towards consolidation—like the mega-merger of Kraft-Heinz.Break ‘Em Up is one of the first books that I’ve read that gives concrete framework to stop the structure from happening.

1. Open, competitive markets, working together with publicly provided services and neutral infrastructure, are necessary for economic liberty. There is no one-size-fits-all answer to every industry, but unregulated private monopoly poses a unique threat. Private corporations with too much power raise prices for consumers, depress wages for workers, choke off democracy, and regulate all of us.

2. To preserve rough economic and political equality, we should make it easier to organize people and harder to organize capital. It should be as easy to unionize, or to create a cooperative, as it is hard to merge goliaths.

3. It’s better to err on the side of decentralized private power. Democratic governance is messy and will lead to mistakes, but corporate government will lead to tyranny.

To me, some of her most powerful writing is when analyzes Michael Sandel’s What Money Can’t Buy, a book that argues the typical progressive line on capitalism—that it’s bad and needs to change for moral reasons. Her response is phenomenal and I think shows a viable path forward to popularizing progressive policies across the ideological spectrum.

Sandel’s approach is dangerous because it closes down an arena of moral action and redirects activism away from breaking up big corporations. It makes us ignore market – structure problems. If we treat markets as a kind of necessary infectious disease that one must cordon off, instead of institutions that can be wonderful or corrupt depending on how they are structured, we stop trying to fix them. And while a few people think the state should make shoes and grow carrots, most people — including myself — imagine most of economic life happening through private exchange.

Zephyr’s solution isn’t to regulate out markets. The solution is to regulate markets in a way that works for people. She then provides a framework that isn’t just theory, but practical and proven.

All in all, Break ‘Em Up is a nice addition to the modern anti-trust movement by one of its most important practitioners.

Consumer packed goods is a tough business. Almost every single consumer product category features entrenched players who have brands backed by literally hundreds of millions of dollars. Not only do companies need to create products that consumers want, but they must fend off competitors who are using their hundred-million-dollar war chests to entice customers (retailers) to give preference to their product through discounts and other sales incentives.

No where is this harder then with commodities—like flour. Realistically, for the average home baker, there isn’t much difference between flours. Today, the retail flour industry is dominated by General Mills, whose Gold Medal brand contributes to the conglomerate’s $17 billion in revenue every year. One thing about Gold Medal is that its attributes are a perfect distillation for the overall consumer goods industry: It’s a reasonable quality product that General Mills can produce quickly across the country.

As flour is exposed to oxygen it naturally bleaches—making it easier to bake. Gold Medal, and most other store-brands, are artificially bleached. A bleaching agent like chlorine gas is used to speed the whole process up. This allows millers to turn production over in a fraction of the time—increasing production efficiency and profit.

Milling flour, at the risk of stating the obvious, is not a new business. The basic technologies of milling were invented sometime in the third century B.C. For the early centuries of American history, local mills, powered by water, were economic anchors for small towns across the American colonies and, later, the nation. Their physical legacy is the hundreds of old stone gristmills scattered around the country, some converted to other uses, others quietly decaying.

The abandoned mills are testament to the fact that during the 20th century, the business of flour was almost entirely overtaken by large, centralized operations. For many decades now, flour has been ruled by the central dogma of American business strategy: maximization of size and scale, ideally to the point of monopoly. Most of America’s large national corporations are built on this model.

The end result is a commodity product across American homes. Something weird happened during the coronavirus era. People flocked to branded flour. The biggest beneficiary was King Arthur.

King Arthur: A Premium Flour

King Arthur is Vermont based employee-owned flour company. In 1984 it logged about $4 million in sales; in 2019 it shipped $150 million worth of flour to retailers. On average King Arthur is priced above Gold Medal.

At the heart of the company’s approach is wheat sourcing. It pays extra for wheat that’s especially high in protein—the critical element for giving baked goods a nice, proud rise. The 45 mills that make King Arthur flour, including Farmer Direct, meticulously blend each variety to get the protein ratio consistent within two-tenths of a percent. King Arthur all-purpose flour clocks in at a sturdy 11.7%, a figure that’s printed right on the front of the bag. The resulting breads are light and airy; the cookies don’t spread too much on the tray…The flour is never bleached, lending it a creamy, natural appearance that sets it apart from its bright-white competitors.

By comparison, Gold Medal is bleached flour and has a protein ratio is 10.5%. That means King Arthur sells a premium product at a premium price.

But how does it differentiate itself? After all, very few people probably know that more protein leads to better baking.

How King Arthur turned a commodity into a branded product

Early on, King Arthur management viewed it as much more than a flour company. It wasn’t selling flour, it was selling the joy and love of baking.

Bloomberg continues (emphasis mine):

As the business’s fortunes have grown, the Sands family’s commitment to baking education has continued to flourish. King Arthur has published three cookbooks, and it offers more than 1,000 recipes on its website—gateways to a thriving e-commerce operation where you can pick up whole-wheat pastry flour, Indonesian cinnamon, or a baguette pan. For 20 years the company has also run a hotline staffed by experienced bakers, who field thousands of calls each month from customers fretting about proofing temperatures or recipe substitutions. An equally knowledgeable team tackles questions and comments that come in through social media.

I think the bolded part bears repeating. For two decades the company has ran a baking hotline where people can call and ask questions about baking! Not only did it sell a premium product, but it built a support infrastructure to support a community.

From commodity to branded – a recipe.

Success in consumer products is about execution. With that in mind, I think the following framework can help in understanding what to execute.

Where is the commodified gap?

As categories grow and scale, gaps inevitably develop across brands. With razors it became price, with Gillette and opening itself up to cheap competitors like Dollar Shave Club. With flour it was quality—allowing a premium brand like King Arthur emerge.

What larger movement does your commodity address?

A premium flour allows better baking. Patagonia offers sustainably designed outdoor gear.

How can you support the larger movement?

Premium products need premium support. King Arthur built out a robust website, an in-person hotline, and leveraged social media to offer more support. King Arthur flour isn’t just a product you buy from the grocery store. It’s a network that amateur bakers can leverage.

COVID-19 has had a tremendous business impact across the CPG landscape. Seemingly overnight the competitive landscape shifted. Faced with concerns about quality and safety, consumers returned to long-established brands. Some brands even exploded after restaurant demand evaporated overnight. This left major companies with an interesting operational decision. For years, CPG companies expanded and structured themselves to deliver unlimited choice for consumers—trying desperately to capture the ever-changing preferences. In the midst of unprecedented demand and uncertainty, retail partners are overwhelmed, preferring to stock safe SKUs—not experiment.

Internet or direct-to-consumers is always trotted out as the silver bullet for struggling companies in the coronavirus era. It’s basically the business version of telling unemployed people to ‘learn to code.’ It’s an unserious idea for a structural issue.

Food service involves selling and delivering one fifty-pound bag of coffee to one customer, retail involves selling fifty one pound bags to fifty customers. They have entirely different cost structures and operations.

But what about the largest CPG companies? They have the resources to pivot on a dime. I combed the largest CPG firm’s public statements to understand the business impact of COVID-19.

“The other one, while still early days, that we saw, is an interest in larger pack sizes. That’s also not surprising when people spend more time at home, rather than consuming lots of small packs, they rather buy fewer large packs. As I said, our strategic business units are now working overtime to really understand, not only in light of the health care crisis, but also the economic pressure, what that means for each of our categories. To me,that is super interesting work because clearly this is not going to be a quick recovery. This is going to be several-quarter, if not several-year kind of process, where it is safe to expect some changed category dynamics. We want to recognize those early and adapt to those early and be a leader when it comes to those trends.”

“Increased demand has focused retailers on the core SKUs that drives the business. There is potential for this to result in a cutting of the long tail of inefficient SKUs and brands in our categories. We’re discovering daily lower cost ways of working with fewer resources. Today’s necessity birthing the productivity intentions of tomorrow. New digital tools are being brought to the forefront, providing another productivity rocket booster on the factory floor and in the office environment.”

“We’ve made some choices in our supply chain to — we’ve reduced some of the tail of our portfolio. We’ve discussed that with our partners, retail partners. And we both agreed that it’s probably the best thing to do, to eliminate the less — let’s say, the smaller SKUs in the portfolio to maximize the best-selling SKUs and be in stock. As I said earlier, our DSD system, I think, is a fundamental advantage in the way we’re able to service our customers. And I think they appreciate that, that we’ve made the effort, adjusting delivery schedules and increasing delivery schedules to make sure that we keep our brands in stock and we help, obviously, our partners.”

“The first test of this theory came early in the pandemic when demand for Unilever’s more essential products, such as cleaning supplies, shot up 600% in some cases. To deliver, the company converted production lines and reduced the number of total SKUs it produced by 65%.”

For as long as there has been business, there have been theories that attempt to explain the outcomes of the market. Some, like creative destruction and the innovator’s dilemma, are far-reaching and offer a universal framework to analyze the political economy. Others, like the wheel of retailing, concentrate on individual industries—and attempt to explain specific niches.

What is the Wheel of Retailing?

The wheel of retailing is fairly straight forward. Here is how Professors Peter Scott and James Walker defined it at Business History:

New retail modes frequently emerge at the bottom end of the price and service spectrum, using low-cost, low margin, `no frills’ formats to undercut incumbent competitors. However, once well-established, such retailers typically up-grade services and facilities, raising costs and prices and leaving themselves vulnerable to a new wave of low-cost entrants.

Walmart is proof of the theory. Founded in 1962 on the mantra of “Always Low Prices,” the company spread like wildfire when fair trade laws left America. Manufacturers were no longer able to control the retail pricing of their products, and Walmart took advantage. It used its size to demand steep discounts and passed the savings to consumers. This newfound pricing power was supported by cutting edge real estate strategies, operations, and logistics—leading to it becoming the most dominant retailer of a generation.

In the late 2000s, Walmart’s strategy switched. Walmart entered grocery and created “superstores.” Low prices were still important to the company’s strategy, but so was the overall shopping experience. In 2019, the company announced plans to invest $11 billion updating over 500 storefronts, which includes redesigning automotive and cosmetics. They aren’t selling the cheapest or the best—but somewhere in between. The company’s mantra is now “Save Money. Live Better.”

As Walmart moved up the wheel of retailing, a new discounter followed in its wake—Dollar General. Like Walmart in the 1960s, Dollar General offers low prices. The low prices are profitable because of their operations. Consider assortment. A typical Walmart superstore carries about 120,000 items. That’s 10x as many items as a Dollar General. From a staffing perspective, Walmart averages one associate per 475 square feet of sales space. Dollar General averages one to about 777 square feet. Dollar General offers less selection, with less customer service, but lower prices.

Will Dollar General ever move up the wheel of retailing?

I don’t think so, but before I get into why it’s important to understand why discounters become successful, and why the transition up the wheel of retailing is often difficult.

Strategy differ across the wheel of retailing

In their 2017 history of five-and-dime stores, Peter Scott and James Walker argue that earlier discounters (like Woolworth) declined because the operations that allowed them to discount profitability didn’t translate when the stores attempt to move up the wheel of retailing.

One of those operations is their personnel strategy.

Today, both Dollar General and Walmart rely on low-wage workers to serve as sales associates. Dollar General pays around $8.50 an hour; Walmart is around $12. Here’s Woolworth’s CEO describing the same sentiment in 1892:

We must have cheap help or we cannot sell cheap goods. When a sales clerk gets so good she can get better wages elsewhere, let her go –for it does not require skilled and experienced salesladies to sell our goods.

This business strategy may work when the store is selling commodity goods like toilet paper and sponges. It falls flat when selling specialized products like clothing and automotive parts. Scott and Walker quote another discounter in 1932, who recently transitioned up the wheel of retailing, highlighting the importance of suggestive selling and bemoaning low-paid worker’s ability to execute it.

You should possess this information in order to properly train your salesgirls in the art of increasing each sale. Of equal importance is a thorough understanding of the best methods for presenting your merchandise to the customer in such a manner that interest is aroused and the salesgirls’ service appreciated…Verbal suggestions must be followed up by intelligent comment… Few salesgirls are instinctively able to do this.

Walmart has been able to manage this transition. History isn’t so kind to others.

Discount strategies struggle when selling higher-value goods

Discount retailers ran into department stores when they attempted to move into high margin products. Retailers like Macy’s, and JP Penny, carried high-end products, carefully purchased by specialized buyers, and sold by well-paid salespeople.

Function

Discounter

Department Store

Advertising

No-advertising, rely on word-of-mouth generated by low prices.

Incremental volume driven by frequent sales and newspaper promotions.

Assortment

Standardized products via centralized and direct purchasing at HQ.

Individual department managers are category specialists who have wide discretion in what they purchase and carry.

Personnel

Low wage hourly sales associates.

Associates are relatively well paid by sales commission.

Discounters never really had a chance. Discounters were designed to bulk purchase a variety of commoditized goods and sell them cheaply—the opposite of higher-end retail.

So this begs the question, why did previous discounters move up the wheel of retailing?

Market saturation moves discounters up the wheel of retailing

Scott and Walker conclude that discounters moved up the wheel of retailing because they had nowhere else to go for growth. Given that the business model relied on no advertising and standardized commodity products, the only way in a new market was to cut prices—a disaster in waiting. They couldn’t enter new territories, because all the territories were taken. According to their analysis, Woolworth, a dominant player, faced competition in just 22 percent of their 238 locations.

Our model views shifts from low to higher value merchandise as being driven by retail format saturation in the low price niche. No frills retail formats compete primarily on price. However, for very low price merchandise substantial gross margins are necessary to cover high handling cost to price ratios. Price wars between rival stores adopting the same format are thus potentially ruinous. The alternative is to move into higher value lines, but this necessarily involves adding more services –to meet the minimum expectations of consumers and provide the information and advice they require. (Emphasis mine)

Dollar General faces different social dynamics

Scott and Walker were writing about an era of unbridled economic growth. As more Americans became middle class, more and more Americans wanted to purchase higher quality goods.

The opposite is now true.

As long as the economy continues to drive inequality, modern dollar stores will continue to excel, giving no incentive to move up the wheel of retailing.

From a New Yorker article detailing how Dollar General became a target for crime:

The chains’ executives are candid about what is driving their growth: widening income inequality and the decline of many city neighborhoods and entire swaths of the country. Todd Vasos, the CEO of Dollar General, told The Wall Street Journal in 2017, “The economy is continuing to create more of our core customer.”

Given what we’ve seen in the last ten years, it seems highly unlikely that Dollar General will ever need to move up the wheel of retailing.

Today, retail pricing, the price you see in stores, is determined by Retailers—not Manufacturers. For example, if you go to Kroger for a 12-pack of Sprite, the price you pay isn’t set by Coca-Cola—it’s set by Kroger.

This wasn’t always the case.

In the past, it was legal for manufacturers to determine retail pricing. Often times, manufacturers offered a lowest acceptable retail price—and it was small retailers who pushed for that ability. Here’s the quick story about how that happened.

Early retailing is a family affair

Edna Gleason, was a self-educated but state-certified pharmacist who owned three drugstores across California. In the early 1900s, pharmacists were predominately small businesses. A family would own a store, where they would mix drugs and sell a variety of home care goods. Edna and other local pharmacist bought most of her goods from a wholesaler, who bought the goods from the manufacturer. Both links in the retail value chain have cost—which meant a mark-up. The result was a modest selection, with two price mark-ups. It was a simple business considered by most to be key to self-sufficiency.

Then came Chain Stores and Pineboards—large, wall capitalized corporate structures that entered new markets and undercut locally owned small businesses.

Chain stores gave retail pricing advantages to stores with big footprints

They’re everywhere today, but chain stores are a relatively new development. Prior to the early 1900s, national chains stores weren’t widespread.

East Coast chain stores, like the Great Atlantic & Pacific Tea Co. (A&P), and department stores, like R. H. Macy’s, pioneered a business model that captured profits by combining high-volume sales with lower profit margins. Most of these retailers purchased goods from a variety of manufacturers. High-throughput manufacturing revolutionized consumer products from processed foods (e.g., Campbell’s Soup) to cigarettes (e.g., American Tobacco).Taking advantage of manufacturers’ economies of scale, these new retailers up-rooted the existing distribution system, tilting economic power toward large-scale retailers and away from the networks of regional manufacturers, wholesalers, and local retailers. Many manufacturers also complained that they had lost control of their brands.

Essentially:

Chain stores placed large orders—which meant they were able to negotiate volume discounts

Chain stores placed orders directly with manufacturers—bypassing traditional wholesalers

Chain stores then passed the price savings on to consumers. The result was a fundamental switch in power from regional manufacturers (who were used to negotiating with thousands of small stores) and small retailers (who held local monopolies in distribution) to chain stores and consumers.

Pineboards were chain stores on steroids

Chain stores often had large, clean, well-lit operations that catered to a growing middle class. Pineboards were something completely different. “The distinctive feature of the pineboard,” Laura Philips Sawyer wrote, “was its ability to offer brand-name products at prices below the manufacturers’ retail network, undercutting even the chain stores.”

This discount model required pineboards to adopt a different strategy than chain stores and locally owned operations. The strategy was strikingly similar to today’s dollar chains.

Pineboards

Modern dollar stores

Lowered fixed costs by renting commercial space on a temporary basis to test competitive waters.

Keep fixed costs low by building small stores in low income rural and urban areas

Reduced variable cost by employing unskilled, low-wage laborers rather than trained pharmacists.

Stores are staffed by 1-2 people low-wage laborers. Customer service is not a priority

Required cash payments and did not offer delivery services.

Mostly deal in cash; did not accept credit cards until recently (Dollar General started in 2005)

A pharmacy by association. No prescription drugs, but sold more basic consumer goods.

Very few fresh food items, but enough to be considered a grocery store and “essential”

The rise of pineboards and chain stores threatened the survival of Edna Gleason’s pharmacy. It also threatened all of small-town America. Local retailers were the life blood of any small town. Unlike chain stores, they bought from local manufacturers, and the money stayed within the community. In contrast, chain stores are arguably extractive—funneling profits to shareholders thousands of miles away. This strategy resulted in cheaper prices and how was she to compete with chain retailers that offered cheaper products?

She couldn’t.

So she organized until she could.

Edna Gleason attempted to standardize retail pricing

In February 1929, about seven months before the Great Depression officially kicked off, Gleason led a movement to restructure the California pharmacy industry. First she consolidated the statewide lobbying groups into one large organization, the California Pharmaceutical Association. Then she set out to publish a statewide pharmaceutical price list.

Philips Sawyer summarized the thinking:

Advocates of fair trade envisioned a strong state association that would publicize standardized price lists and monitor member compliance. The publication of monthly price lists would, they argued, allow businesspeople and regulators alike to monitor price changes.

The initial price lists were informally enforced; compliant retailers would blacklist and shame non-compliant ones. This behavior is of course anti-competitive, illegal even. Until a new legal theory emerged. It held that when competing against chain and pineboard retailers, independents were no different than employees bargaining against large employers. They were free to combine their buying, marketing and sales power to combat larger competitors.

The result was The California Fair Trade Act of 1931. It exempted the above agreements from antitrust prosecution and gave the state police powers to enforce the free trade agreements. Essentially, if a group of independent retailers agreed that a manufacturers retail price was fair, the state police would enforce the agreement. Phillips Sawyer concludes, “This public-private approach to managing price competition came to exemplify Depression-era regulation.”

Fair Trade Goes national and then disappears

Given the current state of American anti-trust, it’s hard to imagine now, but retail pricing laws, which increased consumer prices, were overwhelmingly popular. Underpinning the legislation was an ideological sentiment: Local control and ownership of commerce were a defense against communism and fascism. That freedom to own and manage production was more important than low prices.

In the late 1930s, Congress nationalized the California Fair Trade laws, culminating with the Robinson-Patman Act and Miller-Tydings Act. The first banned selling products at a loss to boost volume and secret discounts. The second, made fair trade contracts enforceable across state lines.

The general Fair Trade framework, spearheaded by Edna Gleason, lasted until the 1975.

By 1975 prices in America were increasing by around 12 percent every year. The causes of this are vast and debated, but at the time, one of the easy culprits were fair trade laws…The logic was that if Congress got rid of fair-trade laws, prices would drop.

With the laws gone, national chain stores were free to use their power and footprint in retail pricing negotiations. Economic power shifted from regional manufacturers and local retailers to national chain stores.

In 1975, Walmart was a regional retailer with around 100 stores.

Influencer marketing is a big business. Business Insider estimates that by 2022, brands will spend up to $15 billion on influencers pitching their products. In most respects, the United States is lagging behind China in its reach and impact.

Bloomberg recently published an article on Huang Wei, China’s dominant live online shopping influencer. She’s expanded from blogs and Instagram posts, to livestreaming.

In April, Huang—known professionally as Viya—sold a rocket launch for around 40 million yuan ($5.6 million). The live, online shopping extravaganza the 34-year-old hosts most nights for her fans across China is part variety show, part infomercial, part group chat. Last month, she hit a record-high audience of more than 37 million—more than the “Game of Thrones” finale, the Oscars or “Sunday Night Football.”

Each night, Viya’s audience places orders worth millions of dollars—typically for cosmetics, appliances, prepared foods or clothing, but she’s also moved houses and cars. On Singles Day, China’s biggest shopping event of the year, she did more than 3 billion yuan in sales. The spread of coronavirus, which put most Chinese people under stay-at-home orders, doubled her viewership.

The numbers here are staggering–37 million people watch a person sell goods online. The manufacturer’s appeal here is obvious. One of the toughest parts of the consumer goods world is getting in front of consumers’ eyeballs, where they can purchase it. Viya solves this—while spreading overall awareness.

Influencer marketing combines sales and marketing functions

The following major business processes drive consumer product companies:

1. Research and Development: Creating a product that consumers want.

2. Production: Figuring out how to manufacture the improved product at scale.

3. Supply chain: Ensuring that you have enough raw commodities to manufacture the product.

4. Transportation: Getting the product to the customer (retailer).

5. Sales: Ensuring the product gets prime placement for a customer through negotiations and pricing.

6. Marketing: Generating consumer awareness and demand through advertising.

Viya combines processes 5 and 6. Traditionally, Marketing would spread mass awareness and tell consumers where they can buy the product. Sales then work with retailers to make sure consumers easily find the product (through slotting and placement fees) and are enticed to buy it (through promotional allowances).

Bloomberg describes how the livestream works (Emphasis mine):

And, of course, everything is available at a deep discount, as long as it lasts. The link to buy a product isn’t released until after Viya’s done pitching and counts down: “5, 4, 3, 2, 1.” If a particularly popular deal runs out, she sometimes pleads with her off-camera producers on behalf of her audience to release more. It’s an honest question—the team is keeping track of inventory and sales in real-time—and a heck of a tactic.

Each one of the bolded tactics is just a modern application of traditional promotional allowances. There’s a price cut, supported by artificial scarcity (limited time offer), but instead of executing them within a store, Viya executes them over the internet.

Influencer Marketing and the QVC comparison

The standard and obvious Western comparison for Viya is QVC or the Home Shopping network. After all, each features people pitching products over video, supported by an advanced technological back-end that ensures consumers can quickly and securely purchase and receive the product.

Ron Popeil was a legendary infomercial and QVC pitchman. On the surface, he doesn’t seem that different from Viya. Ron invented a variety of kitchen gadgets–from the Chop-o-Matic, “Ladies and gentlemen, I’m going to show you the greatest kitchen appliance ever made,” to the Showtime Rotisserie, “Set it and forget”–He rose to prominence filming infomercials. As cable became widespread and the QVC network gained exposure, Popeil became a regular host. In essence, he was a live streamer. He was, of course, great at it, routinely selling $1 million worth of merchandise in one hour.

Here’s Malcolm Gladwell, in “The Pitchman,” describing his marketing strategy (emphasis mine):

There were no buttons being pressed, no hidden and intimidating gears: you could show-and-tell the Veg-O-Matic in a two-minute spot and allay everyone’s fears about a daunting new technology. More specifically, you could train the camera on the machine and compel viewers to pay total attention to the product you were selling. TV allowed you to do even more effectively what the best pitchman strove to do in live demonstrations—make the product the star.

The result of this approach was an enticing proposition to manufacturers.

A 1994 US News Report article on the rise of QVC explains why:

And since QVC deals directly with manufacturers and sells in such vast quantities, its cost of goods is lower than that of many traditional retailers. Designer Diane Von Furstenberg, who now sells her clothes exclusively through QVC, estimates she can price her blouses, skirts and blazers on television at less than half what a department store would have to charge. “Being on QVC allows me to pass up the middleman, the double shipping, the double warehousing, the showroom costs,” says Von Furstenberg. With fewer layers nibbling away at profits, QVC enjoys a larger gross profit margin — 42 percent in 1992 — than a typical department store. “And they don’t pay rent, sales help or advertising,” adds consultant Millstein, listing three of the largest costs for traditional store owners.

Manufacturers maintain their margin but gain access to a huge pool of buyers. Consumers get lower prices for high-quality goods. QVC facilitates it all and takes a cut.

The result was a win/win/win for consumers, manufacturers, and QVC.

Viya and other influencers act as a discounter

Viya shuns the infomercial strategy. Instead, she is the star of the show. It’s Viya, Viya alone that approves the product and pleads with producers to release more goods.

To bolster their own credibility, live streamers demand deep discounts and generous add-ons from the brands they work with. And the long-term effects of a successful promotion can be modest. Less than 10% of customers through live streams become repeat buyers, compared with 40% of the customers who come directly through Tmall, said Roger Huang, China CEO for Saville & Quinn, a U.K. skincare company. “It’s just one wave, and then it’s over. They’re Viya’s fans, and they follow her call,” he said. “Livestreaming is very effective, but we can’t get addicted.”

On the surface, live streamers and other social media influencers seem like an ideal pitchman. However, in reality, they have more in common with Dollar General or Family Dollar than QVC or the Home Shopping Network.

The product will never be the star–instead, it will always be second to the live streamer or store. People go to discount stores because they know they can get deals; they’ll never go because of a brand–it’s the same game with influencer marketing.

Like discounters, it makes sense to engage with influencers like Viya–given the reach of the major players. However, like discounters, manufacturers should consider adjusting quantity counts, creating new SKUs, and limiting trade spend.

Or else influencer marketing led growth could become a mirage, propped up by trade spend.

“Many consumers have returned to some of those pantry staples that we’ve had in our portfolio during this pandemic, and it’s reminding them of their love for a lot of the Kraft Heinz brands,” Christopher Urban, Kraft Heinz’s vice president of global strategic capabilities, said at a virtual licensing conference on Monday. “And we see this in our data. We’ve seen significant increases in household penetration across many of our brands over the past few months. In some cases on some of the brands, we are seeing record high numbers. And I think this increase in household penetration just makes the brands even more relevant to the consumer.”

Urban spoke at the Licensing Week Virtual conference about the opportunities the food company has available and is pursuing, many through the agreement signed last year with Brand Central. Kraft Heinz, which owns scores of well-known and globally beloved brands, entered the Brand Central agreement to transform its megabrands Heinz, Kool-Aid, Planters, Jet-Puffed, Oscar Meyer, Philadelphia, Kraft Macaroni and Cheese and Velveeta into lifestyle brands.

So here’s Kraft’s logic as I see it:

A global pandemic led to record sales for almost every CPG company

Record sales reintroduced old brands to new consumers

They are going to extend the momentum through brand licensing deals

Consider me skeptical. Given the realities of Kraft-Heinz’s business, this seems to be at best an incremental revenue driver.

How Brand Licensing Works

By 1995 M&M’s had lost their mojo. After a generation in the business, sales of the hard-coated candy were flat. The brand was at risk of becoming a commodity. “They’d become just candy.” Susan Credle, a creative director at BBDO, told Business Insider, “An aisle store candy brand versus an icon brand.”

With help from marketing firm BBDO, Mars Inc. transformed the brand into one of the most beloved in America.

BBDO’s idea: Take the colors of the candies in the bag and develop each into a character to make a comedic ensemble.

Credle describes M&M’s as the “court jester” brand — when the king is getting slaughtered, the jester comes in to lift them up.

Along came Red (the sarcastic one,) Yellow (the simple one,) Blue (the cool one,) and Green (the sexy one) — and later, Brown and Orange, too.

The characters debuted at the Super Bowl and were an instant sensation. Today, over twenty years later, M&M’s are still the best-selling chocolate brand in America. Perhaps more importantly, the company leveraged the characters to successfully evolve into a brand licensing platform. People didn’t just want to buy chocolate candies, they wanted to associate with M&M’s themselves. They wanted t-shirts, notebooks, stickers.

Long-term licensing partners include apparel, housewares and plush provider ERE; novelty and candy dispenser maker CandyRific; electronic accessory company Maxell; calendar maker Trends International LLC; travel accessory provider EB Brands and watchmaker MZ Berger. MRG in the past year added apparel maker Mad Engine Inc. and cycling jersey manufacturer Brainstorm Gear to its list of licensees.

This was transformational growth. Apparel, housewares, electronic products–all by a candy company. Kraft-Heinz is betting that it can capture similar enthusiasm with Oscar Meyer, Kool-Aid or any of their legacy brands.

One of the reasons I am skeptical of Kraft-Heinz is that under 3G’s management, the company has effectively no track record of building brands. In fact, they have a strong track record of using zero-based-budgeting to drive efficiencies—which can often destroy a legacy brand’s value. M&M’s transition from a branded candy to a lifestyle brand wasn’t cheap.

In fact, it took one big, bold, and expensive bet—a physical retail store to truly cement the change. A branded retail store is a place where a brand’s image turns into a real experience. Scott Galloway calls it a “temple to the brand.”

Patrick McIntyre, Director of Global Retail at Mars, described the strategy at Insider Trends:

Where brands come to life is advertising either in a TV commercial, in a print ad, or in some interaction that a consumer has with the brand. That’s a snapshot in time. It’s one moment and then it’s over, and then you’re on to the next thing. I think many brands, and us in particular, ealized a long time ago is the impact of being able to amplify those brand attributes in an experience where someone can actually be immersed fully within that brand. That’s what we started 20 years ago with our first M&M’s World Store in Las Vegas – a very famous tourist location. We created a four-floor 28,000-square foot store that was completely and totally dedicated to M&M’s.

Today, Mars Inc. has seven full M&M branded retail stores. The London location alone drives 5.3 million visitors a year. The company has an additional store planned at perhaps the most exceptional branded merchandise company in the world—Disney World.

Kraft-Heinz’s approach could drive some incremental revenue

Given that Kraft-Heinz lacks the characters of M&M and it a full-service retail store seems impractical—especially given COVID-19 realities—I think the safest bet is that the brand licensing initiative is used as a supplement to its dwindling research and development arm (Which I’ve covered in detail here).

One of the goals of this website is to illuminate the context surrounding different business strategies throughout history. A lot of what we consider innovation isn’t new, but re-coloring past strategies. That brings me to fake eggs and Coca-Cola bottler distribution strategy.

Eat Just Inc., a plant-based egg substitute company that has sold about 40 million fake eggs—mostly in America. It is looking to aggressively expand into China, where the average person eats 50 eggs a year, compared to just 35 in America.

Tetrick’s plan for international expansion depends on local partners, who will be expected to mix Just’s mung protein with oil, water, and other ingredients, then bottle and ship the products. The CEO cites Coca-Cola Co.’s syrup distribution network as an inspiration and says current board member Jacob Robbins, a former Coke supply chain executive, persuaded him to outsource distribution and the final stages of production.

The rise of the Coca-Cola Bottler

Today, Coca-Cola is arguably the most famous brand in the world. You can go to almost any country on earth and buy a Coke bottle from a convenience store, and it will taste the same in Germany as it does in Brazil. Very few companies have the reach or the consistency. This simple fact is a testament to the power of Coca-Cola’s operations.

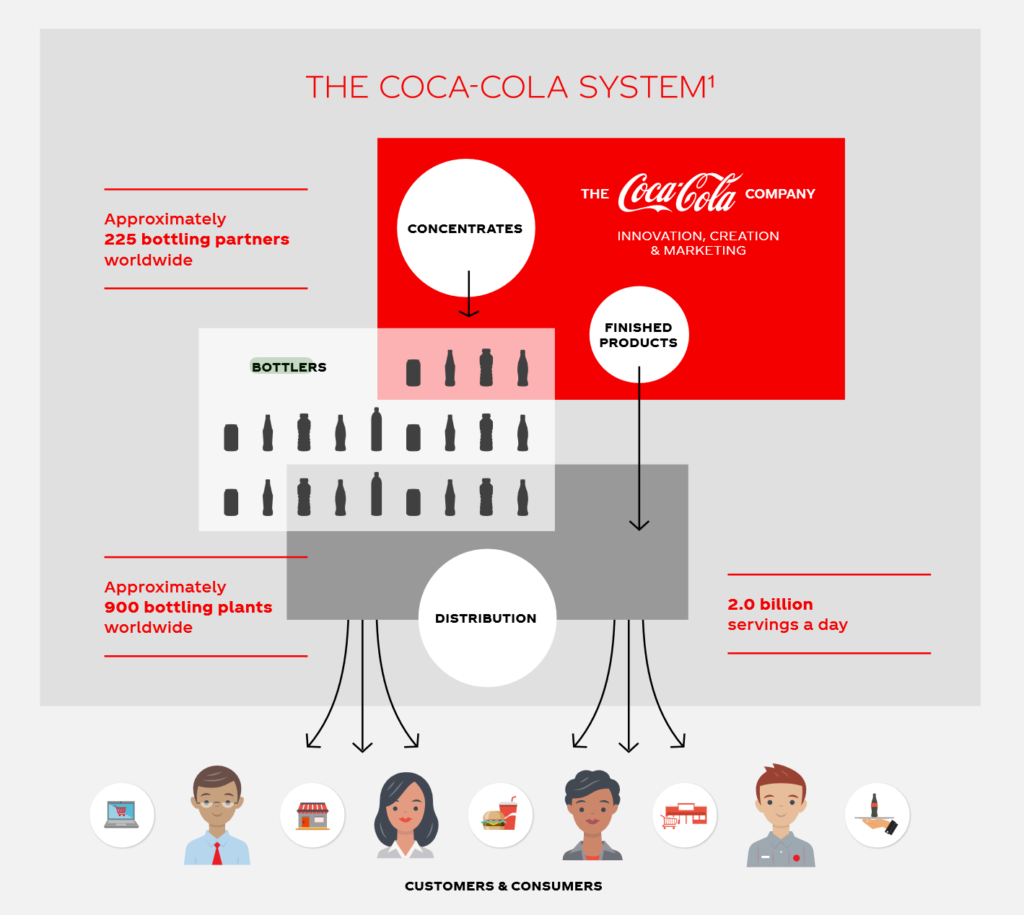

It’s even more impressive when you realize that a fateful 1899 decision means that Coca-Cola doesn’t manage its bottling operations. The Coca-Cola Company manufactures and sells soda concentrates to 225 different bottlers—which then produce millions of bottles of Coke. The bottlers are responsible for creating bottled soda and getting the finished goods to individual retail stores.

The below graphic, shows how it works:

Graphic via Coca-Cola’s 2019 Annual Report

Coca-Cola Bottler; part opportunity, part bad business decision.

Why would Coca-Cola give up its bottling operations? After all, vertical integration allows for higher profits—, especially once the business scales.

In 1899, two young lawyers from Chattanooga, Benjamin Franklin Thomas and Joseph Brown Whitehead, arranged an introduction to Asa Candler, traveled to Atlanta, and made a pitch for the rights to put the soft drink in bottles. At first Candler was unenthusiastic. Bottling was still a back-alley business, in his view, and there was a danger that Coca-Cola’s reputation might suffer if he allowed them to go ahead. Still, Candler told his visitors, he had no interest in keeping the bottling rights for himself and his company. “Gentlemen,” he recalled telling the two Chattanoogans, only half in jest, “we have neither the money, nor brains, nor time to embark in the bottling business.”

At the time, Coca-Cola was experiencing exponential growth. It was earning a 50%return on every bag of syrup it sold to a retailer. Asa Candler, the man who enabled this success, agreed to give away the Coca-Cola bottling rights—for free.

Early Coca-Cola Bottlers Struggled

Candler, Coca-Cola’s CEO, had two reasons to be skeptical of bottling.

Household refrigeration wasn’t widely available. The first mass produced domestic refrigerators arrived in the 1920s. It was not until 1945 when 85% of households had a refrigerator. Coke was best served cold and there was no easy way for people to keep it cold.

Bottles themselves were an unproven technology. Early soda used a “Hutchinson” bottle; a bottle “sealed by a rubber gasket haled in place by a long looping wire.” In the summer, Coca-Cola in a Hutchinson bottle was lucky to last two weeks.

From Chandler’s point-of-view, there wasn’t a market, nor the technology required to support bottling.

Initially, it looked as if Thomas and Whitehead would fail to get the project off the ground.

As they looked ahead to 1900 and the challenge of fulfilling their contract, Thomas and Whitehead realized there was no way they could afford the time and money it would take to open plants across the country one by one by themselves. Their only hope, they concluded, was to become “parent” bottlers, recruiting other men and giving them franchises to build the actual facilities and sell Coca-Cola in the surrounding territories.

To summarize the chain of events:

Coca-Cola outsourced bottling and distribution to a middleman

Unable to scale, the middleman outsourced bottling and distribution to established bottlers—essentially becoming a “service manager” for Coca-Cola

New Bottling Technology Fuels Growth

Running Parallel to all of this was William Painter, an Irish born, Baltimore based inventor. In 1892 he patented an early version of the modern bottle cap: his design standardized glass bottle necks and the corresponding topper. Standardization allowed mass sterilization. Manufacturers could quickly and systematically sterilize bottles—drastically increasing the shelf life of products.

With the technical shortcomings addressed, bottles exploded.

In most cities, a franchise to bottle Coca-Cola was now considered a license to make money. (Expressing the point explicitly, the bottler in San Antonio printed up a letterhead that depicted a Coke bottle spurting dollar signs, over the slogan, “There is money in it.”) Many bottlers found demand so heavy they divided their territories and assigned their rights to a new genus of sub-bottlers who built smaller, more efficient plants. There was no need to recruit new bottlers, because applicants were beating down the company’s door and begging for the opportunity.

Coca-Cola Bottler: Money for Nothing

Bottling opened up a whole new channel for Coke. Within decades syrup sales to bottlers would account for 40 percent of Coca-Cola’s overall revenue. Thomas and Whitehead’s ‘parent’ bottling company found itself in perhaps the best position.

The parent companies were left without a clearly defined role. Syrup was shipped from the Coca-Cola Company’s factories directly to the actual bottlers, so the parents were not even acting as genuine middlemen. They simply sat back and took a royalty on every gallon, even though they never handled a drop. The parents paid the Coca-Cola Company 92 cents a gallon for syrup, then turned around and “resold” it to the actual bottlers at a generous markup, usually $1.20 a gallon. It was all done on paper.

So to recap: Asa Candler, the man who enabled Coca-Cola’s massive rise, agreed to not only give away the Coca-Cola bottling rights but structured the deal in a way where Coke ended up paying a middleman (parent bottlers) for the privilege.

Eat Just’s Rationale

The primary benefit of the Coca-Cola bottler strategy is that instead of building out a physical production and distribution footprint, a company can tap into an established network and scale quickly. The downside is that you lose margin once successful. Plus, they’re going to be at the whim of their partners. Assuming Eat Just operates the “parent bottler” strategy, and has reasonable controls around the operation, it could make phenomenal sense for a company expanding into new markets.

Part of strategy isn’t just understanding the past, it’s learning from the mistakes of the past.

General Electric announced it would sell its lighting business to Savant Systems in a deal valued at $250 million. The agreement itself was long rumored but still comes as a surprise. In a way, the transaction signifies the death of an era–almost as if Coca-Cola sold of its sugary beverage line. General Electric didn’t invent the light bulb, but it did invent consumer light bulbs—the first affordable and mass-produced version. This spring boarded General Electric into the pantheon of history’s great companies. In the mid-2000s, G.E. was in everything from consumer goods to entertainment, and it boasted annual revenues on par with a middle-income country. Then, mismanagement forced the company to rethink the conglomerate strategy. “It has shifted its focus to making heavy equipment,” the WSJ wrote in its coverage, “like power turbines, aircraft engines, and hospital machines.” In 2019 G.E.’s revenue dropped to around $30 billion.

Sometimes significant shifts beg simple questions. If G.E. was one of history’s best companies and it was a conglomerate, what is a conglomerate? Is there a standard conglomerate definition? What was the rationale for becoming one? Did the conglomerate strategy lead to General Electrics’ decline?

A conglomerate is simply a holding company or corporation that operates in multiple industries, usually owning individual divisions that could stand apart as separate businesses on their own. Early conglomerates were initially focused on a suite of related activities, like G.E. and electrical system in the 1900s or branded food conglomerates of the 1920s.

Like all aspects of business, the conglomerate structure evolved as American politics evolved. Founded in 1892 by five titans, including J.P. Morgan and Thomas Edison, General Electric combined a variety of small electrical component companies under one umbrella.

As both businesses expanded, it had become increasingly difficult for either company to produce complete electrical installations relying solely on their own patents and technologies. In 1892, the two companies combined. They called the new organization the General Electric Company.

Several of Edison’s early business offerings are still part of G.E. today, including lighting, transportation, industrial products, power transmission, and medical equipment. The first G.E. Appliances electric fans were produced at the Ft. Wayne electric works as early as the 1890s, while a full line of heating and cooking devices were developed in 1907. G.E. Aircraft Engines, the division’s name only since 1987, actually began its story in 1917 when the U.S. government began its search for a company to develop the first airplane engine “booster” for the fledgling U.S. aviation industry. Thomas Edison’s experiments with plastic filaments for light bulbs in 1893 led to the first G.E. Plastics department, created in 1930.

Basically, through a variety of mergers and acquisitions, General Electric was able to monopolize all aspects of the early American electrical system—from the technical standards and power generation by industry—to the light bulbs screwed into sockets by consumers.

Throughout the Great Depression, America’s attitudes toward corporate concentration changed. The consensus view was that monopoly power, like General Electric held, was bad for society. The result was a variety of New Deal regulations designed to stop conglomerates from rolling up entire industries.

Stoller explains what happened next:

But in the early 1960s a new type of conglomerate emerged, although this time these corporations were shaped by strict antitrust laws. In this instance, cash-rich corporations like RCA and LTV invested in entirely unrelated lines of business—Hertz or Wilson Sporting Goods,say—the argument being that an excellent executive team could manage any line of business well. One of the highest-flying conglomerates at the time, LTV, bought business lines in missiles, electronics, electrical cable, sporting goods, meat and food processing, and pharmaceuticals.

Essentially, General Electric was generating enormous amounts of cash and could no longer use that money to acquire businesses within its core industry.

General Electric, like many monopoly-based conglomerates, decided to expand outward.

The benefits of a conglomerate

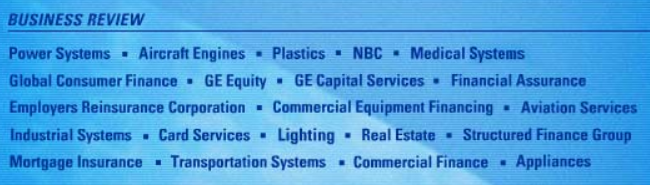

The following image lists every industry General Electric operated in 2000. That year it had revenues of about $130 billion. Adjusted for inflation, that’s about $190 billion of revenue in modern times. To put things in perspective, in 2019 the IMF estimated the New Zealand had a total GDP of about $204 billion.

General Electric was incredibly diverse. It had its hands in everything from entertainment production (NBC) to Lighting and Medical systems.

Here’s the revenue break down by business unit:

Business Unit

Revenue (millions)

Percentage of total Revenue

Margin

Aircraft Engine

$10,770

8%

23%

Appliances

$5,887

5%

12%

Industrial Products and Systems

$11,848

9%

19%

NBC

$6,797

5

26%

Plastics

$7,776

6%

25%

Power Systems

$14,861

11%

19%

Technical Products and Services

7,915

6%

22%

GECS (Financial Services)

$66,177

51%

28%

The smallest business unit had revenues of over $5 billion; larger than many best-of-breed companies. It was the definition of a conglomerate.

So we know what conglomerates are and why they became diversified across a variety of industries. Any definition of a conglomerate needs to explain the benefits of the structure. There are three major pieces.

Rise of Management

G.E. viewed businesses as interchangeable. In the eyes of leadership, a great manager could manage a microwave division just as successfully as they could manage a production company. If there was an opportunity, even if it was completely unrelated to their core competency, the company would jump headfirst. General Electric was proved right during expansionary economic conditions and was dead wrong the minute things went south.

Reduced Short Term Risk

Appliances and Industrial Products don’t have high margins like entertainment or finance, but they involve less risk and generate large amounts of cash flow—that the company can use to fund other deals and reduce risky ones.

Writing in The Master Switch, Tim Wu describes how this enabled G.E. to purchase Universal, a film production company.

Universal would enjoy as much of a hedge as any entertainment firm could hope for. By 2008, G.E. had annual revenues of over $183 billion, while Universal had income of $5 billion, less than 3 percent of the total. With a holding company of that size, the prospect of losing millions on a single film, while not pleasant, is no existential threat. Here was the ultimate defense against even the biggest movie bomb: a corporate structure so titanic that the fate of a $200 million film can be a relatively minor concern.

Synergy!

Being a conglomerate in a variety of disparate industries allows the company to augment itself across a variety of transactions. Synergy is a terrible word, but it’s the best one I can think of.

The relationship is symbiotic. G.E. Capital helps G.E. by financing the customers that buy G.E. power turbines, jet engines, windmills, locomotives, and other products, offering low interest rates that competitors can’t match. In the other direction, G.E. helps G.E. Capital by furnishing the reliable earnings and tangible assets that enable the whole company to maintain that triple-A credit rating, which is overwhelmingly important to G.E.’s success. Company managers call it “sacred” and the “gold standard.” Immelt says it’s “incredibly important.”

That rating lets G.E. Capital borrow funds in world markets at lower cost than any pure financial company. For example, Morgan Stanley’s cost of capital is about 10.6% (as calculated by the EVA Advisers consulting firm). Citigroup’s is about 8.4%. Even Buffett’s Berkshire Hathaway has a capital cost of about 8%. But G.E.’s cost is only 7.3%, and in businesses where hundredths of a percentage point make a big difference, that’s an enormously valuable advantage. And thanks to the earnings strength of G.E.’s industrial side, G.E. Capital can maintain its rating without holding much capital on its balance sheet.

Combined with a rising stock market, in the mid-2000s, G.E.’s conglomerate strategy looked like a great deal.

Until it wasn’t.

The Weakness of a Conglomerate

No definition of a conglomerate would be complete without the structures weaknesses. If you look at G.E.’s 2000 income statement, something should stick out. It was ostensibly an industrial conglomerate that made everything from MRI machines, power turbines, and microwaves. However, around 50 percent of its revenues came from financial services—most of them intertwined with the industrial business. Again, management looked great during boom times, but it became clear how incompetent management was in bad times.

As entangled as it was in the mortgage bubble and the shadow banking sector, G.E. Capital toppled over. At the height of the 2008 crisis, literally no one would lend to it in the overnight markets. G.E. Capital was only saved by an emergency injection of $12 billion from Warren Buffet and other investors. It turned out that the good reputation and credit rating of G.E.’s traditional businesses had essentially been used to gamble wildly in the financial markets.

General Electric said Wednesday that the federal government had agreed to insure as much as $139 billion in debt for its lending subsidiary, G.E. Capital. This is the second time in a month that G.E. has turned to a federal program aimed at helping companies during the global credit crisis.

G.E. Capital is not a bank, but granting it access to a new program from the Federal Deposit Insurance Corporation may reassure investors and help the lender compete with banks that already have government-protected debt, a G.E. spokesman, Russell Wilkerson, told Bloomberg News.

“Inclusion in this program will allow us to source our debt competitively with other participating financial institutions,” Mr. Wilkerson said.

Essentially, all three of the benefits of a conglomerate were so grossly mismanaged that laws had to be shifted to classify G.E. as a bank. If it wasn’t reclassified, it could of brought down large portions of the world’s economy.

Compounding matters, G.E. followed up the financial crisis with a series of bad acquisitions across its’ entire portfolio—including, the largest industrial purchase in the company’s history.

Turns out it’s only easy to manage a large corporation when the stock market is rising.

Conclusion

Rephrasing Matt Stoller’s definition of a conglomerate:

General Electric was simply a corporation that operated in eight different industries, including medical devices, light bulbs, and power generation. At its’ peak, each division generated over $5 billion a year. In boom years, the structure reduced short-term risk, created synergies, and allowed managers to shine. In bad years, the inefficiencies and mismanagement, often masked by its size, brought the firm down.